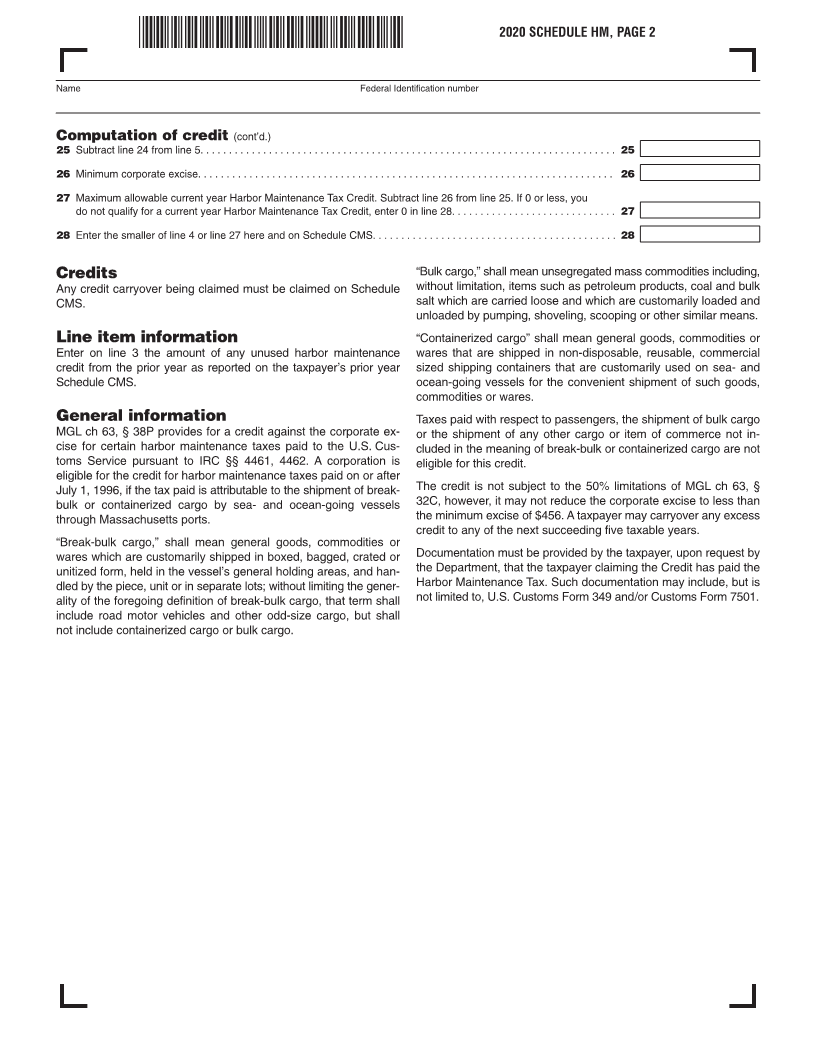

Enlarge image

Massachusetts Department of Revenue

Schedule HM

Harbor Maintenance Tax Credit 2020

For calendar year 2020 or taxable year beginning and ending

Name Federal Identification number

Fill in applicable oval: Shipper Exporter Importer

Current year harbor maintenance tax credit. Documentation must be provided upon request.

a. Tax paid on port b. Tax paid on port c. Tax paid on port

use for domestic move- use for exports of use for imports of

ments of break-bulk break-bulk and break-bulk and

Massachusetts port Date paid and containerized cargo containerized cargo containerized cargo

11 Total. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Computation of credit

12 Total qualifying harbor maintenance taxes for this year. Add line 1, col’s. a through c. . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

13 Enter unused credit from prior year. See instructions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

14 Massachusetts Harbor Maintenance Tax Credit available this year. Add lines 2 and 3. . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

15 Total corporate excise for purposes of determining allowable Harbor Maintenance Tax Credit. Form 355,

Computation of Excise, line 6; Form 355S, Computation of Excise, line 9; or Form 355U, Schedule U-ST, line 37. . . . . 5

16 Amount of Vanpool Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

17 Amount of ITC. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

18 Amount of EOAC. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

19 Amount of Research Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

10 Amount of Low-Income Housing Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Amount of Economic Development Incentive Program Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

12 Amount of Brownfields Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

13 Amount of Historic Rehabilitation Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

14 Amount of Film Incentive Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

15 Amount of Medical Device Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

16 Amount of Life Science Credit(s). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

17 Amount of Employer Wellness Program Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

18 Amount of Certified Housing Development Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

19 Amount of Low-Income Housing Donation Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

20 Amount of Veteran's Hire Tax Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

21 Amount of Community Investment Tax Credit (non-refundable). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

22 Amount of Apprentice Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

23 Amount of Vacant Store Credit. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

24 Add lines 6 through 23. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24