Enlarge image

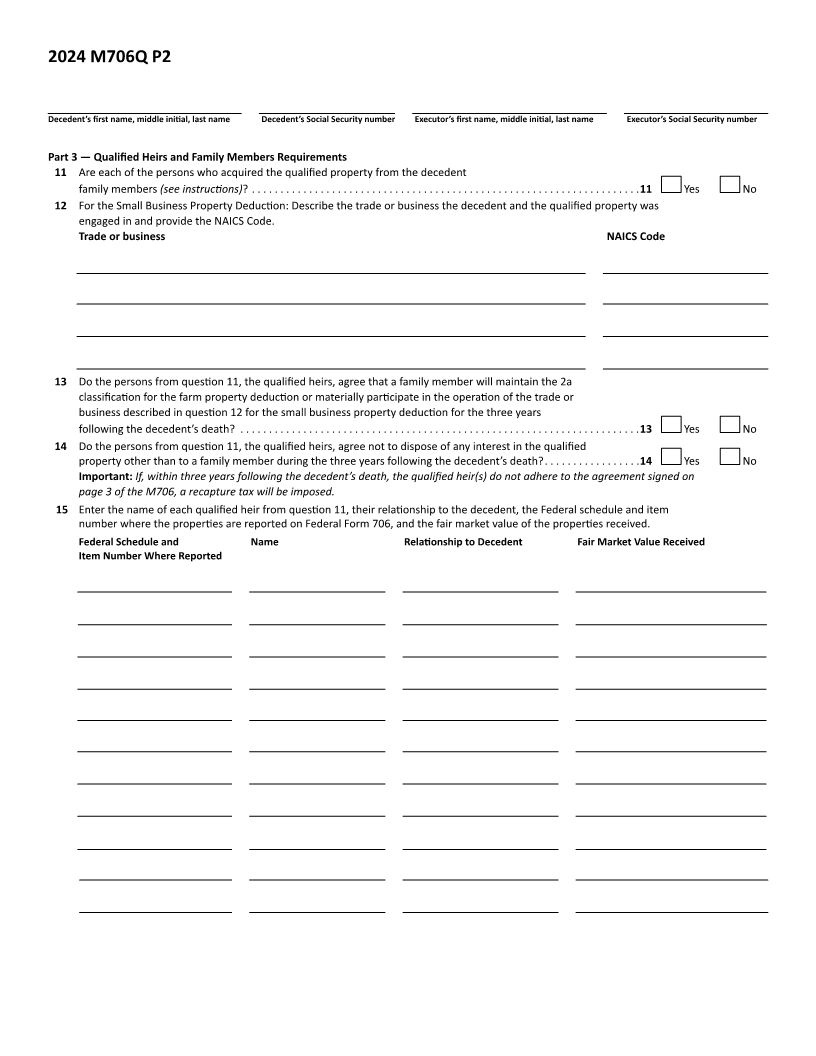

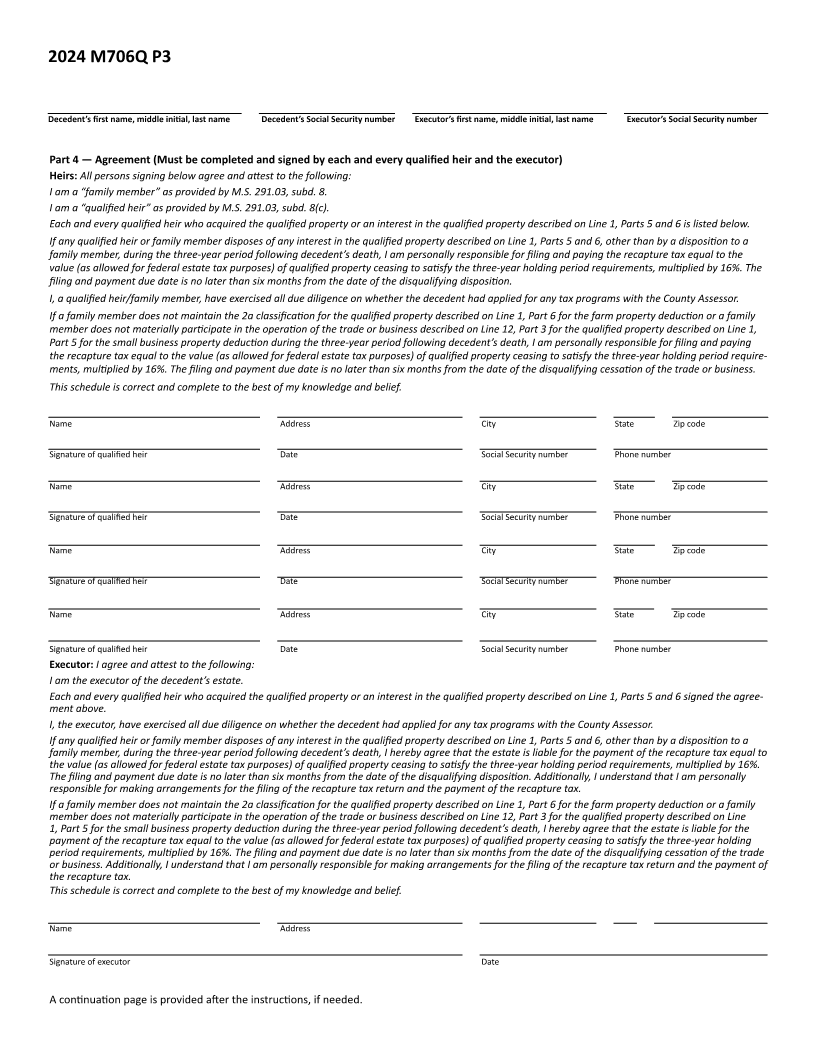

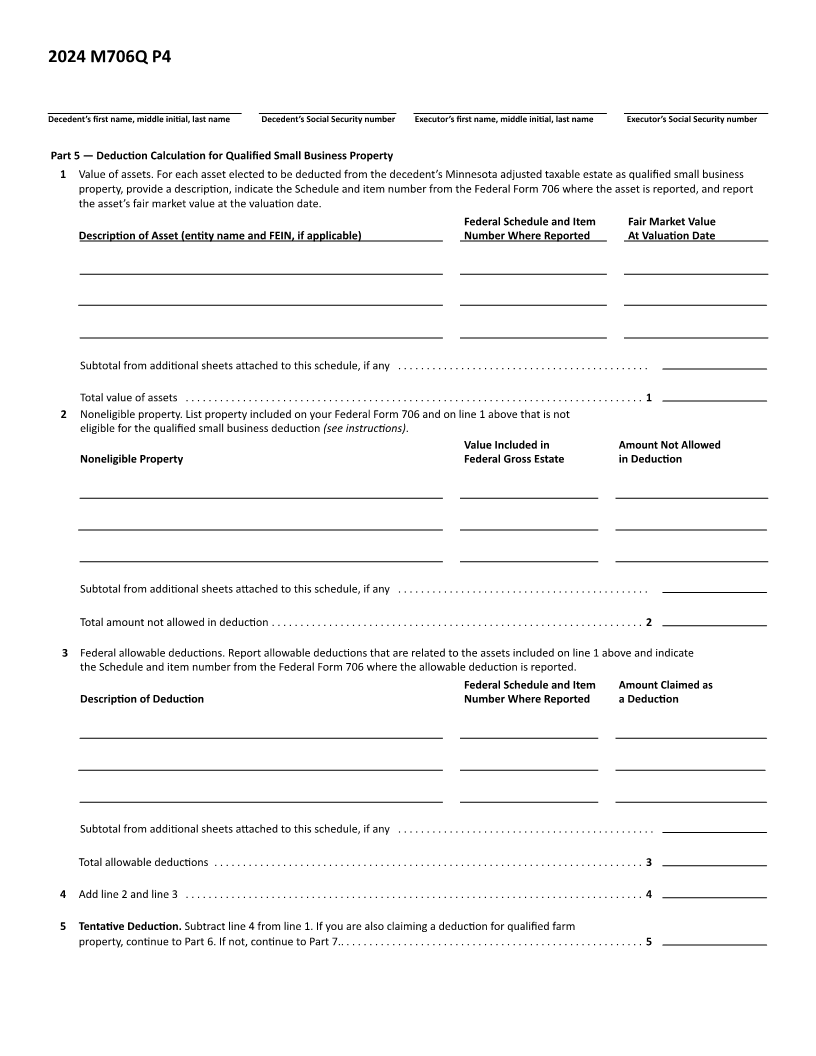

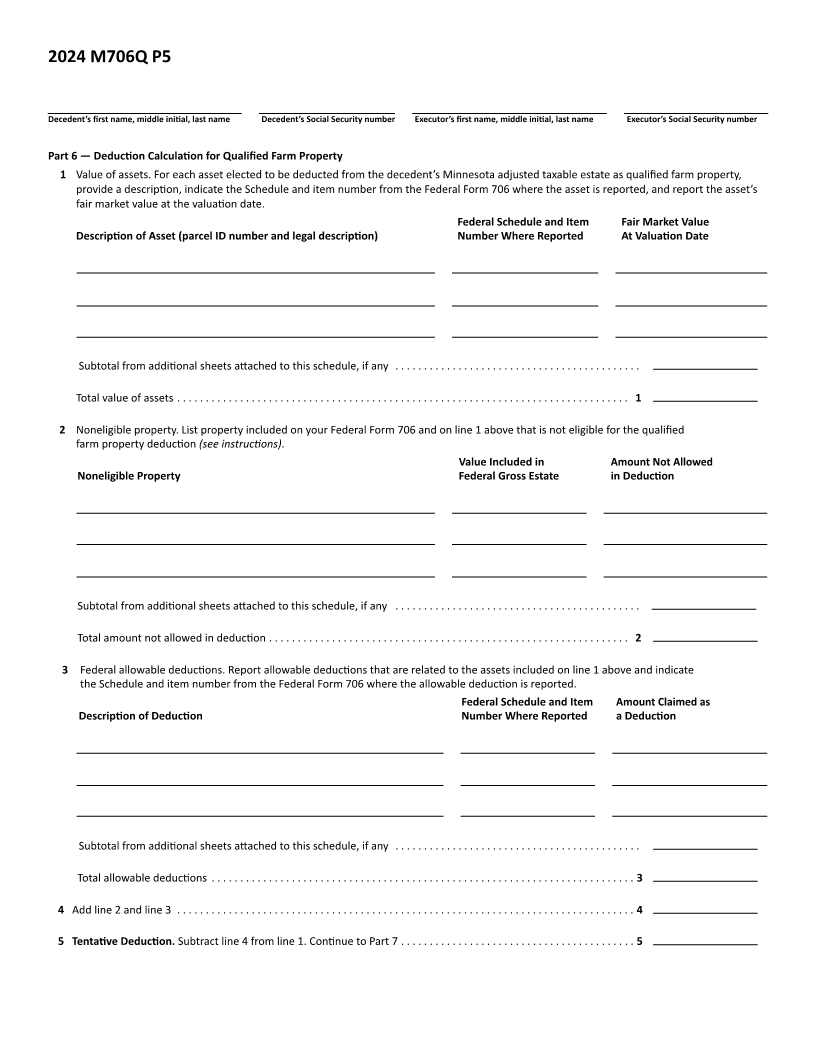

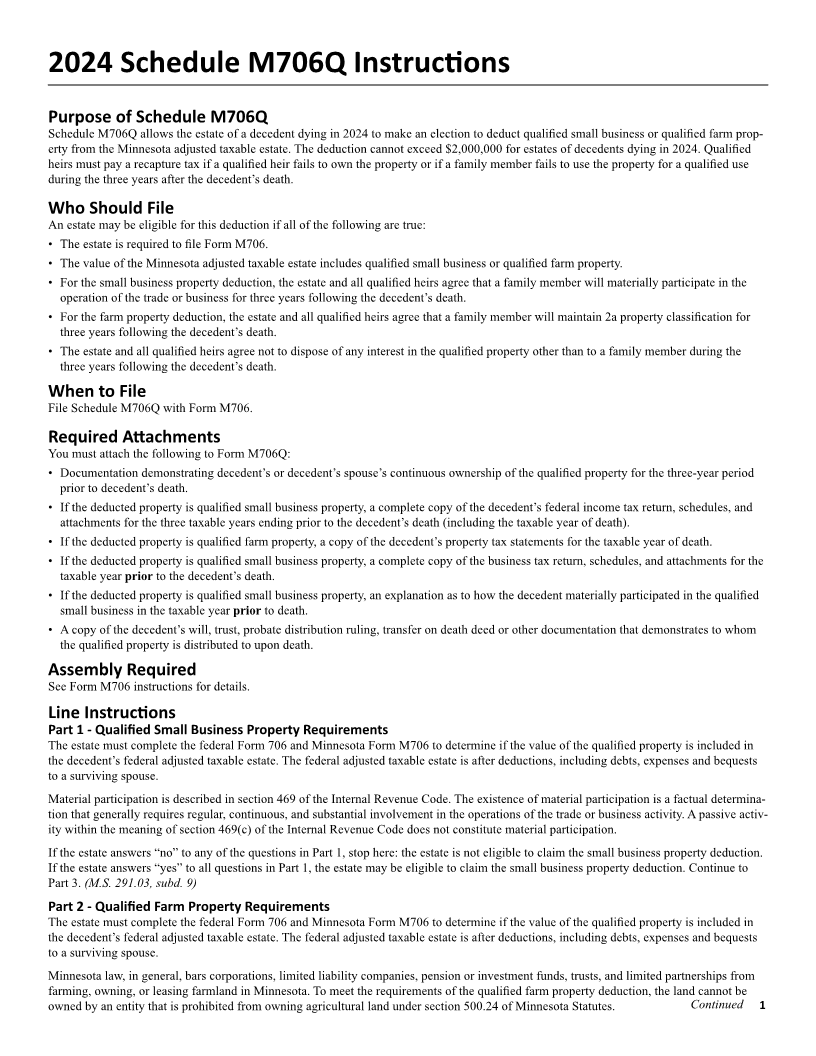

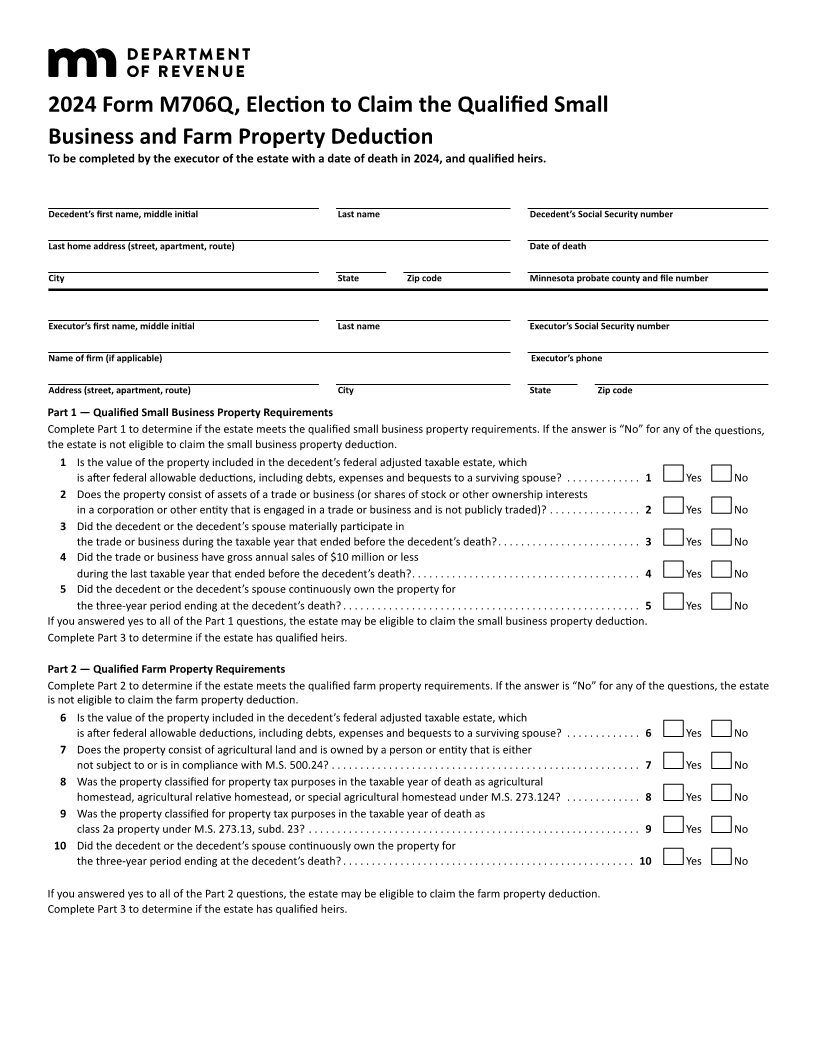

2024 Form M706Q, Election to Claim the Qualified Small Business and Farm Property Deduction To be completed by the executor of the estate with a date of death in 2024, and qualified heirs. Decedent’s first name, middle initial Last name Decedent’s Social Security number Last home address (street, apartment, route) Date of death City State Zip code Minnesota probate county and file number Executor’s first name, middle initial Last name Executor’s Social Security number Name of firm (if applicable) Executor’s phone Address (street, apartment, route) City State Zip code Part 1 — Qualified Small Business Property Requirements Complete Part 1 to determine if the estate meets the qualified small business property requirements. If the answer is “No” for any of the questions, the estate is not eligible to claim the small business property deduction. 1 Is the value of the property included in the decedent’s federal adjusted taxable estate, which is after federal allowable deductions, including debts, expenses and bequests to a surviving spouse? . ...... ..... . 1 Yes No 2 Does the property consist of assets of a trade or business (or shares of stock or other ownership interests in a corporation or other entity that is engaged in a trade or business and is not publicly traded)? ... ..... ...... .. 2 Yes No 3 Did the decedent or the decedent’s spouse materially participate in the trade or business during the taxable year that ended before the decedent’s death?... ...... ..... ....... .... 3 Yes No 4 Did the trade or business have gross annual sales of $10 million or less during the last taxable year that ended before the decedent’s death?... ...... ..... ....... ..... ...... ..... ... 4 Yes No 5 Did the decedent or the decedent’s spouse continuously own the property for the three-year period ending at the decedent’s death? ... ...... ..... ....... ..... ...... ..... ..... ...... .... 5 Yes No If you answered yes to all of the Part 1 questions, the estate may be eligible to claim the small business property deduction. Complete Part 3 to determine if the estate has qualified heirs. Part 2 — Qualified Farm Property Requirements Complete Part 2 to determine if the estate meets the qualified farm property requirements. If the answer is “No” for any of the questions, the estate is not eligible to claim the farm property deduction. 6 Is the value of the property included in the decedent’s federal adjusted taxable estate, which is after federal allowable deductions, including debts, expenses and bequests to a surviving spouse? . ...... ..... . 6 Yes No 7 Does the property consist of agricultural land and is owned by a person or entity that is either not subject to or is in compliance with M.S. 500.24? .... ...... ...... ..... ..... ...... ...... ...... ...... .... 7 Yes No 8 Was the property classified for property tax purposes in the taxable year of death as agricultural homestead, agricultural relative homestead, or special agricultural homestead under M.S. 273.124? ..... ...... .. 8 Yes No 9 Was the property classified for property tax purposes in the taxable year of death as class 2a property under M.S. 273.13, subd. 23? ...... ..... ...... ..... ....... ..... ..... ...... ..... ...... .. 9 Yes No 10 Did the decedent or the decedent’s spouse continuously own the property for the three-year period ending at the decedent’s death? ... ...... ..... ....... ..... ...... ..... ..... ...... ... 10 Yes No If you answered yes to all of the Part 2 questions, the estate may be eligible to claim the farm property deduction. Complete Part 3 to determine if the estate has qualified heirs.