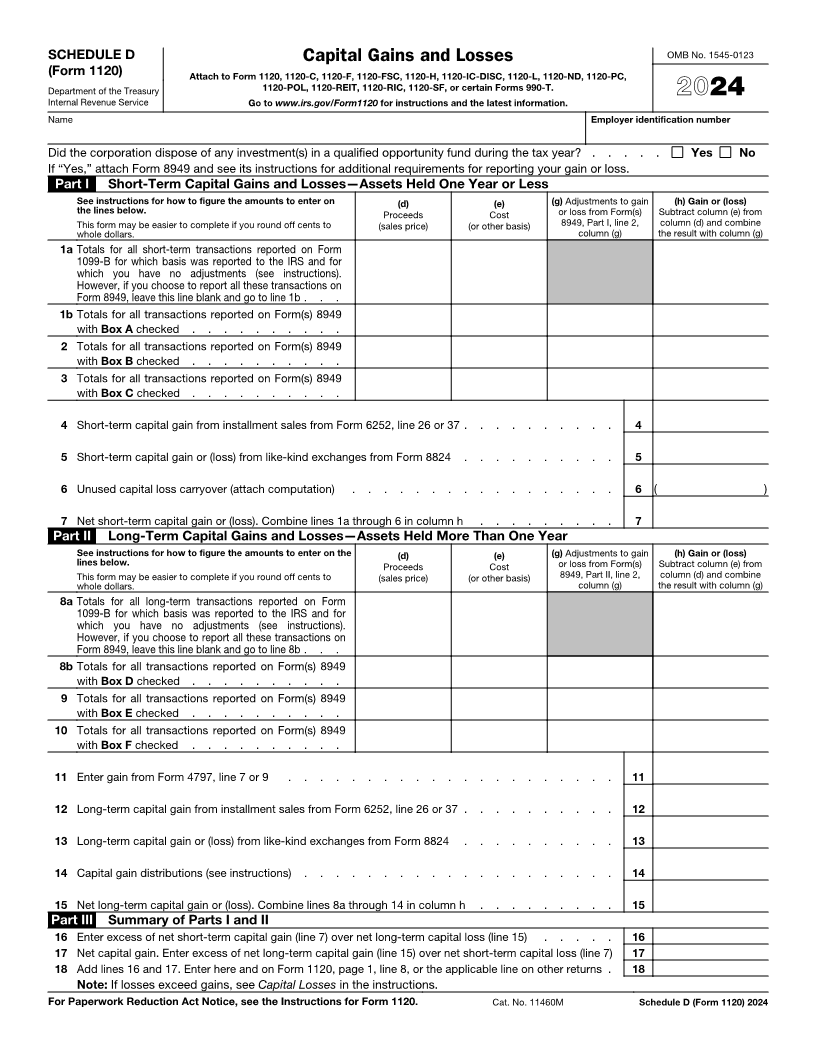

Enlarge image

SCHEDULE D Capital Gains and Losses OMB No. 1545-0123

(Form 1120) Attach to Form 1120, 1120-C, 1120-F, 1120-FSC, 1120-H, 1120-IC-DISC, 1120-L, 1120-ND, 1120-PC,

Department of the Treasury 1120-POL, 1120-REIT, 1120-RIC, 1120-SF, or certain Forms 990-T.

Internal Revenue Service Go to www.irs.gov/Form1120 for instructions and the latest information. 2024

Name Employer identification number

Did the corporation dispose of any investment(s) in a qualified opportunity fund during the tax year? . . . . . Yes No

If “Yes,” attach Form 8949 and see its instructions for additional requirements for reporting your gain or loss.

Part I Short-Term Capital Gains and Losses—Assets Held One Year or Less

See instructions for how to figure the amounts to enter on (d) (e) (g) Adjustments to gain (h) Gain or (loss)

the lines below. Proceeds Cost or loss from Form(s) Subtract column (e) from

This form may be easier to complete if you round off cents to (sales price) (or other basis) 8949, Part I, line 2, column (d) and combine

whole dollars. column (g) the result with column (g)

1a Totals for all short-term transactions reported on Form

1099-B for which basis was reported to the IRS and for

which you have no adjustments (see instructions).

However, if you choose to report all these transactions on

Form 8949, leave this line blank and go to line 1b . . .

1b Totals for all transactions reported on Form(s) 8949

with Box A checked . . . . . . . . . .

2 Totals for all transactions reported on Form(s) 8949

with Box B checked . . . . . . . . . .

3 Totals for all transactions reported on Form(s) 8949

with Box C checked . . . . . . . . . .

4 Short-term capital gain from installment sales from Form 6252, line 26 or 37 . . . . . . . . . . 4

5 Short-term capital gain or (loss) from like-kind exchanges from Form 8824 . . . . . . . . . . 5

6 Unused capital loss carryover (attach computation) . . . . . . . . . . . . . . . . . 6 ( )

7 Net short-term capital gain or (loss). Combine lines 1a through 6 in column h . . . . . . . . . 7

Part II Long-Term Capital Gains and Losses—Assets Held More Than One Year

See instructions for how to figure the amounts to enter on the (d) (e) (g) Adjustments to gain (h) Gain or (loss)

lines below. Proceeds Cost or loss from Form(s) Subtract column (e) from

This form may be easier to complete if you round off cents to (sales price) (or other basis) 8949, Part II, line 2, column (d) and combine

whole dollars. column (g) the result with column (g)

8a Totals for all long-term transactions reported on Form

1099-B for which basis was reported to the IRS and for

which you have no adjustments (see instructions).

However, if you choose to report all these transactions on

Form 8949, leave this line blank and go to line 8b . . .

8b Totals for all transactions reported on Form(s) 8949

with Box D checked . . . . . . . . . .

9 Totals for all transactions reported on Form(s) 8949

with Box E checked . . . . . . . . . .

10 Totals for all transactions reported on Form(s) 8949

with Box F checked . . . . . . . . . .

11 Enter gain from Form 4797, line 7 or 9 . . . . . . . . . . . . . . . . . . . . . 11

12 Long-term capital gain from installment sales from Form 6252, line 26 or 37 . . . . . . . . . . 12

13 Long-term capital gain or (loss) from like-kind exchanges from Form 8824 . . . . . . . . . . 13

14 Capital gain distributions (see instructions) . . . . . . . . . . . . . . . . . . . . 14

15 Net long-term capital gain or (loss). Combine lines 8a through 14 in column h . . . . . . . . . 15

Part III Summary of Parts I and II

16 Enter excess of net short-term capital gain (line 7) over net long-term capital loss (line 15) . . . . . 16

17 Net capital gain. Enter excess of net long-term capital gain (line 15) over net short-term capital loss (line 7) 17

18 Add lines 16 and 17. Enter here and on Form 1120, page 1, line 8, or the applicable line on other returns . 18

Note: If losses exceed gains, see Capital Losses in the instructions.

For Paperwork Reduction Act Notice, see the Instructions for Form 1120. Cat. No. 11460M Schedule D (Form 1120) 2024