Enlarge image

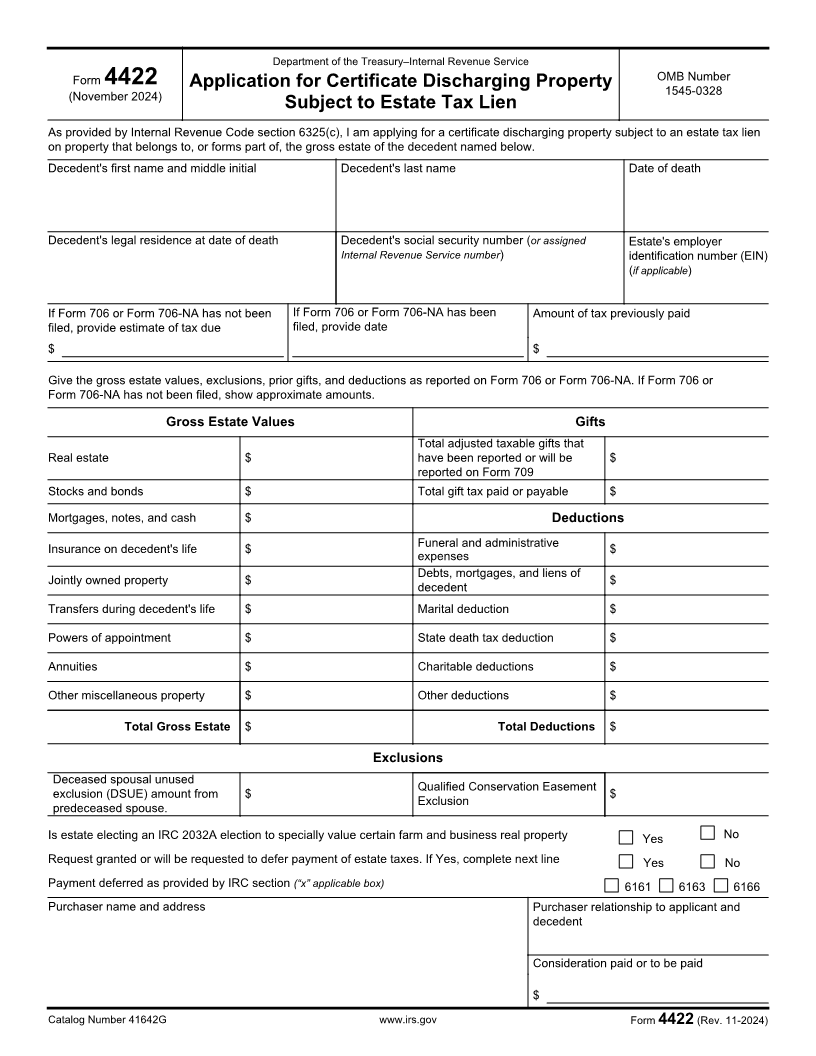

Department of the Treasury–Internal Revenue Service

OMB Number

Form 4422 Application for Certificate Discharging Property 1545-0328

(November 2024)

Subject to Estate Tax Lien

As provided by Internal Revenue Code section 6325(c), I am applying for a certificate discharging property subject to an estate tax lien

on property that belongs to, or forms part of, the gross estate of the decedent named below.

Decedent's first name and middle initial Decedent's last name Date of death

Decedent's legal residence at date of death Decedent's social security number (or assigned Estate's employer

Internal Revenue Service number) identification number (EIN)

(if applicable)

If Form 706 or Form 706-NA has not been If Form 706 or Form 706-NA has been Amount of tax previously paid

filed, provide estimate of tax due filed, provide date

$ $

Give the gross estate values, exclusions, prior gifts, and deductions as reported on Form 706 or Form 706-NA. If Form 706 or

Form 706-NA has not been filed, show approximate amounts.

Gross Estate Values Gifts

Total adjusted taxable gifts that

Real estate $ have been reported or will be $

reported on Form 709

Stocks and bonds $ Total gift tax paid or payable $

Mortgages, notes, and cash $ Deductions

Insurance on decedent's life $ Funeral and administrative $

expenses

Debts, mortgages, and liens of

Jointly owned property $ $

decedent

Transfers during decedent's life $ Marital deduction $

Powers of appointment $ State death tax deduction $

Annuities $ Charitable deductions $

Other miscellaneous property $ Other deductions $

Total Gross Estate $ Total Deductions $

Exclusions

Deceased spousal unused

Qualified Conservation Easement

exclusion (DSUE) amount from $ $

Exclusion

predeceased spouse.

Is estate electing an IRC 2032A election to specially value certain farm and business real property Yes No

Request granted or will be requested to defer payment of estate taxes. If Yes, complete next line Yes No

Payment deferred as provided by IRC section (“x” applicable box) 6161 6163 6166

Purchaser name and address Purchaser relationship to applicant and

decedent

Consideration paid or to be paid

$

Catalog Number 41642G www.irs.gov Form 4422 (Rev. 11-2024)