Enlarge image

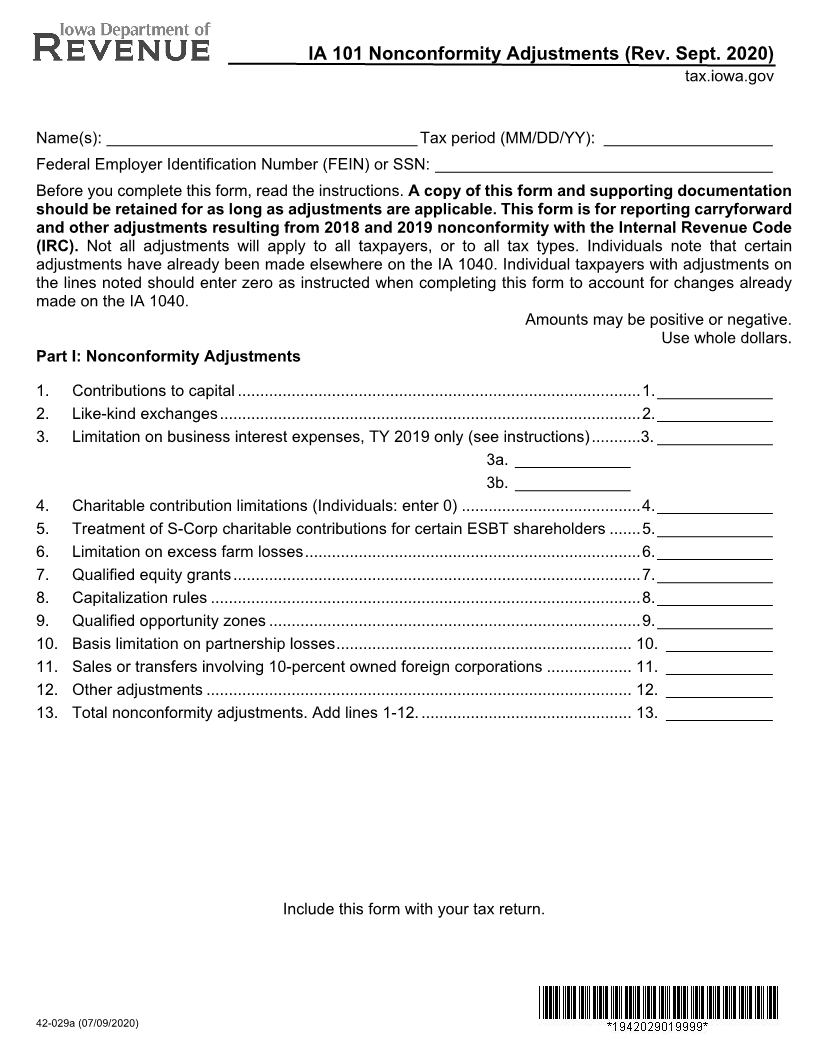

IA 101 Nonconformity Adjustments (Rev. Sept. 2020)

tax.iowa.gov

Name(s): ___________________________________ Tax period (MM/DD/YY): ___________________

Federal Employer Identification Number (FEIN) or SSN: ______________________________________

Before you complete this form, read the instructions. A copy of this form and supporting documentation

should be retained for as long as adjustments are applicable. This form is for reporting carryforward

and other adjustments resulting from 2018 and 2019 nonconformity with the Internal Revenue Code

(IRC). Not all adjustments will apply to all taxpayers, or to all tax types. Individuals note that certain

adjustments have already been made elsewhere on the IA 1040. Individual taxpayers with adjustments on

the lines noted should enter zero as instructed when completing this form to account for changes already

made on the IA 1040.

Amounts may be positive or negative.

Use whole dollars.

Part I: Nonconformity Adjustments

1. Contributions to capital .......................................................................................... 1. _____________

2. Like-kind exchanges .............................................................................................. 2. _____________

3. Limitation on business interest expenses, TY 2019 only (see instructions) ...........3. _____________

3a. _____________

3b. _____________

4. Charitable contribution limitations (Individuals: enter 0) ........................................ 4. _____________

5. Treatment of S-Corp charitable contributions for certain ESBT shareholders ....... 5. _____________

6. Limitation on excess farm losses ........................................................................... 6. _____________

7. Qualified equity grants ........................................................................................... 7. _____________

8. Capitalization rules ................................................................................................ 8. _____________

9. Qualified opportunity zones ................................................................................... 9. _____________

10. Basis limitation on partnership losses .................................................................. 10. ____________

11. Sales or transfers involving 10-percent owned foreign corporations ................... 11. ____________

12. Other adjustments ............................................................................................... 12. ____________

13. Total nonconformity adjustments. Add lines 1-12. ............................................... 13. ____________

Include this form with your tax return.

42-029a (07/09/2020)