Enlarge image

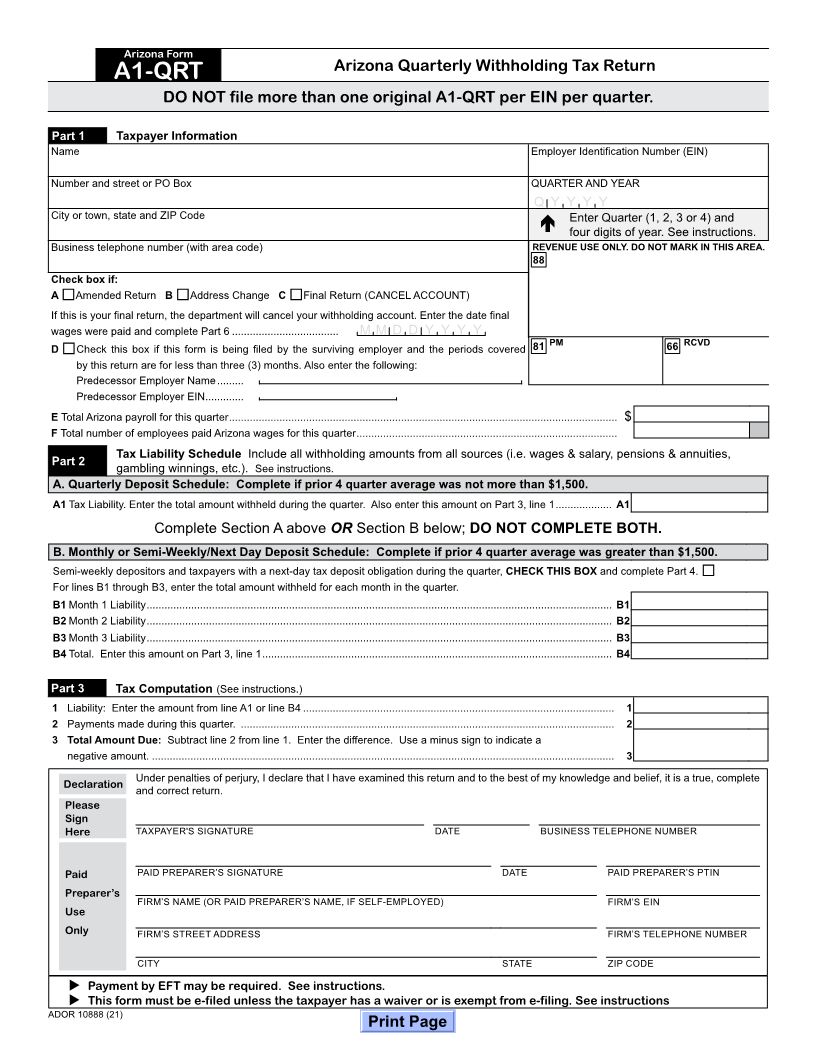

Arizona Form

Arizona Quarterly Withholding Tax Return

A1-QRT w

File no more than one original A1-QRT per EIN.

DO NOT file more than one original A1-QRT per EIN per quarter. Employer Identification Number (EIN)

Part 1 Taxpayer Information QUARTER AND YEAR*: Q Y Y Y Y

Name Employer Identification Number (EIN) *Quarter (1, 2, 3 or 4) and four digits of year

Enter this number

Number and street or PO Box QUARTER AND YEAR For these months: for the quarter:

January, February, March 1

Q Y Y Y Y

City or town, state and ZIP Code Enter Quarter (1, 2, 3 or 4) and April, May, June 2

July, August, September 3

four digits of year. See instructions.

Business telephone number (with area code) REVENUE USE ONLY. DO NOT MARK IN THIS AREA. October, November, December 4

88

Check box if:

A Amended Return B Address Change C Final Return (CANCEL ACCOUNT)

If this is your final return, the department will cancel your withholding account. Enter the date final

wages were paid and complete Part 6 .................................... M M D D Y Y Y Y

D Check this box if this form is being filed by the surviving employer and the periods covered 81 PM 66 RCVD

by this return are for less than three (3) months. Also enter the following:

Predecessor Employer Name .........

Predecessor Employer EIN .............

E Total Arizona payroll for this quarter ................................................................................................................................... $

F Total number of employees paid Arizona wages for this quarter ........................................................................................

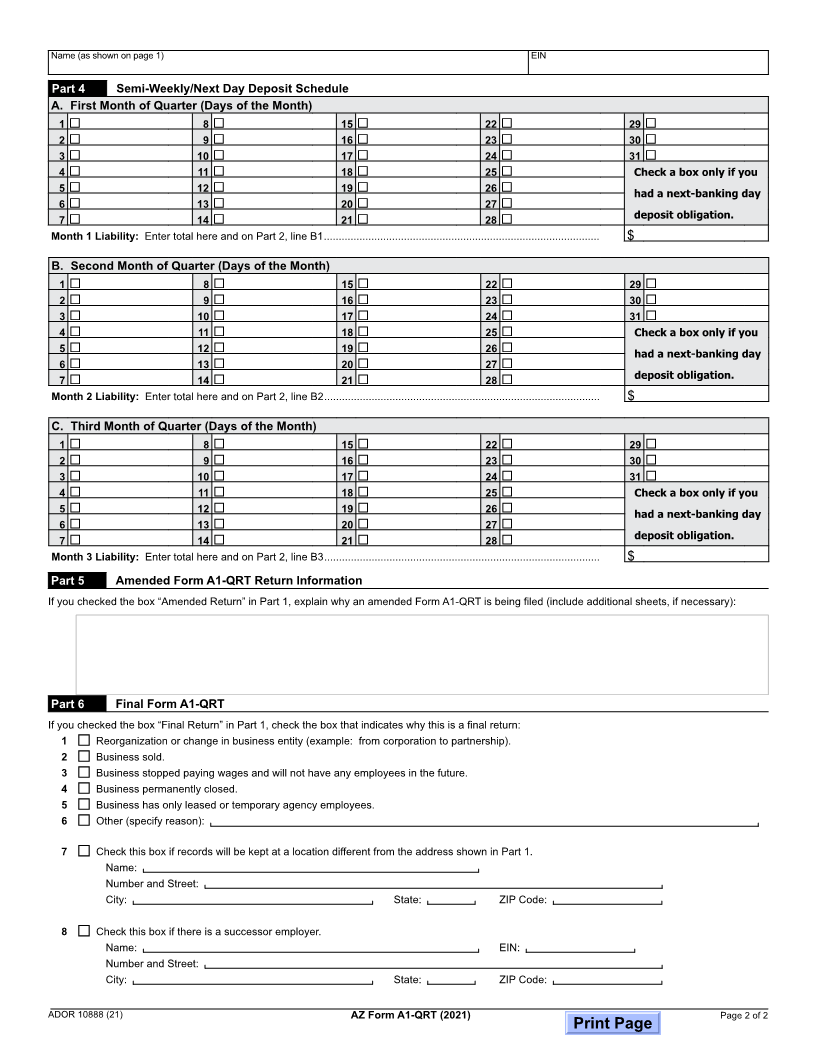

Tax Liability Schedule Include all withholding amounts from all sources (i.e. wages & salary, pensions & annuities,

Part 2 gambling winnings, etc.). See instructions.

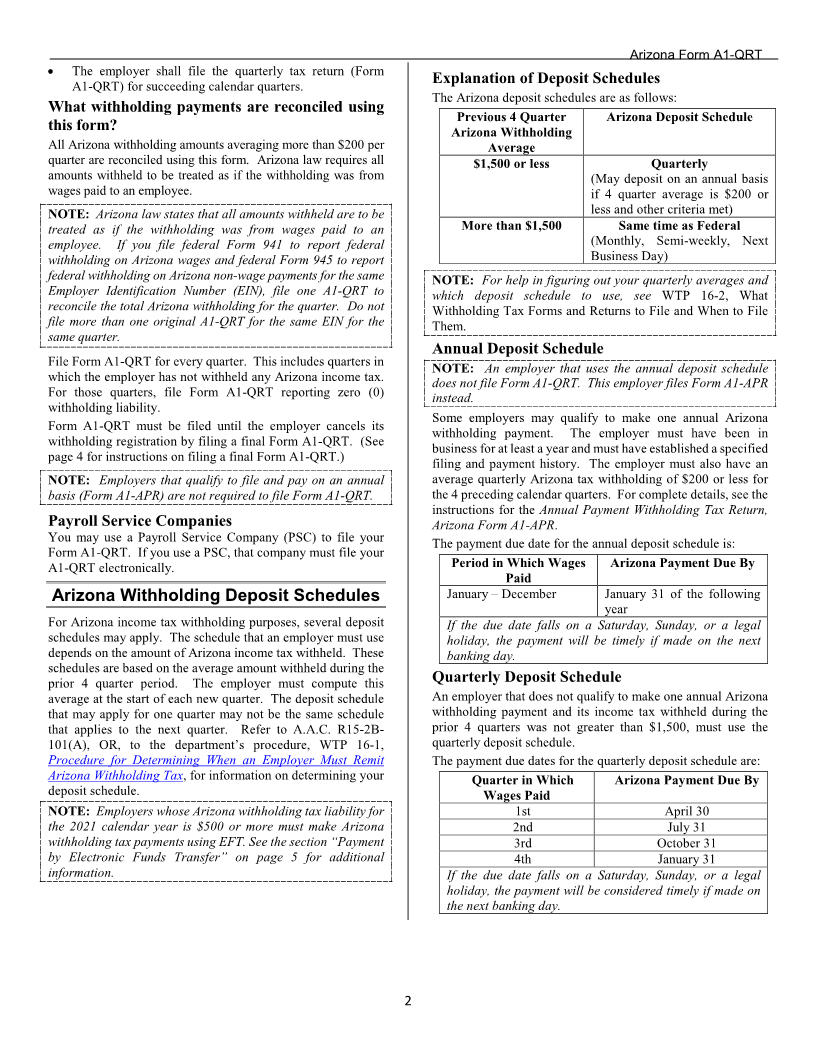

A. Quarterly Deposit Schedule: Complete if prior 4 quarter average was not more than $1,500.

A1 Tax Liability. Enter the total amount withheld during the quarter. Also enter this amount on Part 3, line 1 ................... A1

Complete Section A above OR Section B below; DO NOT COMPLETE BOTH.

B. Monthly or Semi-Weekly/Next Day Deposit Schedule: Complete if prior 4 quarter average was greater than $1,500.

Semi-weekly depositors and taxpayers with a next-day tax deposit obligation during the quarter, CHECK THIS BOX and complete Part 4.

For lines B1 through B3, enter the total amount withheld for each month in the quarter.

B1 Month 1 Liability ............................................................................................................................................................. B1

B2 Month 2 Liability ............................................................................................................................................................. B2

B3 Month 3 Liability ............................................................................................................................................................. B3

B4 Total. Enter this amount on Part 3, line 1 ...................................................................................................................... B4

Part 3 Tax Computation (See instructions.)

1 Liability: Enter the amount from line A1 or line B4 ......................................................................................................... 1

2 Payments made during this quarter. .............................................................................................................................. 2

3 Total Amount Due: Subtract line 2 from line 1. Enter the difference. Use a minus sign to indicate a

negative amount. ............................................................................................................................................................ 3

Declaration Under penalties of perjury, I declare that I have examined this return and to the best of my knowledge and belief, it is a true, complete

and correct return.

Please

Sign

Here TAXPAYER'S SIGNATURE DATE BUSINESS TELEPHONE NUMBER

Paid PAID PREPARER’S SIGNATURE DATE PAID PREPARER’S PTIN

Preparer’s

FIRM’S NAME (OR PAID PREPARER’S NAME, IF SELF-EMPLOYED) FIRM’S EIN

Use

Only FIRM’S STREET ADDRESS FIRM’S TELEPHONE NUMBER

CITY STATE ZIP CODE

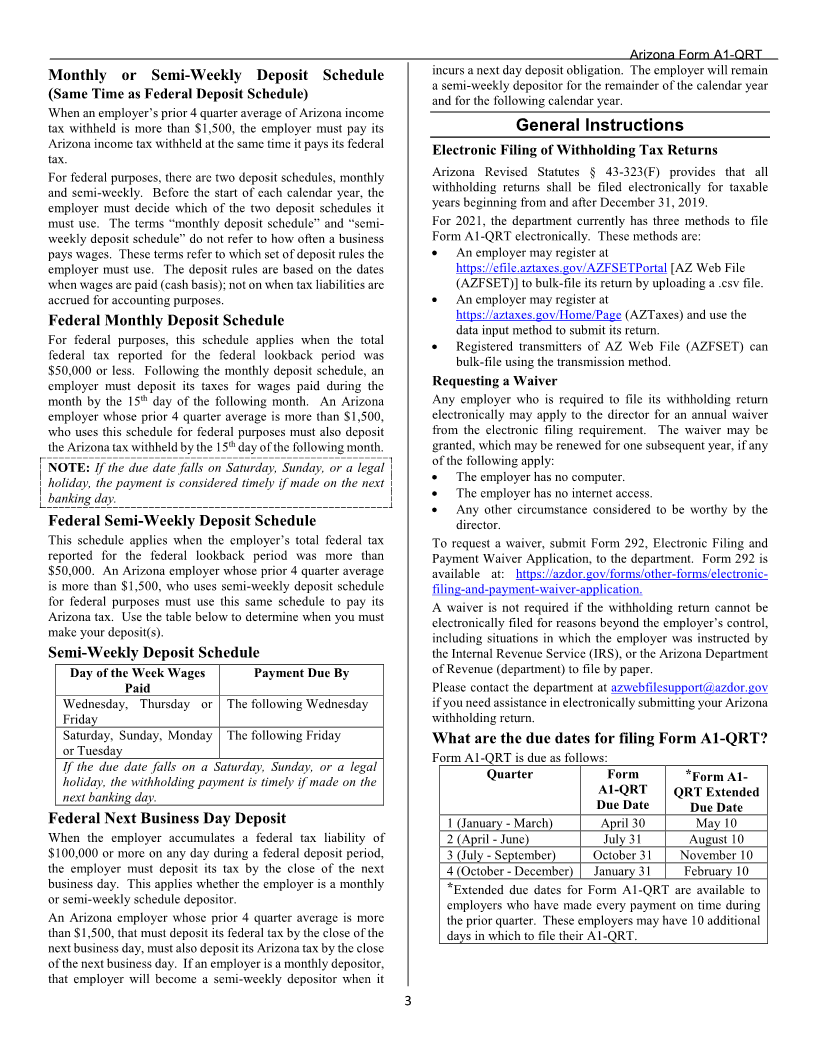

Payment by EFT may be required. See instructions.

This form must be e-filed unless the taxpayer has a waiver or is exempt from e-filing. See instructions

ADOR 10888 (21)

Print Page