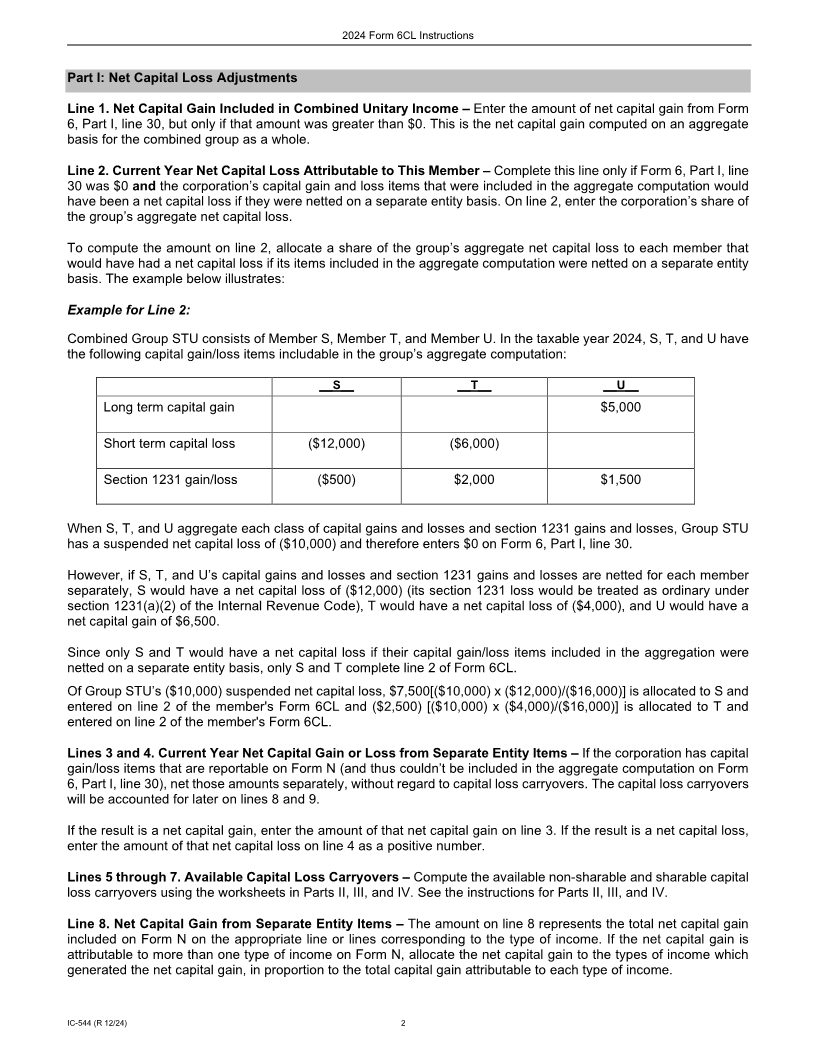

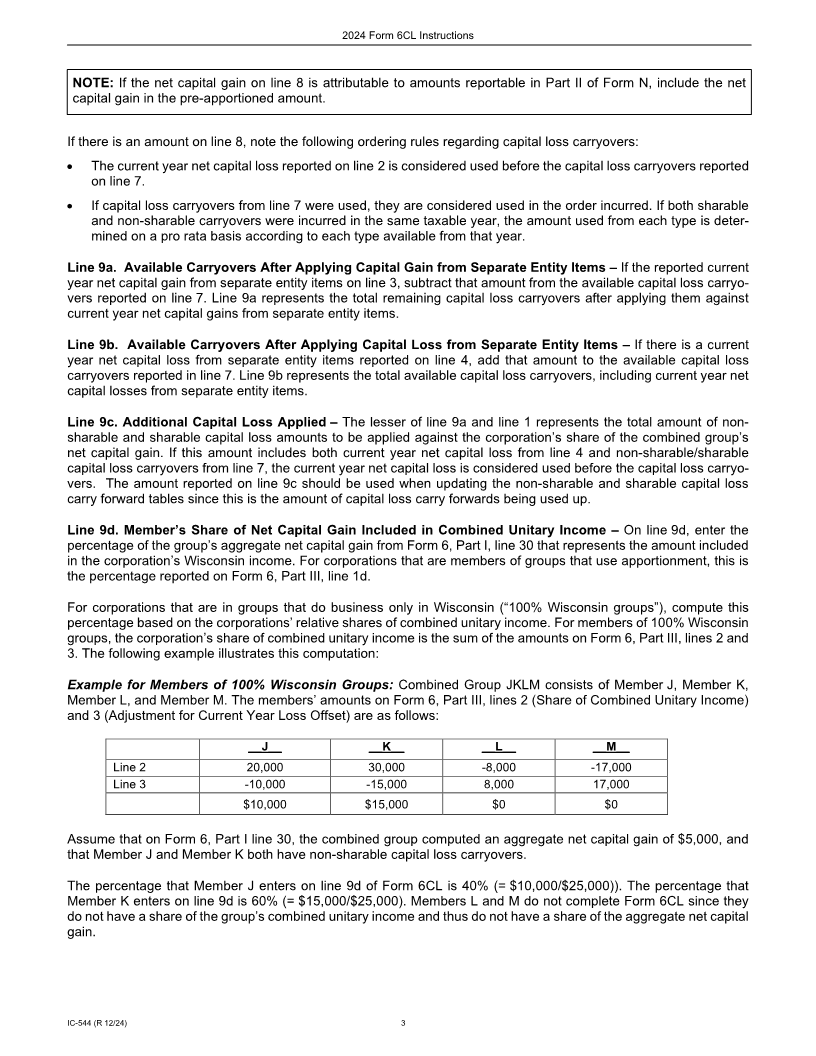

Enlarge image

Instructions for 2024 Form 6CL:

Net Capital Loss Adjustments for Combined Group Members

Who Files Form 6CL

Form 6CL is only for corporations that are combined group members. File Form 6CL only if either A. or B. below is

true:

A. The corporation has unused capital loss carryovers incurred in taxable years beginning before January 1, 2009

(or other non-sharable capital losses) and the combined group reports a net capital gain on Form 6, Part I, line

30, or

B. The corporation has capital gain/loss items to report on Form N, Wisconsin Nonapportionable and Separately

Apportioned Income, for the taxable year and the combined group computes a suspended net capital loss on

Form 6, Part I, line 30 and part of that suspended net capital loss is attributable to the corporation.

NOTE: If neither A. nor B. above is true in its entirety, do not file Form 6CL for the corporation. Also, Form 6CL

does not apply to corporations that are not combined group members, even if they are filing a Form N with the

combined return.

Purpose of Form 6CL

Under section 1211 of the Internal Revenue Code, capital losses may only be used to offset capital gains. Under sec.

71.255(4)(i) and (11), Wis. Stats., and sec. Tax 2.61(6)(c), Wisconsin Administrative Code, the capital loss limitation

is determined on an aggregate basis for the combined group, similarly to how it is determined for a consolidated

group for federal purposes under Treas. Regs. §1.1502-22 and 1.1502-23.

However, not all capital losses may be included in the aggregate computation for the combined group. The aggregate

computation cannot include non-sharable capital loss carryovers or capital gain/loss items that members must report

on a separate entity basis on Form N.

The purpose of Form 6CL is to allow a combined group member to:

• Use the non-sharable capital loss carryovers it could not include in the group’s aggregate computation, and

• Apply all of its available capital losses, including its current year net capital loss from the group’s aggregate

computation, to capital gains that are reportable on a separate entity basis on Form N.

A non-sharable capital loss is one which originated:

• In a taxable year beginning before January 1, 2009, or

In the combined unitary income of another combined group, or

• In transactions reportable on a separate entity basis on Form N.

As an alternative to completing 2024 Form 6CL, a combined group member with non-sharable capital loss carryo-

vers may choose to carry them back to a taxable year beginning before 2009, to the extent allowed under section

1212 of the Internal Revenue Code. Also, see sec. Tax 2.61(6)(c), Wisconsin Administrative Code, for further de-

tails regarding elections a corporation may make regarding its capital loss carryovers.

Line-by-Line Instructions

These instructions are presented in the order the lines appear on Form 6CL:

IC-544 (R.12/24) 1