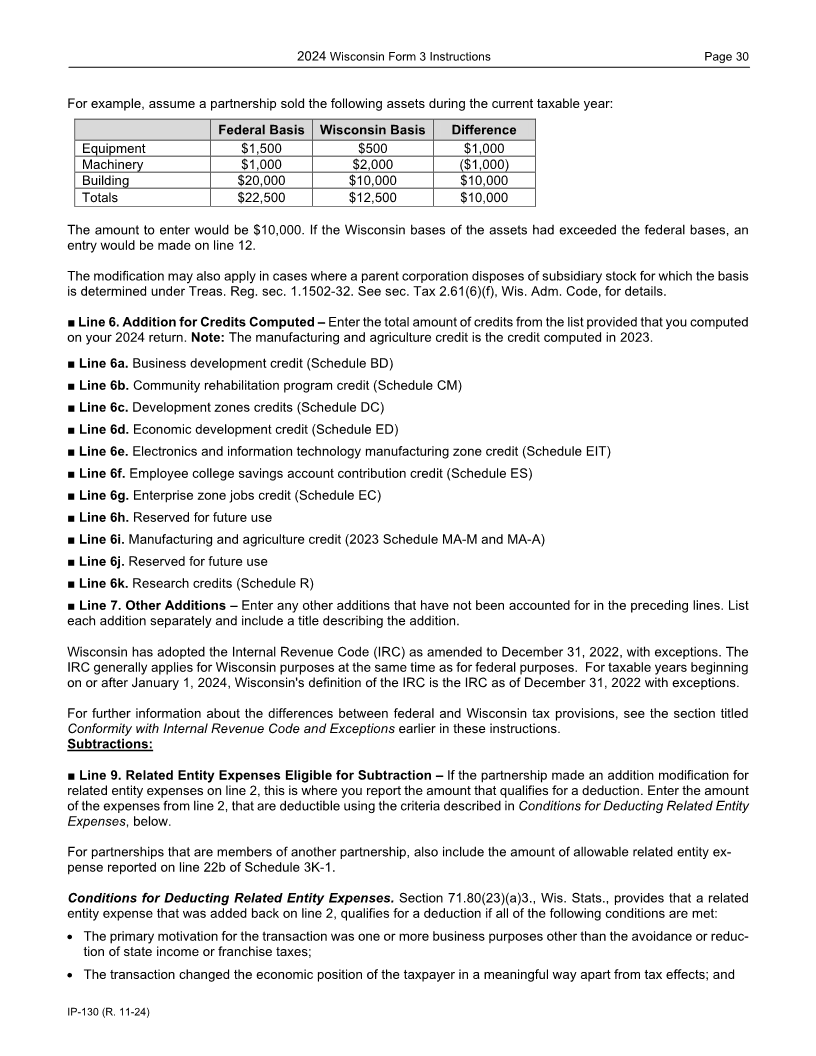

Enlarge image

2024 Wisconsin Form 3 Instructions Page 1 Table of Contents General Instructions for Form 3 ................................................................................................................................ 2 Who Must File Form 3 .............................................................................................................................................. 2 Definitions ................................................................................................................................................................. 3 When and Where to File ........................................................................................................................................... 4 Period Covered by Return ........................................................................................................................................ 5 Accounting Methods and Elections .......................................................................................................................... 5 Payment of Estimated Tax ....................................................................................................................................... 5 Disclosure of Related Entity Expenses and Reportable Transactions ..................................................................... 6 Internal Revenue Service Adjustments, Amended Returns, Claims for Refund, and Final Returns ....................... 7 Partnerships Having Nonresident Partners .............................................................................................................. 8 Schedules 3K-1 and Information Returns ................................................................................................................ 9 Wisconsin Use Tax ................................................................................................................................................... 9 Penalties for Not Filing or Filing Incorrect Returns ................................................................................................... 9 Conformity with Internal Revenue Code and Exceptions ..................................................................................... 10 Provisions of the Internal Revenue Code Adopted by Wisconsin: ......................................................................... 10 Provisions of the Internal Revenue Code Not Adopted by Wisconsin: .................................................................. 11 Depreciation and Bonus Depreciation .................................................................................................................... 15 Section 179 Expense .............................................................................................................................................. 15 How to Report Differences ..................................................................................................................................... 15 Specific Instructions for Form 3 .............................................................................................................................. 16 Items A Through M ................................................................................................................................................. 16 Part I – Calculation of Tax Due or Refund .............................................................................................................. 18 Part II - Schedule 3K – Partners’ Distributive Share Items ................................................................................... 21 Schedule 3K, Columns (b) Through (d) .................................................................................................................. 21 Adjustments Reportable on Schedule 3K, Column (c) ........................................................................................... 21 Modifications Prescribed in Wisconsin Law ........................................................................................................... 22 Guaranteed Payments Reported on Line 4 ............................................................................................................ 23 Credits Reportable on Schedule 3K, Line 15 ......................................................................................................... 23 “Other Items and Amounts” Reportable on Schedule 3K, Item 20c ....................................................................... 25 Schedule 3K, Lines 21 Through 24 ........................................................................................................................ 26 Third Party Designee .............................................................................................................................................. 26 Submitting Your Form 3 .......................................................................................................................................... 27 IP-130 (R. 11-24)