Enlarge image

Userid: CPM Schema: Leadpct: 100% Pt. size: 10 Draft Ok to Print

instrx

AH XSL/XML Fileid: … -form-8959/2024/a/xml/cycle04/source (Init. & Date) _______

Page 1 of 4 14:25 - 12-Nov-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

2024

Instructions for Form 8959

Additional Medicare Tax

Section references are to the Internal Revenue Code considered for purposes of this tax. RRTA compensation

unless otherwise noted. should be separately compared to the threshold.

Your employer is responsible for withholding the 0.9%

Future Developments Additional Medicare Tax on your Medicare wages or RRTA

compensation paid in excess of $200,000 in a calendar

For the latest information about developments related to year. Your employer is required to begin withholding

Form 8959 and its instructions, such as legislation Additional Medicare Tax in the pay period in which your

enacted after they were published, go to IRS.gov/ wages or compensation for the year exceed $200,000 and

Form8959. continue to withhold it in each pay period for the

remainder of the calendar year.

Reminders

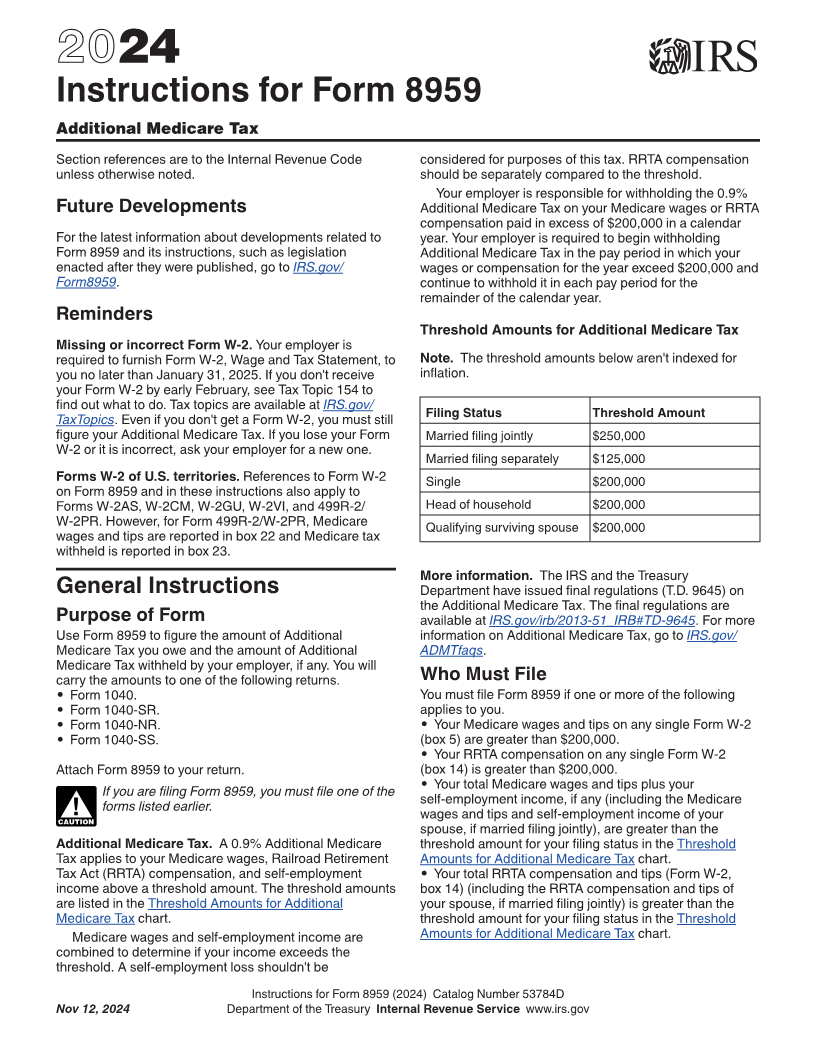

Threshold Amounts for Additional Medicare Tax

Missing or incorrect Form W-2. Your employer is

required to furnish Form W-2, Wage and Tax Statement, to Note. The threshold amounts below aren't indexed for

you no later than January 31, 2025. If you don't receive inflation.

your Form W-2 by early February, see Tax Topic 154 to

find out what to do. Tax topics are available at IRS.gov/

Filing Status Threshold Amount

TaxTopics. Even if you don't get a Form W-2, you must still

figure your Additional Medicare Tax. If you lose your Form Married filing jointly $250,000

W-2 or it is incorrect, ask your employer for a new one.

Married filing separately $125,000

Forms W-2 of U.S. territories. References to Form W-2 Single $200,000

on Form 8959 and in these instructions also apply to

Forms W-2AS, W-2CM, W-2GU, W-2VI, and 499R-2/ Head of household $200,000

W-2PR. However, for Form 499R-2/W-2PR, Medicare Qualifying surviving spouse $200,000

wages and tips are reported in box 22 and Medicare tax

withheld is reported in box 23.

More information. The IRS and the Treasury

General Instructions Department have issued final regulations (T.D. 9645) on

the Additional Medicare Tax. The final regulations are

Purpose of Form available at IRS.gov/irb/2013-51_IRB#TD-9645. For more

Use Form 8959 to figure the amount of Additional information on Additional Medicare Tax, go to IRS.gov/

Medicare Tax you owe and the amount of Additional ADMTfaqs.

Medicare Tax withheld by your employer, if any. You will

carry the amounts to one of the following returns. Who Must File

• Form 1040. You must file Form 8959 if one or more of the following

• Form 1040-SR. applies to you.

• Form 1040-NR. • Your Medicare wages and tips on any single Form W-2

• Form 1040-SS. (box 5) are greater than $200,000.

• Your RRTA compensation on any single Form W-2

Attach Form 8959 to your return. (box 14) is greater than $200,000.

If you are filing Form 8959, you must file one of the • Your total Medicare wages and tips plus your

self-employment income, if any (including the Medicare

! forms listed earlier. wages and tips and self-employment income of your

CAUTION

spouse, if married filing jointly), are greater than the

Additional Medicare Tax. A 0.9% Additional Medicare threshold amount for your filing status in the Threshold

Tax applies to your Medicare wages, Railroad Retirement Amounts for Additional Medicare Tax chart.

Tax Act (RRTA) compensation, and self-employment • Your total RRTA compensation and tips (Form W-2,

income above a threshold amount. The threshold amounts box 14) (including the RRTA compensation and tips of

are listed in the Threshold Amounts for Additional your spouse, if married filing jointly) is greater than the

Medicare Tax chart. threshold amount for your filing status in the Threshold

Medicare wages and self-employment income are Amounts for Additional Medicare Tax chart.

combined to determine if your income exceeds the

threshold. A self-employment loss shouldn't be

Instructions for Form 8959 (2024) Catalog Number 53784D

Nov 12, 2024 Department of the Treasury Internal Revenue Service www.irs.gov