- 14 -

Enlarge image

|

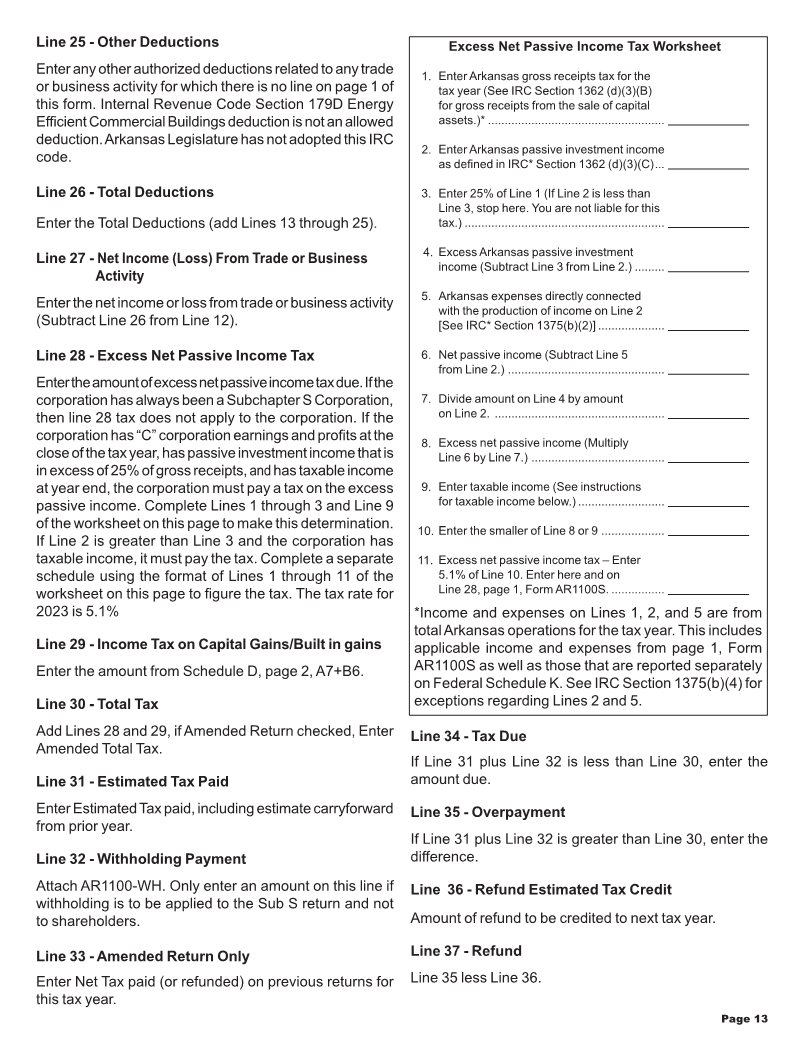

Taxable Income (Line 9 of the Excess Net Passive regular course of the taxpayer’s trade or business and

Income Tax Worksheet) includes income from tangible and intangible property

if the acquisition, management, and disposition of the

Line 9, taxable income, is defined in IRC Section 1374(d). property constitute integral parts of the taxpayer’s trade

Figure this income by completing Lines 9 through 27 or business operations. In essence, all income which arises

of page 1, or Schedule A, page 2 of Form AR1100CT, from the conduct of trade or business operations of a

Arkansas Corporation Income Tax Return. Include taxpayer is business income. Income of any type or class

the Form AR1100CT computation with the worksheet and from any source is business income if it arises from

computation you attached to Form AR1100S. You do transactions and activity occurring in the regular course

not have to attach the schedules etc. called for on Form of a trade or business. In general, all transactions and

AR1100CT. However you may want to complete certain activities of the taxpayer’s economic enterprise as a whole

schedules such as Schedule D, Form AR1100S. constitute the taxpayer’s trade or business and will be

considered “Business Income”, unless otherwise excluded

Schedule D (Form AR1100S) by Arkansas law. ACA 26-51-701(e) defines Nonbusiness

income as all income other than business income.

Enter on Line 29 the tax from Schedule D, Form AR1100S,

For tax years beginning on or after January 1, 2021,

page 2. If net capital gain for Arkansas is $25,000 or less,

all multistate corporations should use the single sales

the corporation is not liable for capital gains tax. If the net

factor only unless they are required to use a three

capital gain is more than $25,000 you must determine if the

factor apportionment formula under the special industry

corporation owes the tax in part A, or part B of Schedule

apportionment regulations. If a special industry three-factor

D, Form AR1100S. The tax rate for 2023 is 5.1%

apportionment rule applies, the business income is to be

apportioned to this state by multiplying the income by a

Part A – Capital gains tax computation

fraction; the numerator of which is the property factor, plus

the payroll factor plus two (2) times the sales factor, and

If the corporation made its election to be an S Corporation

the denominator of which is four (4).

before 1987, IRC Section 1374 (as in effect before the

enactment of the Tax Reform Act of 1986) continues to The sales factor is a fraction; the numerator of which is

impose a tax on certain gains of the S Corporation. Consult the total sales of the taxpayer in this state during the tax

the IRS instructions to determine if you are liable for this period and the denominator of which is the total sales of

tax. If so, complete Part A, Schedule D, Form AR1100S. the taxpayer everywhere during the tax period.

If multistate, under Schedule D, part A, Line 3, multiply by

Sales of tangible personal property are in this state if:

apportionment factor from Part B, Line 5 of Schedule A.

(a) the property is delivered or shipped to a purchaser,

other than the United States Government, within this State

Part B – Built-in gains tax computation

regardless of the f.o.b. point or other conditions of the

sale or: (b) the property is shipped from an office, store,

If the corporation made its election to be an S Corporation

warehouse, factory, or

after December 31,1986, IRC Section 1374 provides for a other place of storage in this State

and: (1) the purchaser is the United States Government or:

tax on built-in gains that applies to certain S corporations.

(2) the taxpayer is not taxed in the State of the purchaser.

Consult the IRS instructions to determine if you are liable

for this tax. If so, complete Part B, Schedule D, Form Sales, other than sales of tangible personal property, are

AR1100S. If multistate, under Schedule D, Part B, Line in this State if the income producing activity is performed

2, multiply apportionment factor from Part B, Line 5 of both within and without the State, in which event the income

Schedule A. allocable to this State shall be the percentage that is used

in the formula for apportioning business income to this

Worksheet for Apportionment of State.

Multistate Corporations

Prior written approval is required before deviation

For corporations with income from sources within and

from the allocation and apportionment method.

without the State:

In general, taxpayers with income derived from activities Apportionment Formula

both within and outside the State are required to allocate

and apportion the net income under the following: Construction companies, pipelines, and private

railcar operators must utilize the three factor double

Business Income is defined in ACA 26-51-701(a) as weighted sales factor apportionment method, briefly

income arising from transactions and activity in the outlined on page 17. Broadcasters and publishers will

Page 14

|