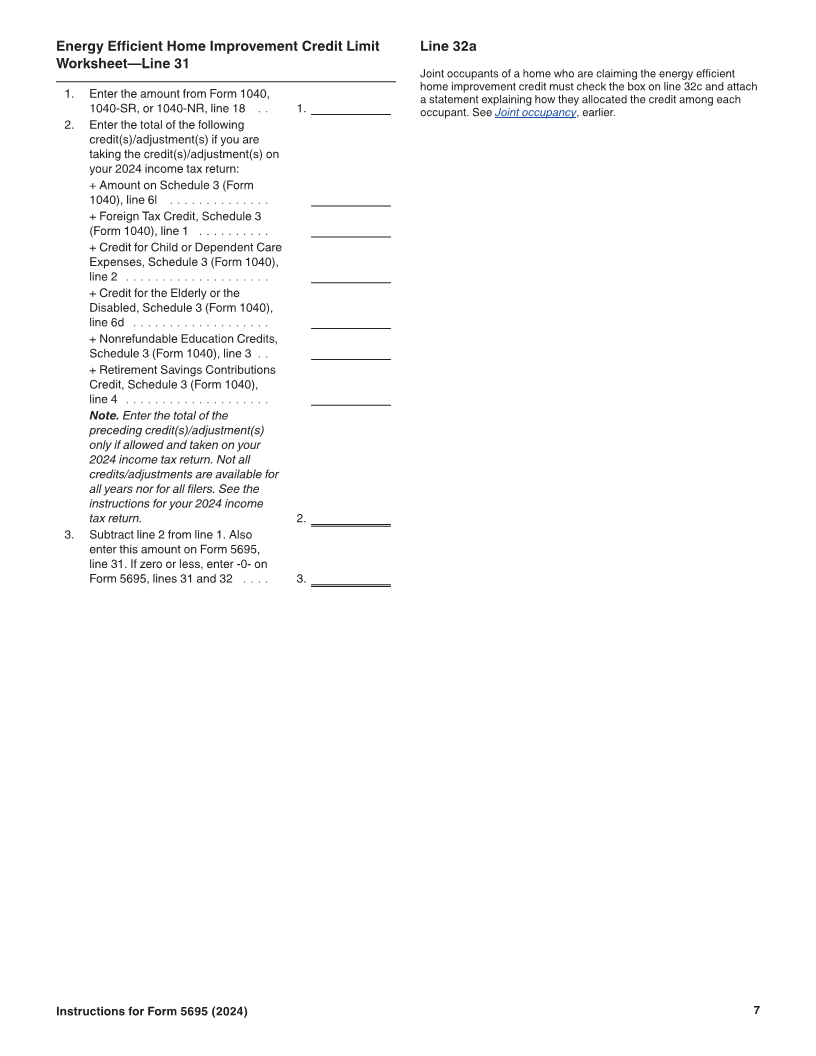

Enlarge image

Userid: CPM Schema: instrx Leadpct: 100% Pt. size: 8.5 Draft Ok to Print

AH XSL/XML Fileid: … -form-5695/2024/a/xml/cycle10/source (Init. & Date) _______

Page 1 of 7 12:24 - 29-Nov-2024

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

2024

Instructions for Form 5695

Residential Energy Credits

Section references are to the Internal Revenue Code unless property credits, see Fact Sheet 2024-15 at https://www.irs.gov/pub/

otherwise noted. taxpros/fs-2024-15.pdf.

Purpose of Form

General Instructions Use Form 5695 to figure and take your residential energy credits.

The residential energy credits are:

Future Developments • The residential clean energy credit, and

For the latest information about developments related to Form 5695 • The energy efficient home improvement credit.

and its instructions, such as legislation enacted after they were

published, go to IRS.gov/Form5695. Also use Form 5695 to take any residential clean energy credit

carryforward from 2023 or to carry the unused portion of the

residential clean energy credit to 2025.

What’s New

Home energy audits. Beginning January 1, 2024, home energy Who Can Take the Credits

audits must be performed by a Qualified Home Energy Auditor or You may be able to take the credits if you made energy saving

under the supervision of a Qualified Home Energy Auditor. The improvements to your home located in the United States in 2024.

Qualified Home Energy Auditor must be certified by a Qualified

Certification Program at the time of the home energy audit. See Home. A home is where you lived in 2024 and can include a house,

Lines 26a Through 26c, later for details. houseboat, mobile home, cooperative apartment, condominium, and

a manufactured home that conforms to Federal Manufactured Home

Reminders Construction and Safety Standards.

You must reduce the cost basis of your home if a residential

Residential clean energy credit. The residential energy efficient energy credit is allowed for any expense for any property. The

property credit is now the residential clean energy credit. The credit increase in the basis of the property that would result from the

rate for property placed in service in 2022 through 2032 is 30%. expenses will be reduced by the amount of the allowed credit.

The residential clean energy credit added a credit for qualified Main home. Your main home is generally the home where you live

battery storage technology. Battery storage technology costs are most of the time. A temporary absence due to special

allowed for the residential clean energy credit for expenses paid circumstances, such as illness, education, business, military service,

after December 31, 2022. See Qualified battery storage technology or vacation, won't change your main home.

costs, later, for details.

Biomass fuel property costs are no longer allowed for the Costs. For purposes of both credits, costs are treated as being paid

residential clean energy credit for property placed in service after when the original installation of the item is completed, or, in the case

December 31, 2022. of costs connected with the reconstruction of your home, when your

original use of the reconstructed home begins. For purposes of the

Energy efficient home improvement credit. The nonbusiness residential clean energy credit only, costs connected with the

energy property credit is now the energy efficient home improvement construction of a home are treated as being paid when your original

credit. The credit is extended to property placed in service through use of the constructed home begins. If less than 80% of the use of

December 31, 2032. an item is for nonbusiness purposes, only that portion of the costs

The energy efficient home improvement credit is now divided into that is allocable to the nonbusiness use can be used to determine

two sections to differentiate between qualified energy efficiency either credit.

improvements and residential energy property expenditures. The residential clean energy credit (Part I) is available for

For the energy efficient home improvement credit, the lifetime ! both existing homes and homes being constructed. The

limitation has been replaced by an annual credit limit. A 30% credit, CAUTION energy efficient home improvement credit (Part II) is only

up to a maximum of $1,200, may be allowed for: available for existing homes.

• Insulation material or air sealing material or systems;

• Exterior doors; IRS guidance issued with respect to the energy credit under

• Windows and skylights; ! section 48, such as Notice 2018-59 and Notice 2021-41,

• Central air conditioners; CAUTION does not apply to the residential energy credits.

• Natural gas, propane or oil water heaters;

• Natural gas, propane or oil furnaces or hot water boilers; Association or cooperative costs. If you are a member of a

• Improvements or replacement of panelboards, subpanelboards, condominium management association for a condominium you own

branch circuits or feeders; and or a tenant-stockholder in a cooperative housing corporation, you

• Home energy audits. are treated as having paid your proportionate share of any costs of

The limits for each category of these items that qualify for a credit is such association or corporation.

discussed later in Section A—Qualified Energy Efficiency If you received a subsidy from a public utility for the

Improvements. ! purchase or installation of an energy conservation product

Heat pumps and heat pump water heaters, biomass stoves and CAUTION and that subsidy wasn't included in your gross income, you

biomass boilers have a separate annual credit limit of $2,000 with no must reduce your cost for the product by the amount of that subsidy

lifetime limitation, which replaces the prior lifetime limitation of $500. before you figure your credit. This rule also applies if a third party

(such as a contractor) receives the subsidy on your behalf. See Fact

For additional information and frequently asked questions about Sheet 2024-15 at https://www.irs.gov/pub/taxpros/fs-2024-15.pdf,

energy efficient home improvements and residential clean energy for details.

Instructions for Form 5695 (2024) Catalog Number 66412G

Nov 29, 2024 Department of the Treasury Internal Revenue Service www.irs.gov