Enlarge image

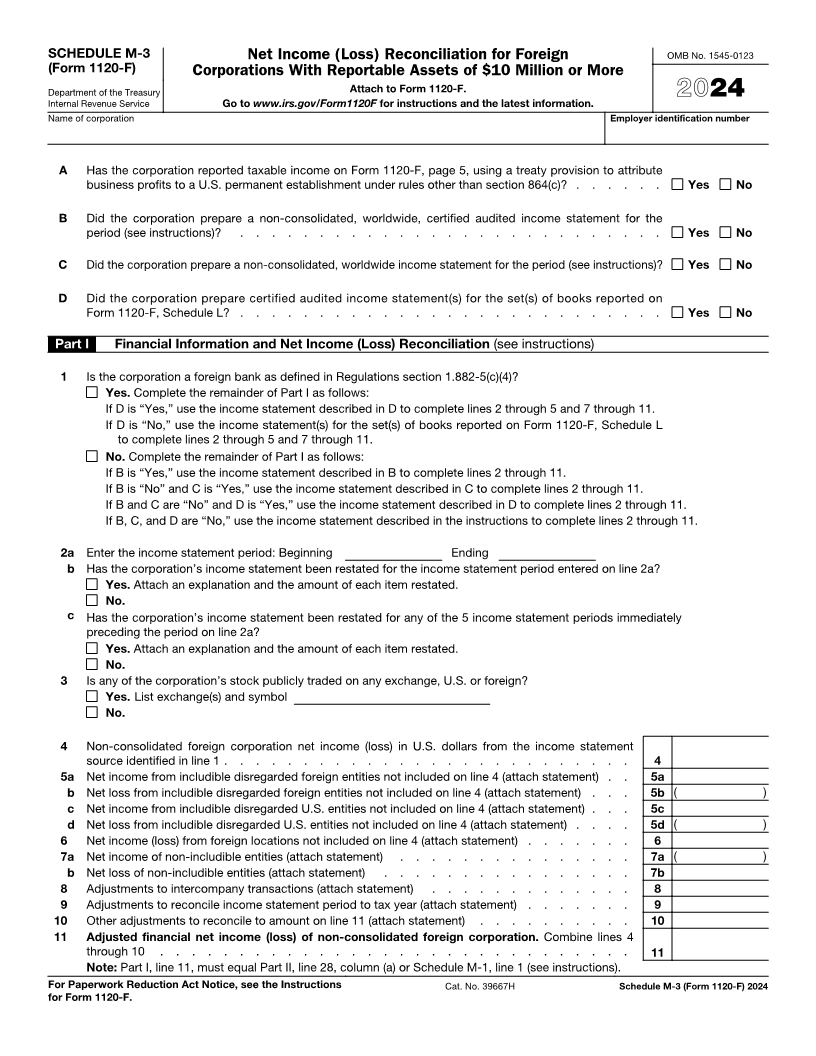

SCHEDULE M-3 Net Income (Loss) Reconciliation for Foreign OMB No. 1545-0123 (Form 1120-F) Corporations With Reportable Assets of $10 Million or More Department of the Treasury Attach to Form 1120-F. Internal Revenue Service Go to www.irs.gov/Form1120F for instructions and the latest information. 2024 Name of corporation Employer identification number A Has the corporation reported taxable income on Form 1120-F, page 5, using a treaty provision to attribute business profits to a U.S. permanent establishment under rules other than section 864(c)? . . . . . . Yes No B Did the corporation prepare a non-consolidated, worldwide, certified audited income statement for the period (see instructions)? . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No C Did the corporation prepare a non-consolidated, worldwide income statement for the period (see instructions)? Yes No D Did the corporation prepare certified audited income statement(s) for the set(s) of books reported on Form 1120-F, Schedule L? . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes No Part I Financial Information and Net Income (Loss) Reconciliation (see instructions) 1 Is the corporation a foreign bank as defined in Regulations section 1.882-5(c)(4)? Yes. Complete the remainder of Part I as follows: If D is “Yes,” use the income statement described in D to complete lines 2 through 5 and 7 through 11. If D is “No,” use the income statement(s) for the set(s) of books reported on Form 1120-F, Schedule L to complete lines 2 through 5 and 7 through 11. No. Complete the remainder of Part I as follows: If B is “Yes,” use the income statement described in B to complete lines 2 through 11. If B is “No” and C is “Yes,” use the income statement described in C to complete lines 2 through 11. If B and C are “No” and D is “Yes,” use the income statement described in D to complete lines 2 through 11. If B, C, and D are “No,” use the income statement described in the instructions to complete lines 2 through 11. 2a Enter the income statement period: Beginning Ending b Has the corporation’s income statement been restated for the income statement period entered on line 2a? Yes. Attach an explanation and the amount of each item restated. No. c Has the corporation’s income statement been restated for any of the 5 income statement periods immediately preceding the period on line 2a? Yes. Attach an explanation and the amount of each item restated. No. 3 Is any of the corporation’s stock publicly traded on any exchange, U.S. or foreign? Yes. List exchange(s) and symbol No. 4 Non-consolidated foreign corporation net income (loss) in U.S. dollars from the income statement source identified in line 1 . . . . . . . . . . . . . . . . . . . . . . . . . . 4 5a Net income from includible disregarded foreign entities not included on line 4 (attach statement) . . 5a b Net loss from includible disregarded foreign entities not included on line 4 (attach statement) . . . 5b ( ) c Net income from includible disregarded U.S. entities not included on line 4 (attach statement) . . . 5c d Net loss from includible disregarded U.S. entities not included on line 4 (attach statement) . . . . 5d ( ) 6 Net income (loss) from foreign locations not included on line 4 (attach statement) . . . . . . . 6 7a Net income of non-includible entities (attach statement) . . . . . . . . . . . . . . . 7a ( ) b Net loss of non-includible entities (attach statement) . . . . . . . . . . . . . . . . 7b 8 Adjustments to intercompany transactions (attach statement) . . . . . . . . . . . . . 8 9 Adjustments to reconcile income statement period to tax year (attach statement) . . . . . . . 9 10 Other adjustments to reconcile to amount on line 11 (attach statement) . . . . . . . . . . 10 11 Adjusted financial net income (loss) of non-consolidated foreign corporation. Combine lines 4 through 10 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11 Note: Part I, line 11, must equal Part II, line 28, column (a) or Schedule M-1, line 1 (see instructions). For Paperwork Reduction Act Notice, see the Instructions Cat. No. 39667H Schedule M-3 (Form 1120-F) 2024 for Form 1120-F.