Enlarge image

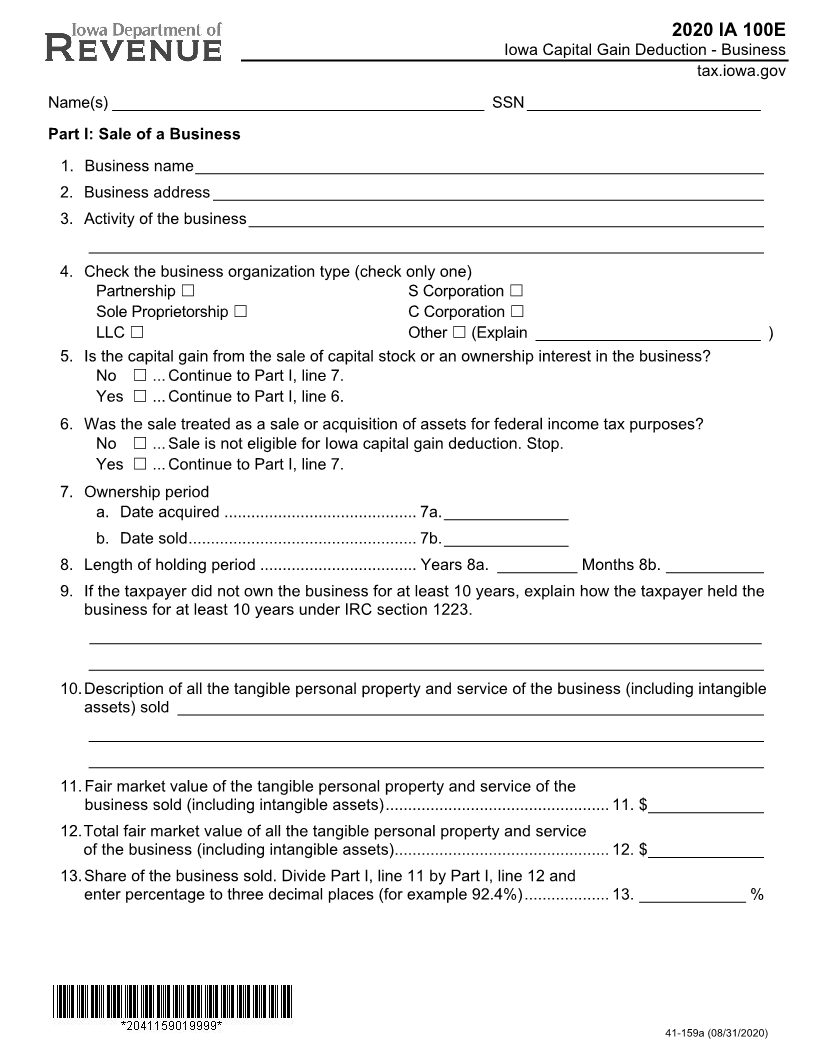

2020 IA 100E

Iowa Capital Gain Deduction - Business

tax.iowa.gov

Name(s) ___________________________________________ SSN ___________________________

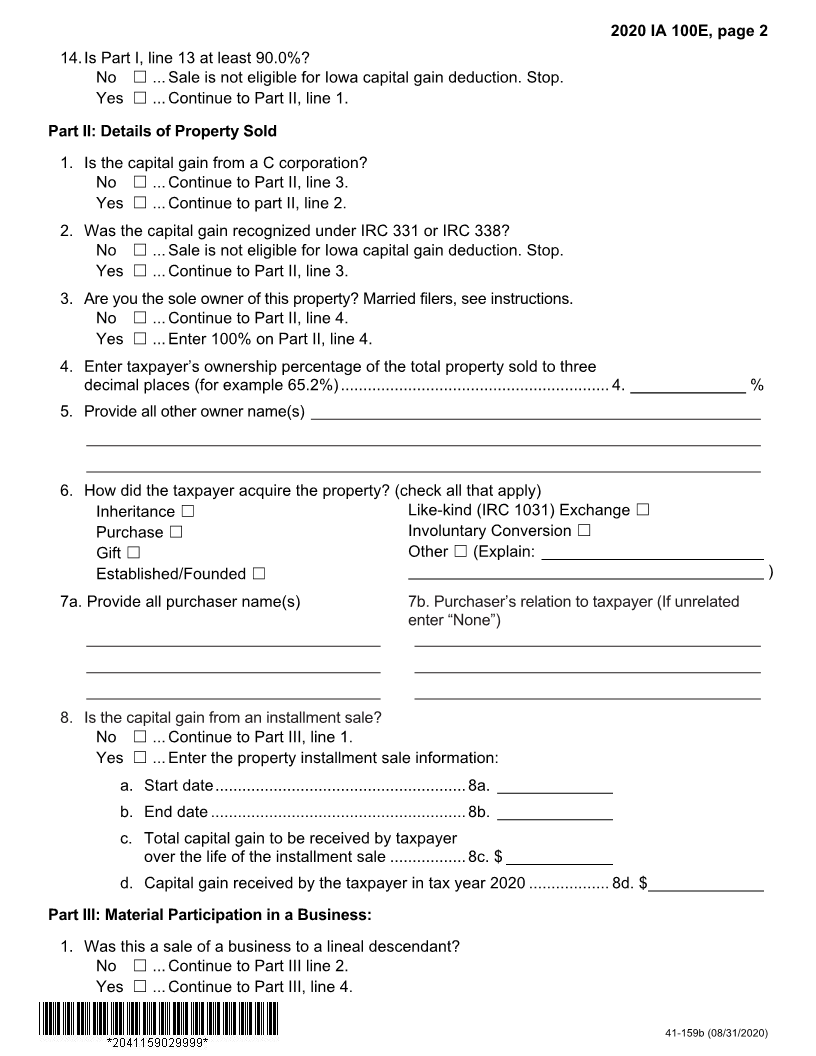

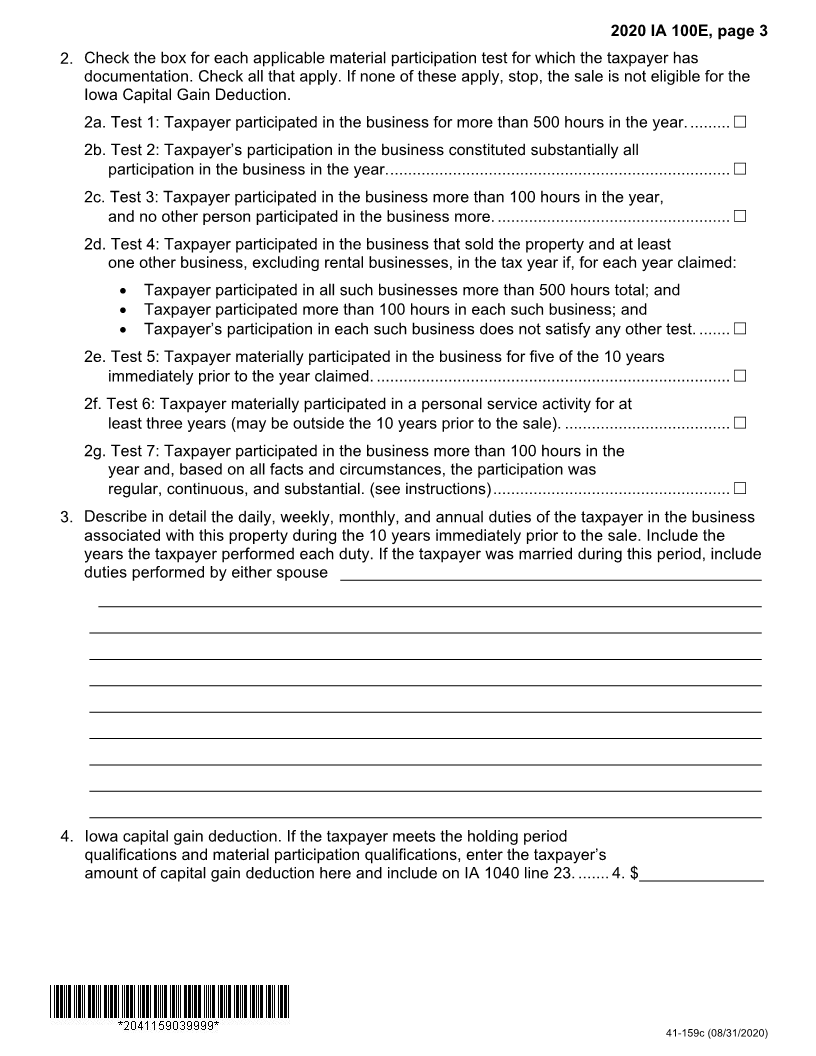

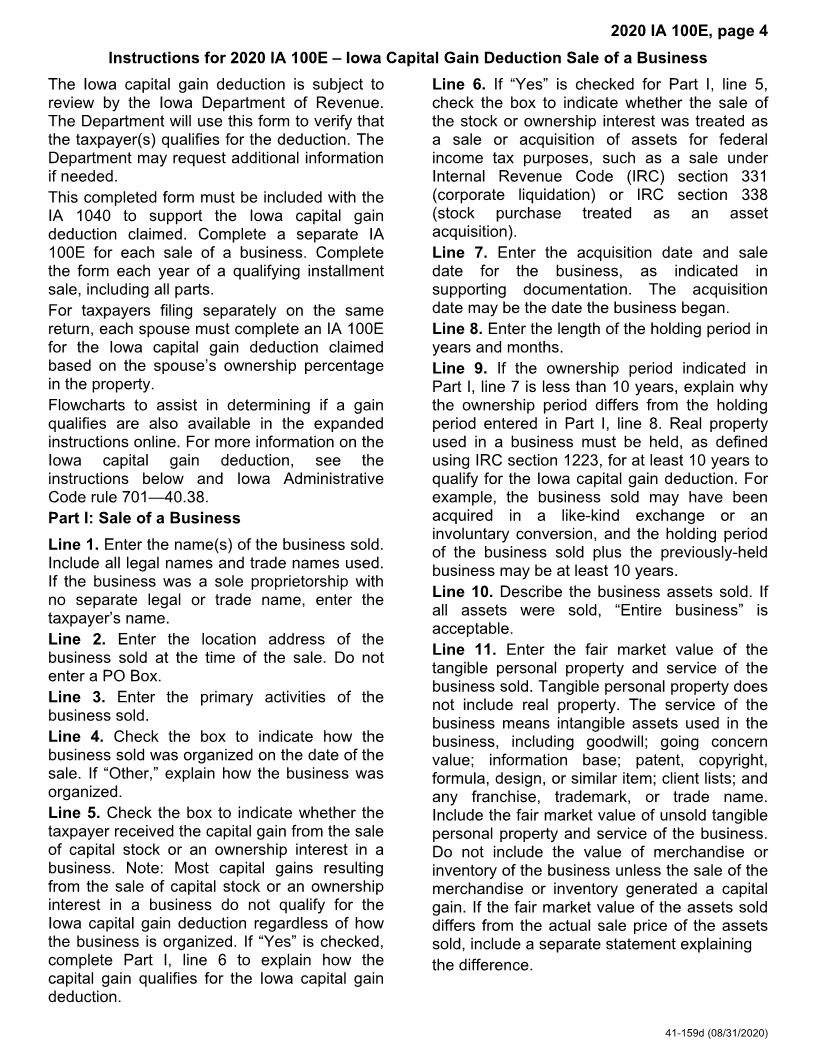

Part I: Sale of a Business

1. Business name ________________________________________________________________

2. Business address ______________________________________________________________

3. Activity of the business __________________________________________________________

____________________________________________________________________________

4. Check the business organization type (check only one)

Partnership ☐ S Corporation ☐

Sole Proprietorship ☐ C Corporation ☐

LLC ☐ Other ☐(Explain __________________________ )

5. Is the capital gain from the sale of capital stock or an ownership interest in the business?

No ☐ ... Continue to Part I, line 7.

Yes ☐... Continue to Part I, line 6.

6. Was the sale treated as a sale or acquisition of assets for federal income tax purposes?

No ☐ ... Sale is not eligible for Iowa capital gain deduction. Stop.

Yes ☐... Continue to Part I, line 7.

7. Ownership period

a. Date acquired ........................................... 7a. ______________

b. Date sold ................................................... 7b. ______________

8. Length of holding period ................................... Years 8a. _________ Months 8b. ___________

9. If the taxpayer did not own the business for at least 10 years, explain how the taxpayer held the

business for at least 10 years under IRC section 1223.

___________________________________________________________________________

____________________________________________________________________________

10. Description of all the tangible personal property and service of the business (including intangible

assets) sold __________________________________________________________________

____________________________________________________________________________

____________________________________________________________________________

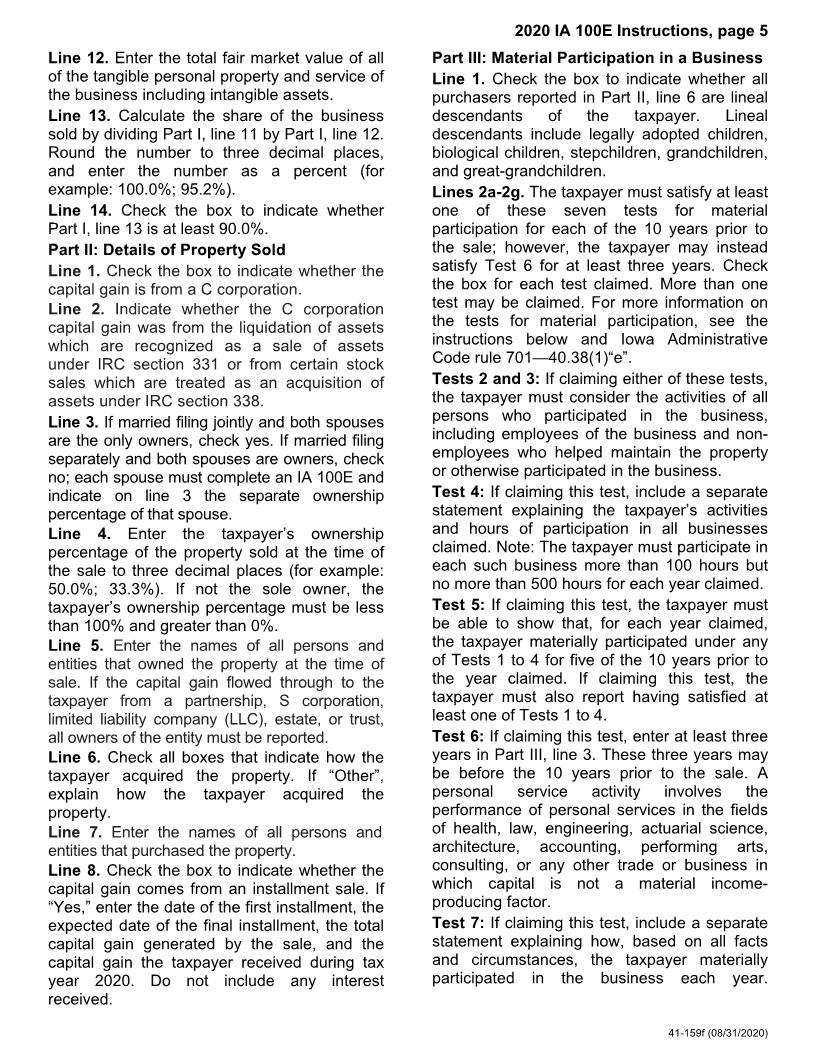

11. Fair market value of the tangible personal property and service of the

business sold (including intangible assets) .................................................. 11. $ _____________

12. Total fair market value of all the tangible personal property and service

of the business (including intangible assets) ................................................ 12. $ _____________

13. Share of the business sold. Divide Part I, line 11 by Part I, line 12 and

enter percentage to three decimal places (for example 92.4%) ................... 13. ____________ %

41-159a (08/31/2020)