Enlarge image

Userid: CPM Schema: instrx Leadpct: 100% Pt. size: 9 Draft Ok to Print

AH XSL/XML Fileid: … form-843/202412/a/xml/cycle03/source (Init. & Date) _______

Page 1 of 6 7:47 - 17-Dec-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Instructions for Form 843

(Rev. December 2024)

(For use with Form 843 (Rev. December 2024))

Claim for Refund and Request for Abatement

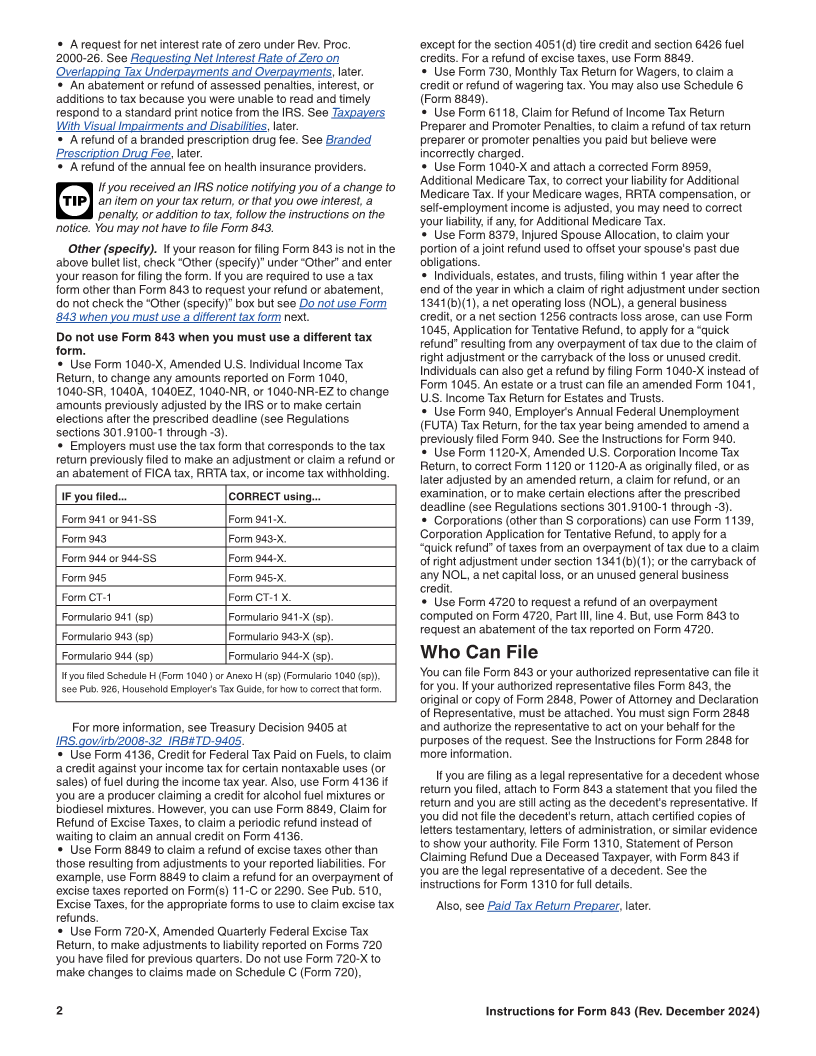

Section references are to the Internal Revenue Code unless Do not use Form 843 to request an abatement of

otherwise noted. ! income, estate, or gift tax. Do not use Form 843 to

CAUTION request a refund of income tax or Additional Medicare

Contents Page Tax. Employers cannot use Form 843 to request a refund or an

Future Developments . . . . . . . . . . . . . . . . . . . . . . . . 1 abatement of Federal Insurance Contributions Act (FICA) tax,

What’s New . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1 Railroad Retirement Tax Act (RRTA) tax, or income tax

General Instructions . . . . . . . . . . . . . . . . . . . . . . . . . 1 withholding. Also, do not use Form 843 to amend a previously

filed income or employment tax return. Do not use Form 843 to

Purpose of Form . . . . . . . . . . . . . . . . . . . . . . . . . 1 claim a refund of agreement fees, offer-in-compromise fees, or

Who Can File . . . . . . . . . . . . . . . . . . . . . . . . . . . 2 lien fees.

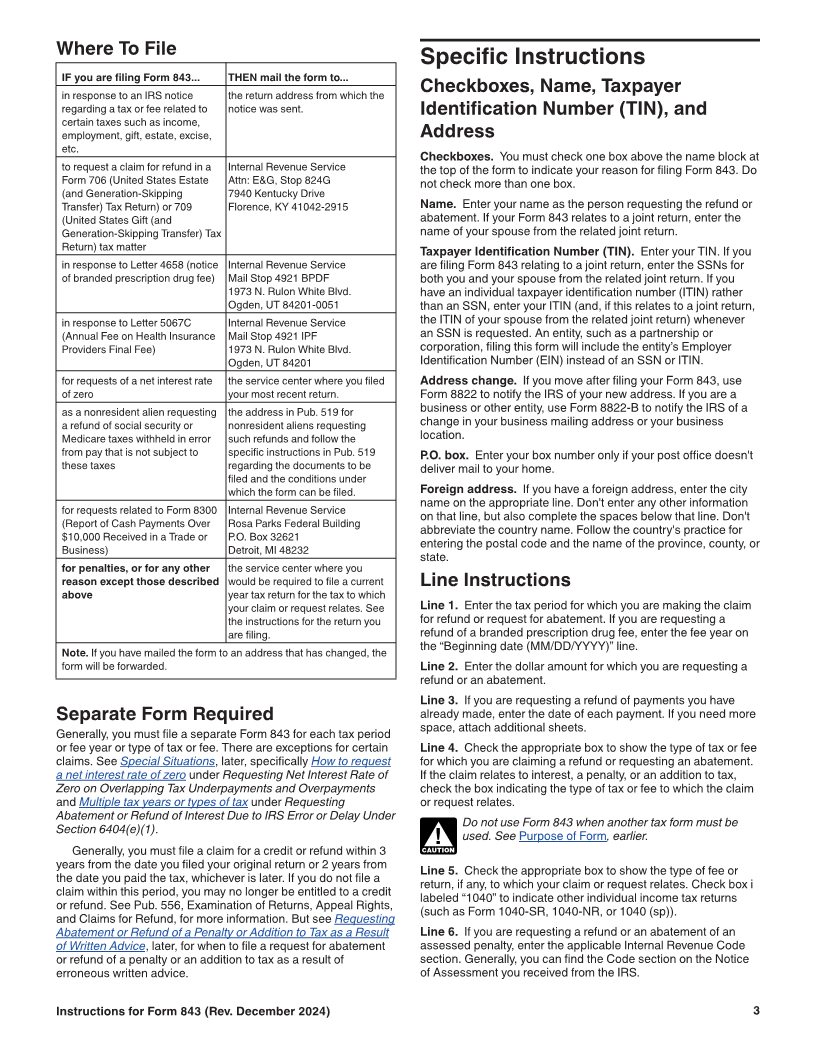

Where To File . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Separate Form Required . . . . . . . . . . . . . . . . . . . 3 Checkboxes at the top of Form 843. Check the box at the top

of your Form 843 that provides your reason for filing the form.

Specific Instructions . . . . . . . . . . . . . . . . . . . . . . . . . 3 Those reasons are listed below.

Checkboxes, Name, Taxpayer Identification • An abatement or refund of tax, other than income, estate, or

Number (TIN), and Address . . . . . . . . . . . . . . . 3 gift tax. Employers cannot use Form 843 to request an

Line Instructions: Lines 1 through 8 . . . . . . . . . . . 3 abatement of FICA tax, RRTA tax, or income tax withholding.

• An abatement or refund of tax, other than a tax for which a

Signature . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 different form must be used. (See Do not use Form 843 when

Paid Tax Return Preparer . . . . . . . . . . . . . . . . . . . 4 you must use a different tax form, later.)

Special Situations . . . . . . . . . . . . . . . . . . . . . . . . 4 • A refund to an employee of excess social security, Medicare,

Taxpayers With Visual Impairments and or RRTA tax withheld by any one employer but only if your

employer will not adjust the overcollection. See Refund of

Disabilities . . . . . . . . . . . . . . . . . . . . . . . . 4

Excess Social Security, Medicare, or RRTA Tax, later.

Refund of Excess Social Security, • A refund to an employee of excess tier 2 RRTA tax when, for

Medicare, or RRTA Tax . . . . . . . . . . . . . . . 4 the year, you had more than one railroad employer and your total

Excess Tier 2 RRTA Tax . . . . . . . . . . . . . . . . 4 tier 2 RRTA tax withheld or paid for the year was more than the

Refund of Social Security or Medicare tier 2 limit. See Excess Tier 2 RRTA Tax, later.

Tax Withheld in Error . . . . . . . . . . . . . . . . . 4 • A refund to an employee of social security, Medicare, or RRTA

tax that was withheld in error but only if your employer will not

Requesting Abatement or Refund of a adjust the overcollection. See Refund of Social Security and

Penalty or Addition to Tax as a Result Medicare Tax Withheld in Error, later. If you are a nonresident

of Written Advice . . . . . . . . . . . . . . . . . . . 4 alien, see Pub. 519, U.S. Tax Guide for Aliens, for specific

Requesting Abatement or Refund of instructions.

Interest Due to IRS Error or Delay • An abatement or refund of tier 1 RRTA tax for an employee

Under Section 6404(e)(1) . . . . . . . . . . . . . 5 representative.

• An abatement or refund of a penalty or addition to tax due to

Requesting Net Interest Rate of Zero on reasonable cause or other reason allowed under the law. (This

Overlapping Tax Underpayments and includes a request for a refund or an abatement of the section

Overpayments . . . . . . . . . . . . . . . . . . . . . 5 6676 penalty for an erroneous claim for refund, where the claim

Branded Prescription Drug Fee . . . . . . . . . . . 5 was due to reasonable cause. The penalty is assessed at 20% of

the amount determined to be excessive.)

• An abatement or refund of the penalty imposed under section

Future Developments 6672 for failure to collect and pay over tax, or attempt to evade or

For the latest information about developments related to Form defeat tax (Trust Fund Recovery Penalty).

843 and its instructions, such as legislation enacted after they • A refund of the penalty imposed under section 6695A for

were published, go to IRS.gov/Form843. misstatements due to incorrect appraisals.

• A refund of the penalty imposed under section 6715 for

misuse of dyed fuel.

What’s New • An abatement or refund under section 6404(f) of a penalty or

an addition to tax caused by certain erroneous written advice

Redesigned. We have redesigned Form 843 and these from the IRS. See Requesting Abatement or Refund of a Penalty

instructions. or Addition to Tax as a Result of Written Advice, later.

• An abatement or refund of interest due to IRS error or delay

General Instructions under section 6404(e)(1). See Requesting Abatement or Refund

of Interest Due to IRS Error or Delay Under Section 6404(e)(1),

Purpose of Form later.

Use Form 843 to claim a refund or request an abatement of

certain taxes, penalties, additions to tax, interest, and fees.

Instructions for Form 843 (Rev. 12-2024) Catalog Number 11200I

Dec 17, 2024 Department of the Treasury Internal Revenue Service www.irs.gov