Enlarge image

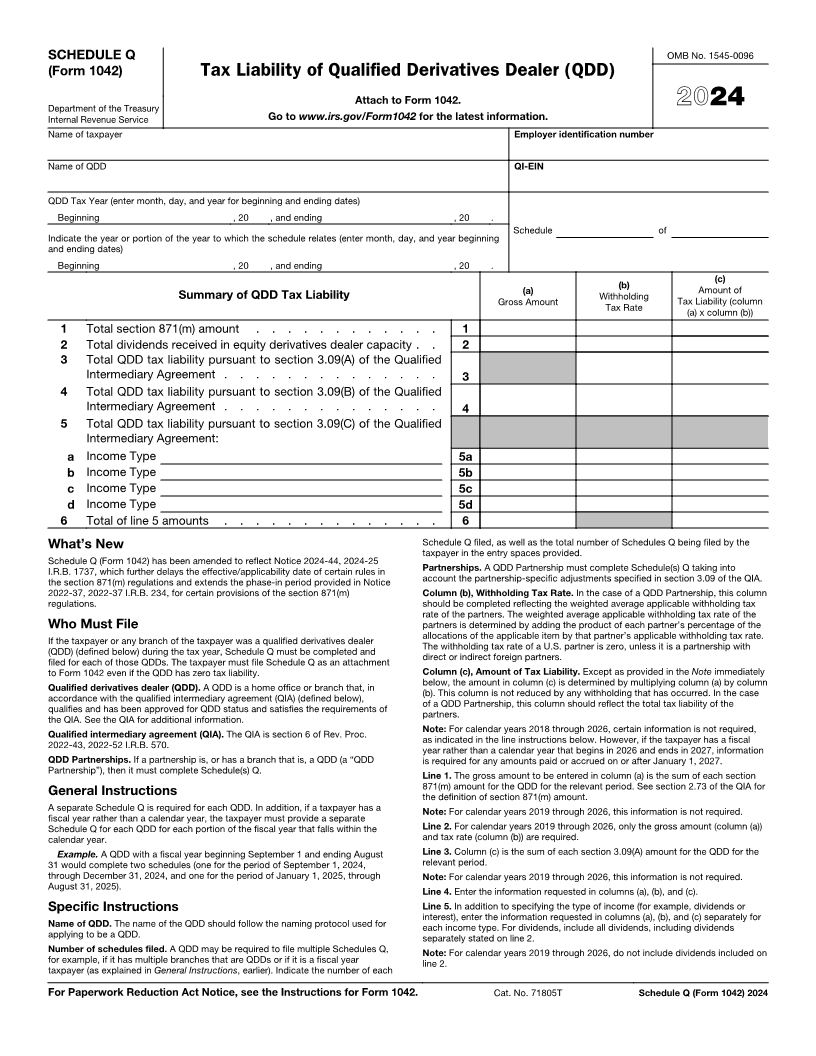

SCHEDULE Q OMB No. 1545-0096

(Form 1042) Tax Liability of Qualified Derivatives Dealer (QDD)

Attach to Form 1042.

Department of the Treasury 2024

Internal Revenue Service Go to www.irs.gov/Form1042 for the latest information.

Name of taxpayer Employer identification number

Name of QDD QI-EIN

QDD Tax Year (enter month, day, and year for beginning and ending dates)

Beginning , 20 , and ending , 20 .

Schedule of

Indicate the year or portion of the year to which the schedule relates (enter month, day, and year beginning

and ending dates)

Beginning , 20 , and ending , 20 .

Summary of QDD Tax Liability (a) (b) (c)

Gross Amount Withholding Amount of

Tax Rate Tax Liability (column

(a) x column (b))

1 Total section 871(m) amount . . . . . . . . . . . . 1

2 Total dividends received in equity derivatives dealer capacity . . 2

3 Total QDD tax liability pursuant to section 3.09(A) of the Qualified

Intermediary Agreement . . . . . . . . . . . . . . 3

4 Total QDD tax liability pursuant to section 3.09(B) of the Qualified

Intermediary Agreement . . . . . . . . . . . . . . 4

5 Total QDD tax liability pursuant to section 3.09(C) of the Qualified

Intermediary Agreement:

a Income Type 5a

b Income Type 5b

c Income Type 5c

d Income Type 5d

6 Total of line 5 amounts . . . . . . . . . . . . . . 6

What’s New Schedule Q filed, as well as the total number of Schedules Q being filed by the

taxpayer in the entry spaces provided.

Schedule Q (Form 1042) has been amended to reflect Notice 2024-44, 2024-25 A QDD Partnership must complete Schedule(s) Q taking into

I.R.B. 1737, which further delays the effective/applicability date of certain rules in Partnerships.

the section 871(m) regulations and extends the phase-in period provided in Notice account the partnership-specific adjustments specified in section 3.09 of the QIA.

2022-37, 2022-37 I.R.B. 234, for certain provisions of the section 871(m) Column (b), Withholding Tax Rate. In the case of a QDD Partnership, this column

regulations. should be completed reflecting the weighted average applicable withholding tax

rate of the partners. The weighted average applicable withholding tax rate of the

Who Must File partners is determined by adding the product of each partner’s percentage of the

If the taxpayer or any branch of the taxpayer was a qualified derivatives dealer allocations of the applicable item by that partner’s applicable withholding tax rate.

(QDD) (defined below) during the tax year, Schedule Q must be completed and The withholding tax rate of a U.S. partner is zero, unless it is a partnership with

filed for each of those QDDs. The taxpayer must file Schedule Q as an attachment direct or indirect foreign partners.

to Form 1042 even if the QDD has zero tax liability. Column (c), Amount of Tax Liability. Except as provided in the Note immediately

Qualified derivatives dealer (QDD). A QDD is a home office or branch that, in below, the amount in column (c) is determined by multiplying column (a) by column

accordance with the qualified intermediary agreement (QIA) (defined below), (b). This column is not reduced by any withholding that has occurred. In the case

qualifies and has been approved for QDD status and satisfies the requirements of of a QDD Partnership, this column should reflect the total tax liability of the

the QIA. See the QIA for additional information. partners.

Qualified intermediary agreement (QIA). The QIA is section 6 of Rev. Proc. Note: For calendar years 2018 through 2026, certain information is not required,

2022-43, 2022-52 I.R.B. 570. as indicated in the line instructions below. However, if the taxpayer has a fiscal

year rather than a calendar year that begins in 2026 and ends in 2027, information

QDD Partnerships. If a partnership is, or has a branch that is, a QDD (a “QDD is required for any amounts paid or accrued on or after January 1, 2027.

Partnership”), then it must complete Schedule(s) Q. Line 1. The gross amount to be entered in column (a) is the sum of each section

General Instructions 871(m) amount for the QDD for the relevant period. See section 2.73 of the QIA for

the definition of section 871(m) amount.

A separate Schedule Q is required for each QDD. In addition, if a taxpayer has a Note: For calendar years 2019 through 2026, this information is not required.

fiscal year rather than a calendar year, the taxpayer must provide a separate

Schedule Q for each QDD for each portion of the fiscal year that falls within the Line 2. For calendar years 2019 through 2026, only the gross amount (column (a))

calendar year. and tax rate (column (b)) are required.

Example. A QDD with a fiscal year beginning September 1 and ending August Line 3. Column (c) is the sum of each section 3.09(A) amount for the QDD for the

31 would complete two schedules (one for the period of September 1, 2024, relevant period.

through December 31, 2024, and one for the period of January 1, 2025, through Note: For calendar years 2019 through 2026, this information is not required.

August 31, 2025). Line 4. Enter the information requested in columns (a), (b), and (c).

Specific Instructions Line 5. In addition to specifying the type of income (for example, dividends or

interest), enter the information requested in columns (a), (b), and (c) separately for

Name of QDD. The name of the QDD should follow the naming protocol used for each income type. For dividends, include all dividends, including dividends

applying to be a QDD. separately stated on line 2.

Number of schedules filed. A QDD may be required to file multiple Schedules Q, Note: For calendar years 2019 through 2026, do not include dividends included on

for example, if it has multiple branches that are QDDs or if it is a fiscal year line 2.

taxpayer (as explained in General Instructions, earlier). Indicate the number of each

For Paperwork Reduction Act Notice, see the Instructions for Form 1042. Cat. No. 71805T Schedule Q (Form 1042) 2024