Enlarge image

2024 Form 4T Instructions

Tax-exempt organizations and certain individual retirement arrangements (IRAs) or Medical Savings Accounts

(MSAs) use Form 4T to report their unrelated business taxable income and credits and to compute their franchise or

income tax and economic development surcharge liability.

Table of Contents

General Franchise or Income Tax Return Instructions ................................................................. 2

Who Must File ........................................................................................................................ 2

When and Where to File ........................................................................................................ 3

Period Covered by Return ..................................................................................................... 3

Accounting Methods and Elections ...................................................................................... 4

Payment of Estimated Tax ..................................................................................................... 4

Disclosure of Related Entity Expenses and Reportable Transactions ............................... 5

Internal Revenue Service Adjustments, Amended Returns, and Claims for Refund ......... 6

Economic Development Surcharge ...................................................................................... 6

Information Returns ............................................................................................................... 7

Wisconsin Use Tax ................................................................................................................ 7

Penalties for Not Filing or Filing Incorrect Returns ............................................................ 7

Conformity With Internal Revenue Code and Exceptions .................................................................... 7

Provisions of the Internal Revenue Code Not Adopted by Wisconsin: .............................. 8

Other Exceptions to Internal Revenue Code ...................................................................... 12

Depreciation and Bonus Depreciation ............................................................................... 12

Accounting for Differences ................................................................................................. 12

Items A Through J ................................................................................................................ 13

Lines 1 Through 13 - Organizations Taxable as Corporations......................................... 14

Lines 14 Through 23 - Organizations Taxable as Trusts ................................................... 18

Lines 25 Through 41 ............................................................................................................ 21

Additional Information, Signatures, and Supplemental Schedules .................................. 23

Wisconsin Income of Multistate Organizations ................................................................. 24

Who Must Use Apportionment ............................................................................................ 24

What Is the Apportionment Percentage ............................................................................. 25

Corporate Partners or LLC Members ................................................................................. 25

Obtaining Forms and Assistance ....................................................................................... 26

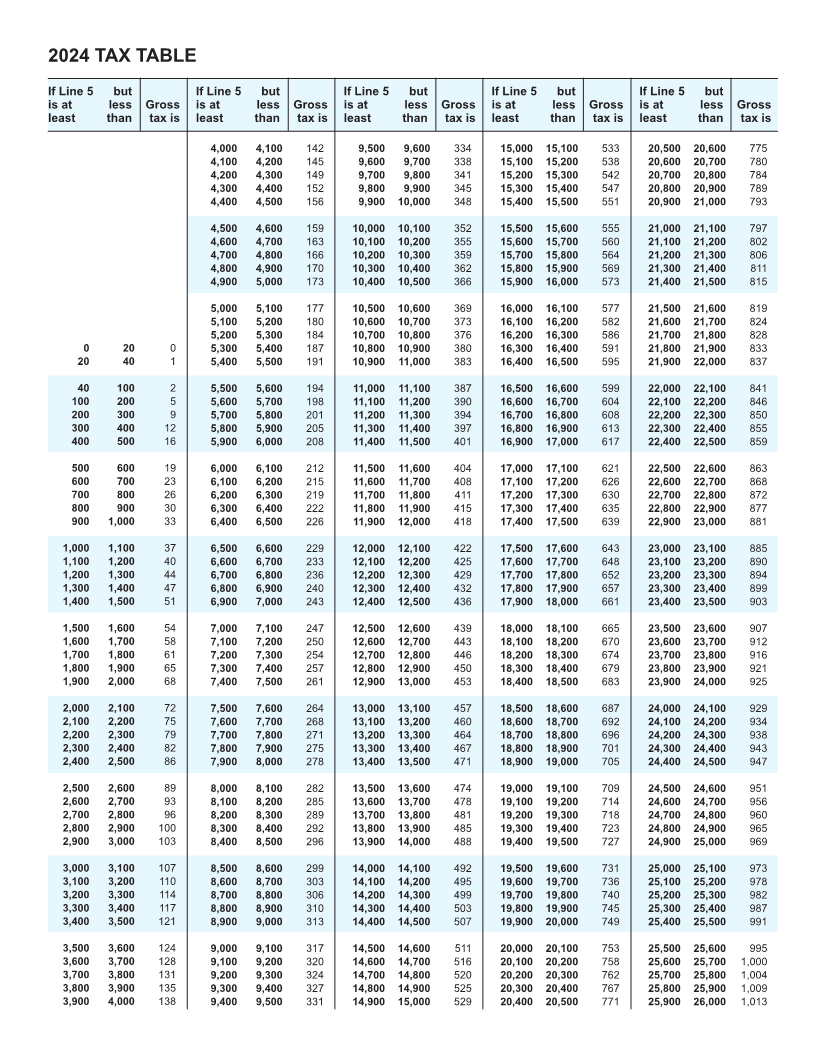

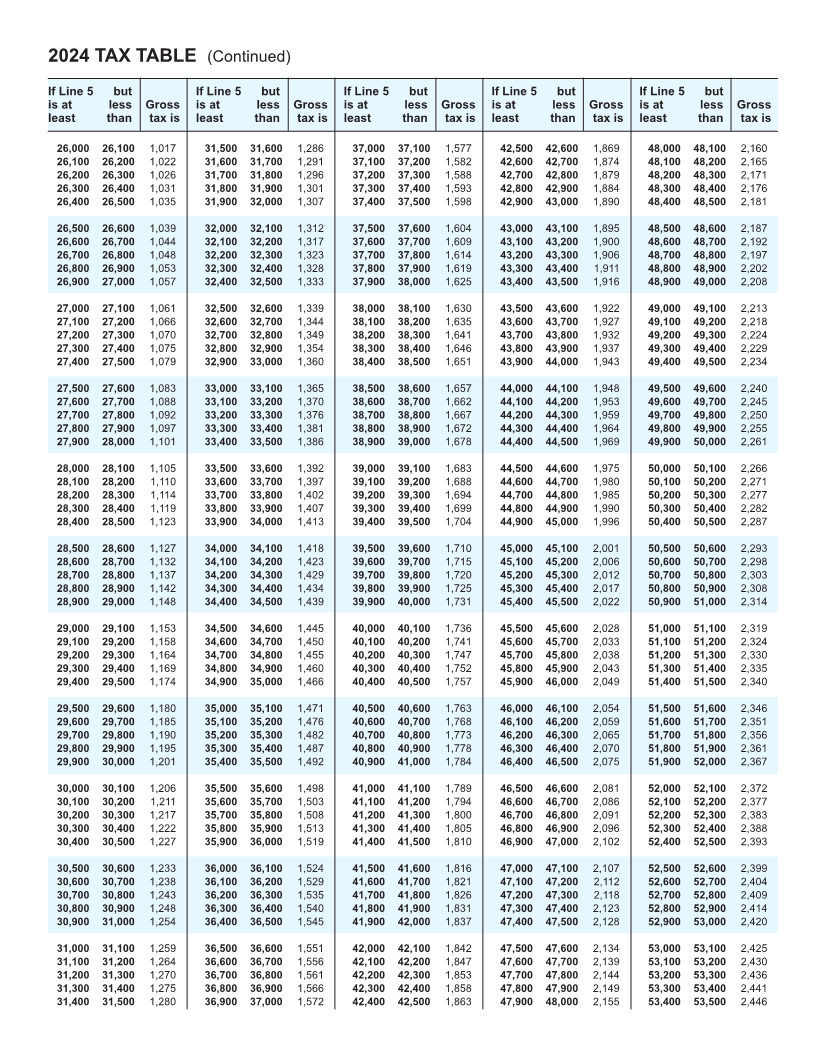

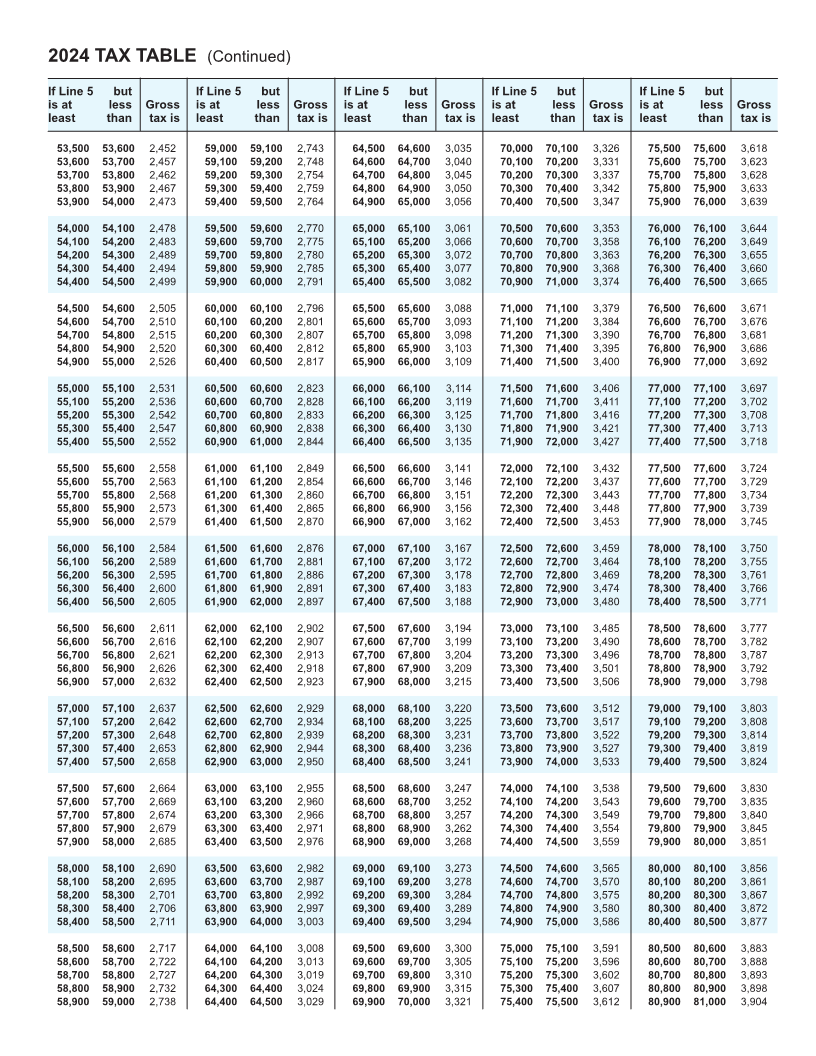

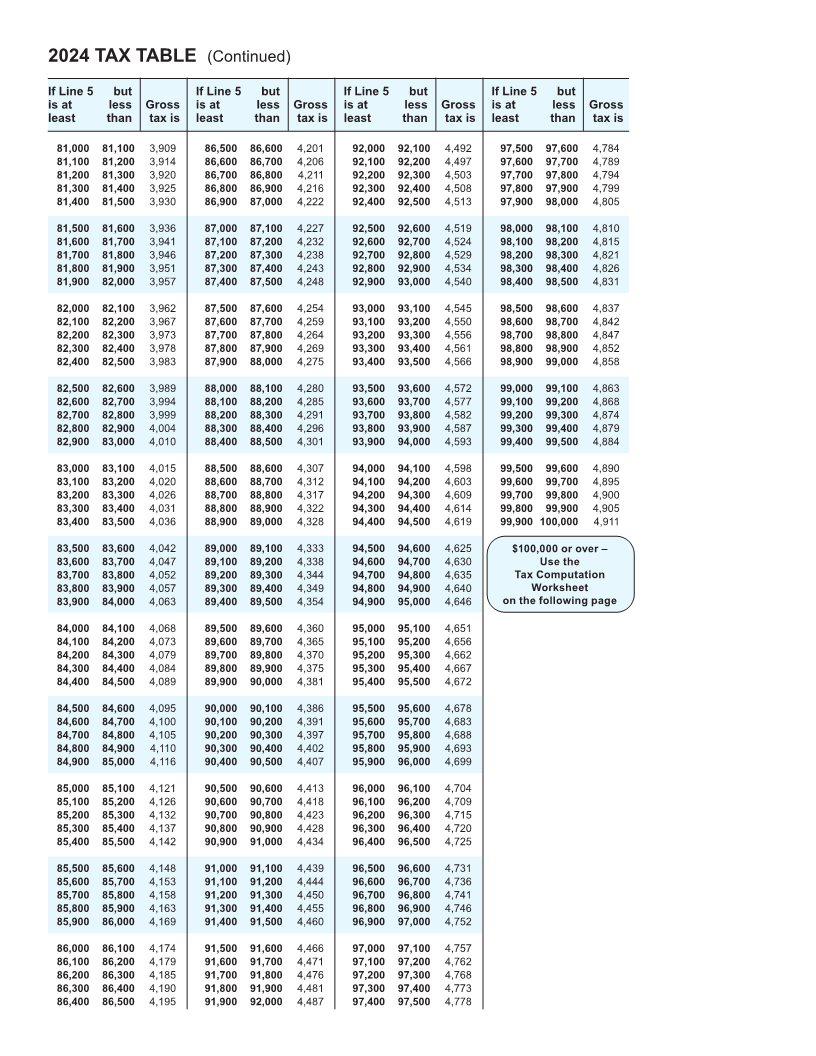

Appendix: Tax Table for Trusts