Enlarge image

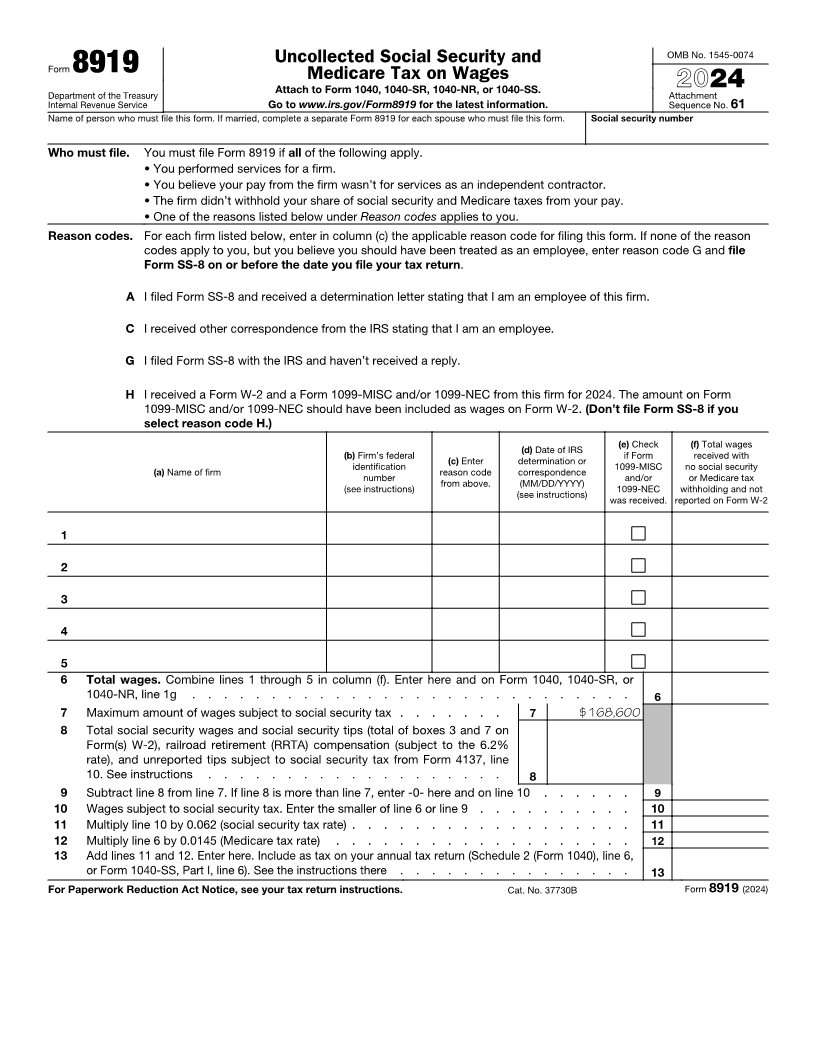

OMB No. 1545-0074

Uncollected Social Security and

Form 8919 Medicare Tax on Wages

Department of the Treasury Attach to Form 1040, 1040-SR, 1040-NR, or 1040-SS. 2024

Attachment

Internal Revenue Service Go to www.irs.gov/Form8919 for the latest information. Sequence No. 61

Name of person who must file this form. If married, complete a separate Form 8919 for each spouse who must file this form. Social security number

Who must file. You must file Form 8919 if all of the following apply.

• You performed services for a firm.

• You believe your pay from the firm wasn’t for services as an independent contractor.

• The firm didn’t withhold your share of social security and Medicare taxes from your pay.

• One of the reasons listed below under Reason codes applies to you.

Reason codes. For each firm listed below, enter in column (c) the applicable reason code for filing this form. If none of the reason

codes apply to you, but you believe you should have been treated as an employee, enter reason code G and file

Form SS-8 on or before the date you file your tax return.

A I filed Form SS-8 and received a determination letter stating that I am an employee of this firm.

C I received other correspondence from the IRS stating that I am an employee.

G I filed Form SS-8 with the IRS and haven’t received a reply.

H I received a Form W-2 and a Form 1099-MISC and/or 1099-NEC from this firm for 2024. The amount on Form

1099-MISC and/or 1099-NEC should have been included as wages on Form W-2. (Don’t file Form SS-8 if you

select reason code H.)

(b) Firm’s federal (d) Date of IRS (e) Check (f) Total wages

(a) Name of firm identification (c) Enter determination or if Form received with

number reason code correspondence 1099-MISC no social security

(see instructions) from above. (MM/DD/YYYY) and/or or Medicare tax

(see instructions) 1099-NEC withholding and not

was received. reported on Form W-2

1

2

3

4

5

6 Total wages. Combine lines 1 through 5 in column (f). Enter here and on Form 1040, 1040-SR, or

1040-NR, line 1g . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

7 Maximum amount of wages subject to social security tax . . . . . . . 7 $168,600

8 Total social security wages and social security tips (total of boxes 3 and 7 on

Form(s) W-2), railroad retirement (RRTA) compensation (subject to the 6.2%

rate), and unreported tips subject to social security tax from Form 4137, line

10. See instructions . . . . . . . . . . . . . . . . . . . 8

9 Subtract line 8 from line 7. If line 8 is more than line 7, enter -0- here and on line 10 . . . . . . 9

10 Wages subject to social security tax. Enter the smaller of line 6 or line 9 . . . . . . . . . . 10

11 Multiply line 10 by 0.062 (social security tax rate) . . . . . . . . . . . . . . . . . . 11

12 Multiply line 6 by 0.0145 (Medicare tax rate) . . . . . . . . . . . . . . . . . . . 12

13 Add lines 11 and 12. Enter here. Include as tax on your annual tax return (Schedule 2 (Form 1040), line 6,

or Form 1040-SS, Part I, line 6). See the instructions there . . . . . . . . . . . . . . . 13

For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 37730B Form 8919 (2024)