- 2 -

Enlarge image

|

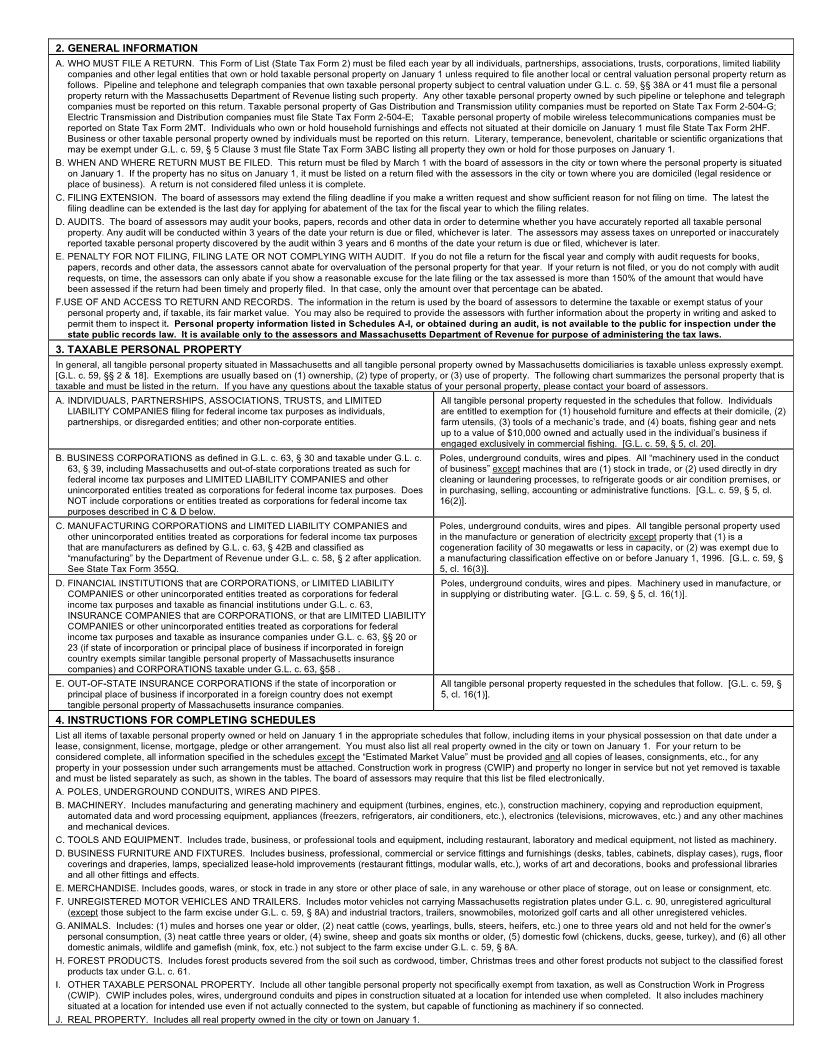

2. GENERAL INFORMATION

A. WHO MUST FILE A RETURN. This Form of List (State Tax Form 2) must be filed each year by all individuals, partnerships, associations, trusts, corporations, limited liability

companies and other legal entities that own or hold taxable personal property on January 1 unless required to file another local or central valuation personal property return as

follows. Pipeline and telephone and telegraph companies that own taxable personal property subject to central valuation under G.L. c. 59, §§ 38A or 41 must file a personal

property return with the Massachusetts Department of Revenue listing such property. Any other taxable personal property owned by such pipeline or telephone and telegraph

companies must be reported on this return. Taxable personal property of Gas Distribution and Transmission utility companies must be reported on State Tax Form 2-504-G;

Electric Transmission and Distribution companies must file State Tax Form 2-504-E; Taxable personal property of mobile wireless telecommunications companies must be

reported on State Tax Form 2MT. Individuals who own or hold household furnishings and effects not situated at their domicile on January 1 must file State Tax Form 2HF.

Business or other taxable personal property owned by individuals must be reported on this return. Literary, temperance, benevolent, charitable or scientific organizations that

may be exempt under G.L. c. 59, § 5 Clause 3 must file State Tax Form 3ABC listing all property they own or hold for those purposes on January 1.

B. WHEN AND WHERE RETURN MUST BE FILED. This return must be filed by March 1 with the board of assessors in the city or town where the personal property is situated

on January 1. If the property has no situs on January 1, it must be listed on a return filed with the assessors in the city or town where you are domiciled (legal residence or

place of business). A return is not considered filed unless it is complete.

C. FILING EXTENSION. The board of assessors may extend the filing deadline if you make a written request and show sufficient reason for not filing on time. The latest the

filing deadline can be extended is the last day for applying for abatement of the tax for the fiscal year to which the filing relates.

D. AUDITS. The board of assessors may audit your books, papers, records and other data in order to determine whether you have accurately reported all taxable personal

property. Any audit will be conducted within 3 years of the date your return is due or filed, whichever is later. The assessors may assess taxes on unreported or inaccurately

reported taxable personal property discovered by the audit within 3 years and 6 months of the date your return is due or filed, whichever is later.

E. PENALTY FOR NOT FILING, FILING LATE OR NOT COMPLYING WITH AUDIT. If you do not file a return for the fiscal year and comply with audit requests for books,

papers, records and other data, the assessors cannot abate for overvaluation of the personal property for that year. If your return is not filed, or you do not comply with audit

requests, on time, the assessors can only abate if you show a reasonable excuse for the late filing or the tax assessed is more than 150% of the amount that would have

been assessed if the return had been timely and properly filed. In that case, only the amount over that percentage can be abated.

F.USE OF AND ACCESS TO RETURN AND RECORDS. The information in the return is used by the board of assessors to determine the taxable or exempt status of your

personal property and, if taxable, its fair market value. You may also be required to provide the assessors with further information about the property in writing and asked to

permit them to inspect it. Personal property information listed in Schedules A-I, or obtained during an audit, is not available to the public for inspection under the

state public records law. It is available only to the assessors and Massachusetts Department of Revenue for purpose of administering the tax laws.

3. TAXABLE PERSONAL PROPERTY

In general, all tangible personal property situated in Massachusetts and all tangible personal property owned by Massachusetts domiciliaries is taxable unless expressly exempt.

[G.L. c. 59, §§ 2 & 18]. Exemptions are usually based on (1) ownership, (2) type of property, or (3) use of property. The following chart summarizes the personal property that is

taxable and must be listed in the return. If you have any questions about the taxable status of your personal property, please contact your board of assessors.

A. INDIVIDUALS, PARTNERSHIPS, ASSOCIATIONS, TRUSTS, and LIMITED All tangible personal property requested in the schedules that follow. Individuals

LIABILITY COMPANIES filing for federal income tax purposes as individuals, are entitled to exemption for (1) household furniture and effects at their domicile, (2)

partnerships, or disregarded entities; and other non-corporate entities. farm utensils, (3) tools of a mechanic’s trade, and (4) boats, fishing gear and nets

up to a value of $10,000 owned and actually used in the individual’s business if

engaged exclusively in commercial fishing. [G.L. c. 59, § 5, cl. 20].

B. BUSINESS CORPORATIONS as defined in G.L. c. 63, § 30 and taxable under G.L. c. Poles, underground conduits, wires and pipes. All “machinery used in the conduct

63, § 39, including Massachusetts and out-of-state corporations treated as such for of business” except machines that are (1) stock in trade, or (2) used directly in dry

federal income tax purposes and LIMITED LIABILITY COMPANIES and other cleaning or laundering processes, to refrigerate goods or air condition premises, or

unincorporated entities treated as corporations for federal income tax purposes. Does in purchasing, selling, accounting or administrative functions. [G.L. c. 59, § 5, cl.

NOT include corporations or entities treated as corporations for federal income tax 16(2)].

purposes described in C & D below.

C. MANUFACTURING CORPORATIONS and LIMITED LIABILITY COMPANIES and Poles, underground conduits, wires and pipes. All tangible personal property used

other unincorporated entities treated as corporations for federal income tax purposes in the manufacture or generation of electricity except property that (1) is a

that are manufacturers as defined by G.L. c. 63, § 42B and classified as cogeneration facility of 30 megawatts or less in capacity, or (2) was exempt due to

“manufacturing” by the Department of Revenue under G.L. c. 58, § 2 after application. a manufacturing classification effective on or before January 1, 1996. [G.L. c. 59, §

See State Tax Form 355Q. 5, cl. 16(3)].

D. FINANCIAL INSTITUTIONS that are CORPORATIONS, or LIMITED LIABILITY Poles, underground conduits, wires and pipes. Machinery used in manufacture, or

COMPANIES or other unincorporated entities treated as corporations for federal in supplying or distributing water. [G.L. c. 59, § 5, cl. 16(1)].

income tax purposes and taxable as financial institutions under G.L. c. 63,

INSURANCE COMPANIES that are CORPORATIONS, or that are LIMITED LIABILITY

COMPANIES or other unincorporated entities treated as corporations for federal

income tax purposes and taxable as insurance companies under G.L. c. 63, §§ 20 or

23 (if state of incorporation or principal place of business if incorporated in foreign

country exempts similar tangible personal property of Massachusetts insurance

companies) and CORPORATIONS taxable under G.L. c. 63, §58 .

E. OUT-OF-STATE INSURANCE CORPORATIONS if the state of incorporation or All tangible personal property requested in the schedules that follow. [G.L. c. 59, §

principal place of business if incorporated in a foreign country does not exempt 5, cl. 16(1)].

tangible personal property of Massachusetts insurance companies.

4. INSTRUCTIONS FOR COMPLETING SCHEDULES

List all items of taxable personal property owned or held on January 1 in the appropriate schedules that follow, including items in your physical possession on that date under a

lease, consignment, license, mortgage, pledge or other arrangement. You must also list all real property owned in the city or town on January 1. For your return to be

considered complete, all information specified in the schedules except the “Estimated Market Value” must be provided and all copies of leases, consignments, etc., for any

property in your possession under such arrangements must be attached. Construction work in progress (CWIP) and property no longer in service but not yet removed is taxable

and must be listed separately as such, as shown in the tables. The board of assessors may require that this list be filed electronically.

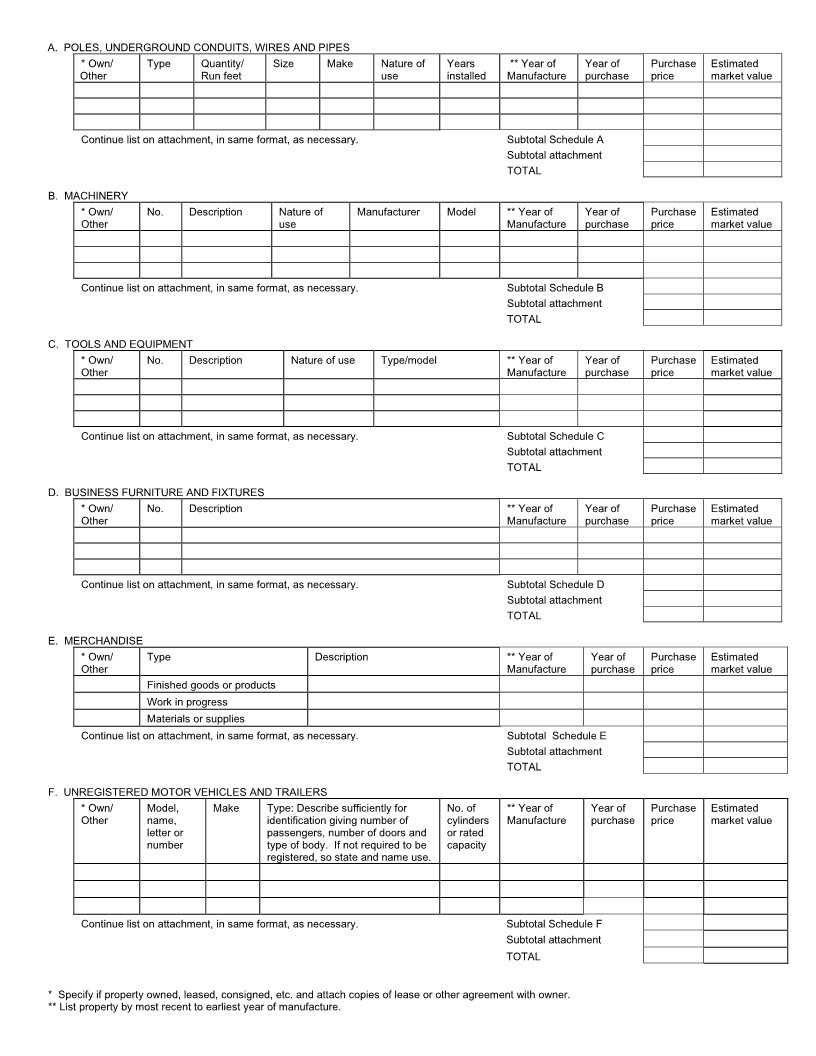

A. POLES, UNDERGROUND CONDUITS, WIRES AND PIPES.

B. MACHINERY. Includes manufacturing and generating machinery and equipment (turbines, engines, etc.), construction machinery, copying and reproduction equipment,

automated data and word processing equipment, appliances (freezers, refrigerators, air conditioners, etc.), electronics (televisions, microwaves, etc.) and any other machines

and mechanical devices.

C. TOOLS AND EQUIPMENT. Includes trade, business, or professional tools and equipment, including restaurant, laboratory and medical equipment, not listed as machinery.

D. BUSINESS FURNITURE AND FIXTURES. Includes business, professional, commercial or service fittings and furnishings (desks, tables, cabinets, display cases), rugs, floor

coverings and draperies, lamps, specialized lease-hold improvements (restaurant fittings, modular walls, etc.), works of art and decorations, books and professional libraries

and all other fittings and effects.

E. MERCHANDISE. Includes goods, wares, or stock in trade in any store or other place of sale, in any warehouse or other place of storage, out on lease or consignment, etc.

F. UNREGISTERED MOTOR VEHICLES AND TRAILERS. Includes motor vehicles not carrying Massachusetts registration plates under G.L. c. 90, unregistered agricultural

(except those subject to the farm excise under G.L. c. 59, § 8A) and industrial tractors, trailers, snowmobiles, motorized golf carts and all other unregistered vehicles.

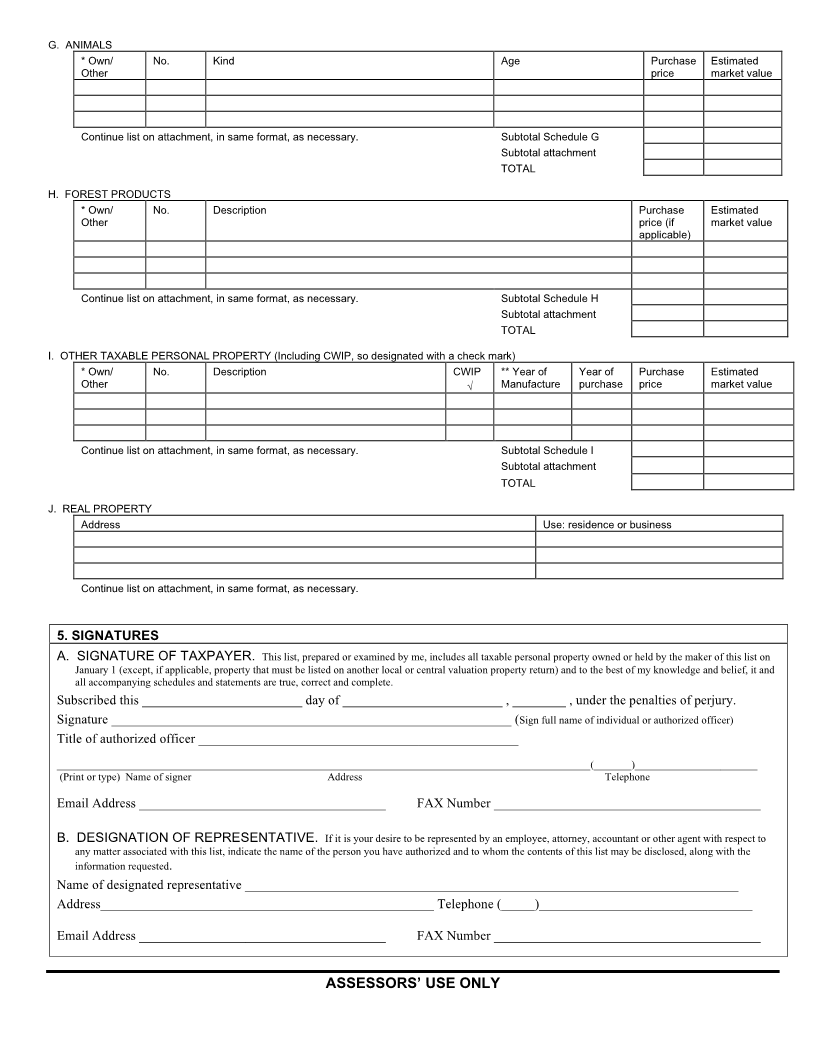

G. ANIMALS. Includes: (1) mules and horses one year or older, (2) neat cattle (cows, yearlings, bulls, steers, heifers, etc.) one to three years old and not held for the owner’s

personal consumption, (3) neat cattle three years or older, (4) swine, sheep and goats six months or older, (5) domestic fowl (chickens, ducks, geese, turkey), and (6) all other

domestic animals, wildlife and gamefish (mink, fox, etc.) not subject to the farm excise under G.L. c. 59, § 8A.

H. FOREST PRODUCTS. Includes forest products severed from the soil such as cordwood, timber, Christmas trees and other forest products not subject to the classified forest

products tax under G.L. c. 61.

I. OTHER TAXABLE PERSONAL PROPERTY. Include all other tangible personal property not specifically exempt from taxation, as well as Construction Work in Progress

(CWIP). CWIP includes poles, wires, underground conduits and pipes in construction situated at a location for intended use when completed. It also includes machinery

situated at a location for intended use even if not actually connected to the system, but capable of functioning as machinery if so connected.

J. REAL PROPERTY. Includes all real property owned in the city or town on January 1.

|