Enlarge image

*244411*

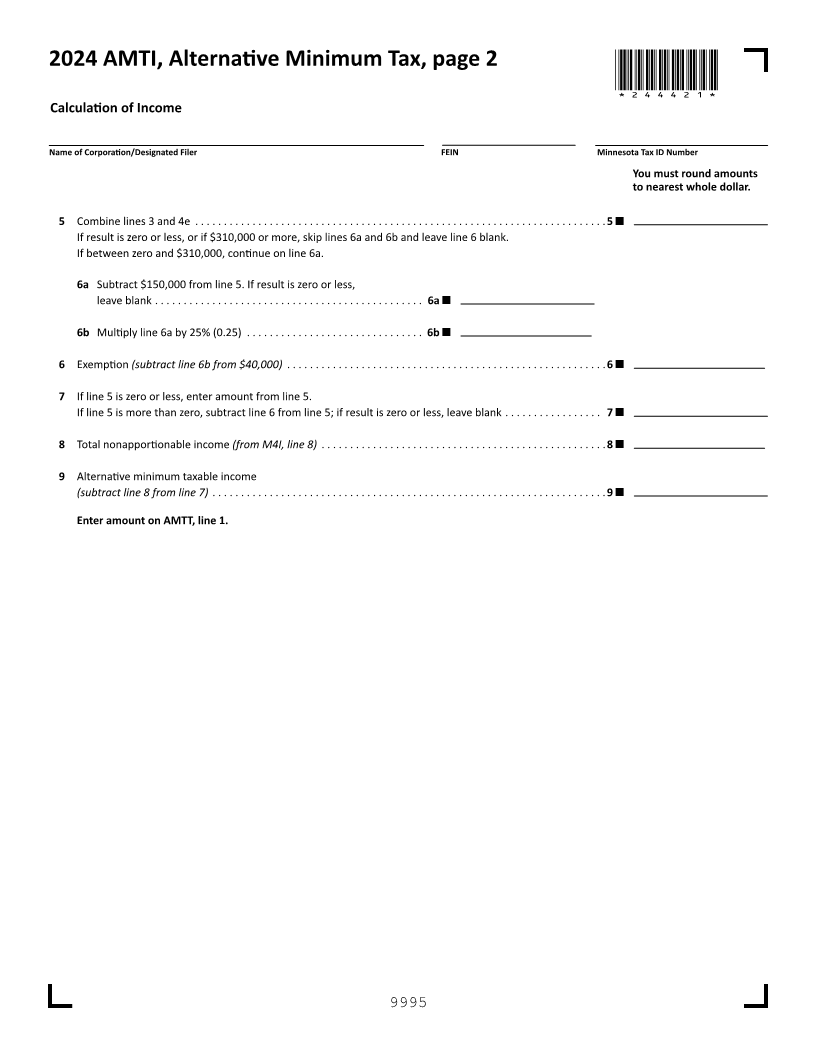

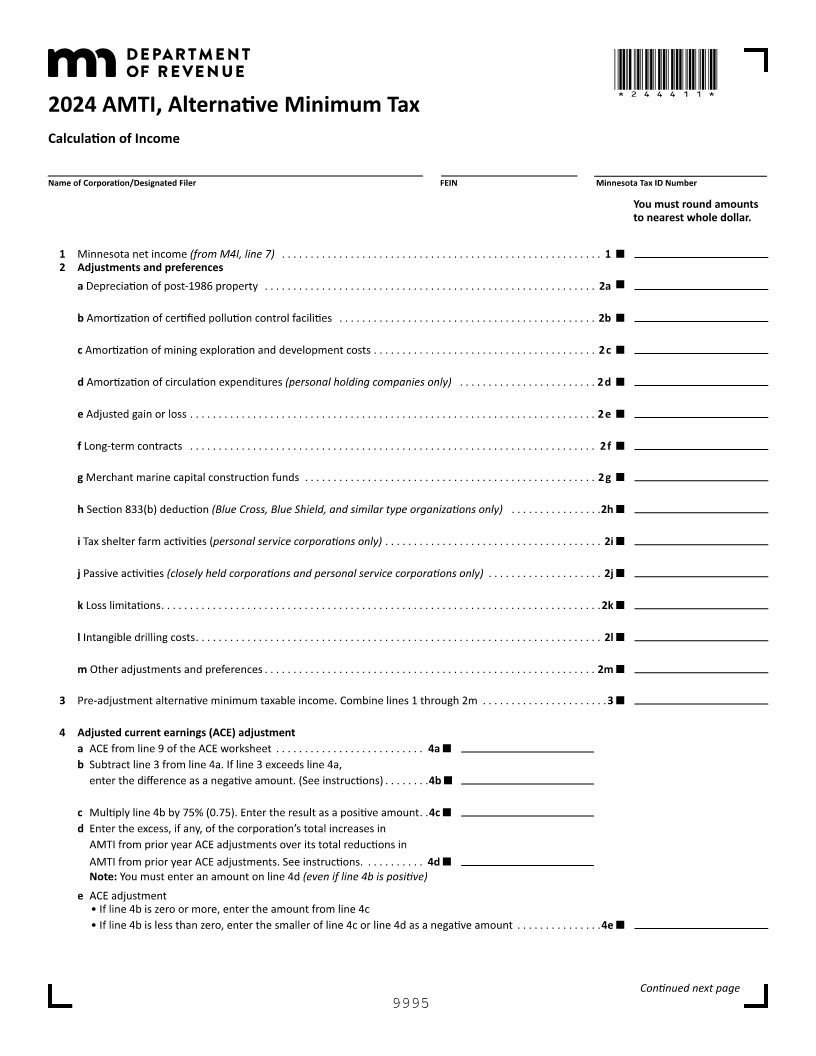

2024 AMTI Alternative Minimum Tax ,

Calculation of Income

Name of Corporation/Designated Filer FEIN Minnesota Tax ID Number

You must round amounts

to nearest whole dollar.

1 Minnesota net income (from M4I, line 7) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2 Adjustments and preferences

a Depreciation of post-1986 property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2a

b Amortization of certified pollution control facilities . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2b

c Amortization of mining exploration and development costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2c

d Amortization of circulation expenditures (personal holding companies only) . . . . . . . . . . . . . . . . . . . . . . . . 2d

e Adjusted gain or loss . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2e

f Long-term contracts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2f

g Merchant marine capital construction funds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2g

hSection 833(b) deduction (Blue Cross, Blue Shield, and similar type organizations only) . . . . . . . . . . . . . . 2h. .

i Tax shelter farm activities (personal service corporations only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2i

j Passive activities (closely held corporations and personal service corporations only) . . . . . . . . . . . . . . . . . . . . 2j

k Loss limitations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2k

l Intangible drilling costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2l

m Other adjustments and preferences . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2m

3 Pre-adjustment alternative minimum taxable income. Combine lines 1 through 2m . . . . . . . . . . . . . . . . . . . . . . 3

4 Adjusted current earnings (ACE) adjustment

a ACE from line 9 of the ACE worksheet . . . . . . . . . . . . . . . . . . . . . . . . . . 4a

b Subtract line 3 from line 4a. If line 3 exceeds line 4a,

enter the difference as a negative amount. (See instructions) . . . . . . . .4b

c Multiply line 4b by 75% (0.75). Enter the result as a positive amount . .4c

d Enter the excess, if any, of the corporation’s total increases in

AMTI from prior year ACE adjustments over its total reductions in

AMTI from prior year ACE adjustments. See instructions. . . . . . . . . . . 4d

Note: You must enter an amount on line 4d (even if line 4b is positive)

e ACE adjustment

• If line 4b is zero or more, enter the amount from line 4c

• If line 4b is less than zero, enter the smaller of line 4c or line 4d as a negative amount . . . . . . . . . . . . . . .4e

Continued next page

9995