Enlarge image

Userid: CPM Schema: instrx Leadpct: 100% Pt. size: 9 Draft Ok to Print

AH XSL/XML Fileid: … -form-8960/2024/a/xml/cycle03/source (Init. & Date) _______

Page 1 of 22 16:56 - 18-Nov-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

2024

Instructions for Form 8960

Net Investment Income Tax—Individuals, Estates, and Trusts

Section references are to the Internal Revenue Code unless Regulations section 1.1411-10. See Regulations section

otherwise noted. 1.965-1(d).

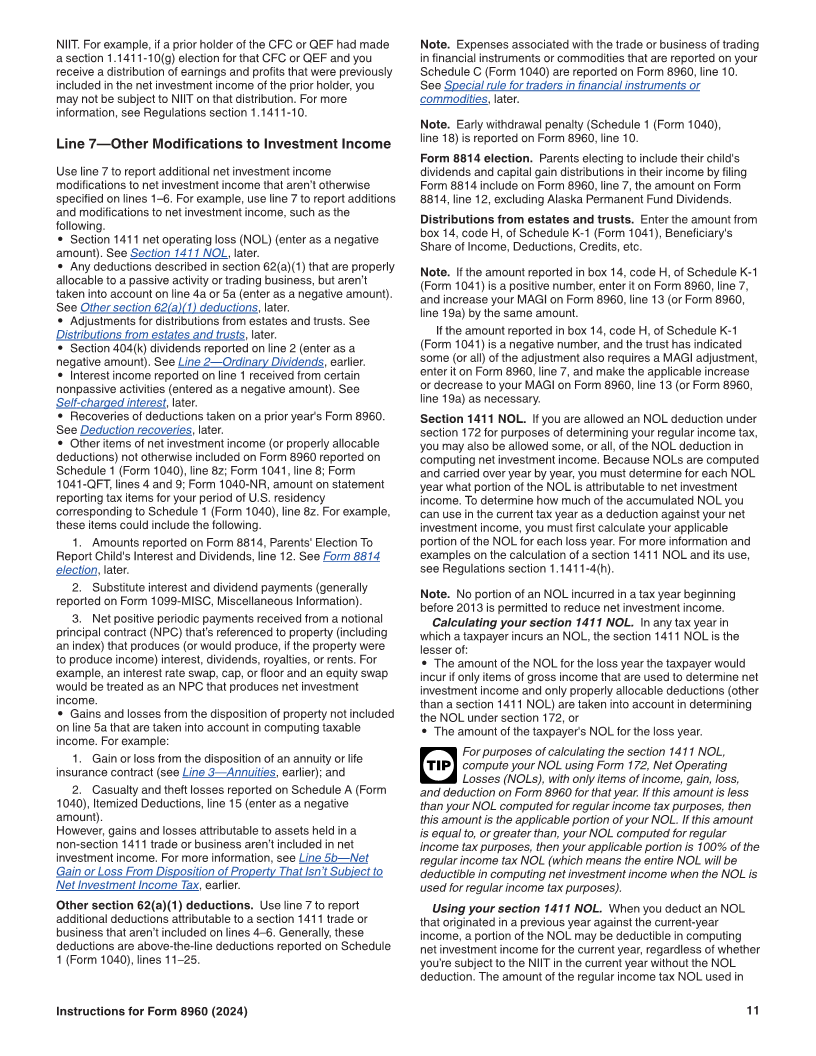

Excluded income. Excluded income means:

Future Developments • Income excluded from gross income in chapter 1 of the

Internal Revenue Code;

For the latest information about developments related to Form • Income not included in net investment income; and

8960 and its instructions, such as legislation enacted after they • Gross income and net gain specifically excluded by section

were published, go to IRS.gov/Form8960. 1411, related regulations, or other guidance published in the

Internal Revenue Bulletin.

General Instructions Examples of excluded items are:

• Wages,

Reminders • Unemployment compensation,

• Alaska Permanent Fund Dividends,

Digital assets. Income derived from transactions involving • Alimony,

digital assets may be subject to the tax imposed on net • Social security benefits,

investment income under section 1411(a), which applies in • Tax-exempt interest income,

addition to other income taxes imposed under Subtitle A of the • Income from certain qualified retirement plan distributions,

code. and

Charitable contribution deduction for electing small busi- • Income subject to self-employment taxes.

ness trusts (ESBTs). Line 18b of Form 8960 was updated to Net investment income. Generally, net investment income

reflect changes outlined in P. L. 115-97, section 13542, that includes gross income from interest, dividends, annuities,

amended the way the S portion of an ESBT accounts for royalties, and rents, unless they’re derived from the ordinary

charitable contribution deductions under section 170(b) instead course of a trade or business that isn’t (a) a passive activity, or

of section 641(c), effective January 1, 2018. See Line 18b (b) a trade or business of trading in financial instruments or

Deductions for Distributions of Net Investment Income and commodities. In addition, net investment income includes other

Charitable Deductions. gross income derived from a trade or business that’s (a) a

Trade or business income subject to net investment in- passive activity, or (b) a trade or business of trading in financial

come tax (NIIT). Line 4a of Form 8960 was amended to bring instruments or commodities. Additionally, net investment income

attention to certain income reported on Schedule C (Form 1040) includes net gain (to the extent taken into account in computing

and Schedule E (Form 1040) that is subject to NIIT. This change taxable income) attributable to the disposition of property other

was made to the instructions for Form 8960 in tax year 2022 to than property held in a trade or business that’s not (a) a passive

better reflect section 1411(c)(2). activity, or (b) a trade or business of trading in financial

These instructions are based mostly on Regulations sections instruments or commodities. To arrive at net investment income,

1.1411-1 through 1.1411-10. the above items are reduced by deductions allowed against the

income tax that are properly allocable to those items of gross

Who Must File income or net gain. See section 1411(c) and Regulations

sections 1.1411-4 and 1.1411-10(c).

Attach Form 8960 to your return if your modified adjusted gross

income (MAGI) is greater than the applicable threshold amount. Passive foreign investment company (PFIC). Generally, a

PFIC is any foreign corporation if at least 75% of its gross

Purpose of Form income is passive income or an average of at least 50% of its

Use Form 8960 to figure the amount of your Net Investment assets produce passive income or are held for the production of

Income Tax (NIIT). passive income. See section 1297(a).

Qualified electing fund (QEF). Generally, a QEF is a PFIC for

Definitions which the taxpayer has made an election under section 1295(b)

Controlled foreign corporation (CFC). Generally, a CFC is and the PFIC complies with IRS requirements for determining

any foreign corporation if more than 50% of its voting power or ordinary earnings and net capital gain. See section 1295(a).

stock value is owned or considered owned by U.S. shareholders Section 1.1411-10(g) election. An election made under

(as defined in section 951(b)) on any day during the tax year. Regulations section 1.1411-10(g) (section 1.1411-10(g)

Certain foreign insurance companies are considered CFCs if election). See Regulations Section 1.1411-10(g) Election, later.

more than 25% of their voting power or stock value is owned or

considered owned by U.S. shareholders (as defined in section Section 1411 trade or business. Generally, a trade or

951(b)) on any day during the tax year. See section 957(a) and business that’s either a passive activity for the taxpayer or is a

(b). Additionally, certain foreign insurance companies with trade or business of trading in financial instruments or

related person insurance income may be CFCs. See section commodities. See section 1411(c)(2) and Regulations section

953(c). A specified foreign corporation described in section 1.1411-5(a).

965(e)(1)(B) and Regulations section 1.965-1(f)(45)(i)(B) that is

not otherwise a CFC is treated as a CFC for purposes of

Instructions for Form 8960 (2024) Catalog Number 53783S

Nov 18, 2024 Department of the Treasury Internal Revenue Service www.irs.gov