Enlarge image

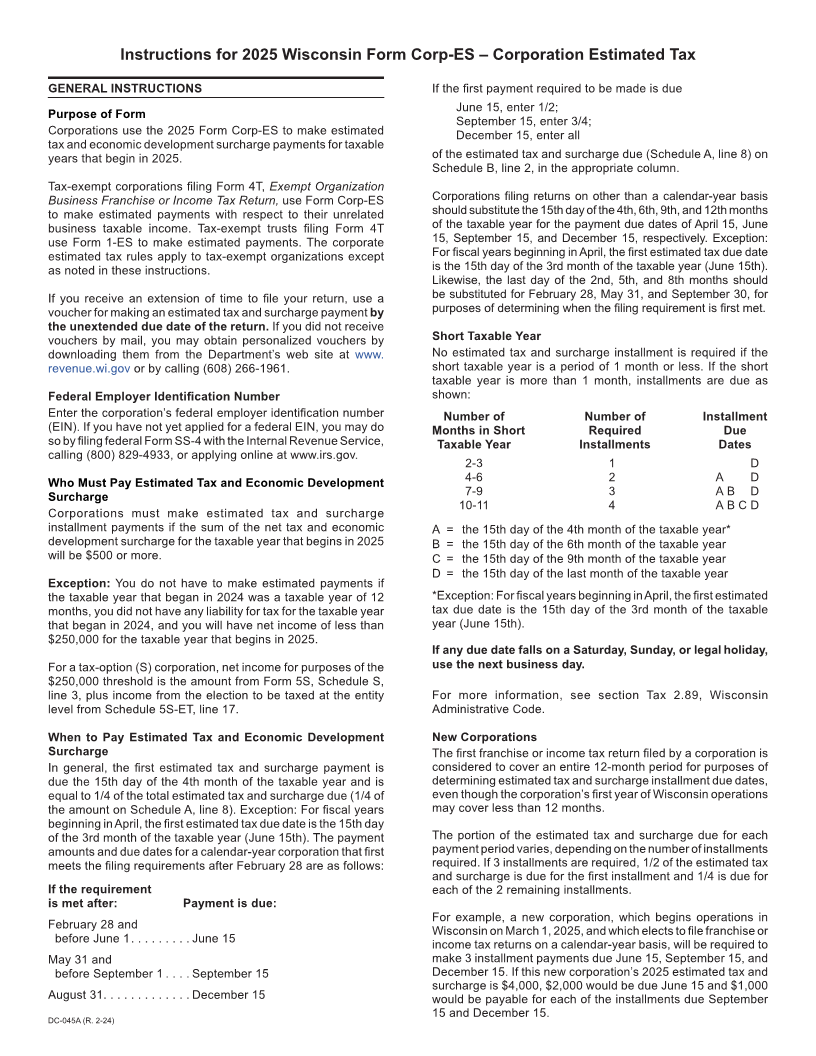

Instructions for 2025 Wisconsin Form Corp-ES – Corporation Estimated Tax

GENERAL INSTRUCTIONS If the first payment required to be made is due

June 15, enter 1/2;

Purpose of Form September 15, enter 3/4;

Corporations use the 2025 Form Corp-ES to make estimated December 15, enter all

tax and economic development surcharge payments for taxable

years that begin in 2025. of the estimated tax and surcharge due (Schedule A, line 8) on

Schedule B, line 2, in the appropriate column.

Tax-exempt corporations filing Form 4T, Exempt Organization

Business Franchise or Income Tax Return, use Form Corp-ES Corporations filing returns on other than a calendar-year basis

to make estimated payments with respect to their unrelated should substitute the 15th day of the 4th, 6th, 9th, and 12th months

business taxable income. Tax-exempt trusts filing Form 4T of the taxable year for the payment due dates of April 15, June

use Form 1-ES to make estimated payments. The corporate 15, September 15, and December 15, respectively. Exception:

estimated tax rules apply to tax-exempt organizations except For fiscal years beginning in April, the first estimated tax due date

as noted in these instructions. is the 15th day of the 3rd month of the taxable year (June 15th).

Likewise, the last day of the 2nd, 5th, and 8th months should

If you receive an extension of time to file your return, use a be substituted for February 28, May 31, and September 30, for

voucher for making an estimated tax and surcharge payment by purposes of determining when the filing requirement is first met.

the unextended due date of the return. If you did not receive

vouchers by mail, you may obtain personalized vouchers by Short Taxable Year

downloading them from the Department’s web site at www. No estimated tax and surcharge installment is required if the

revenue.wi.gov or by calling (608) 266-1961. short taxable year is a period of 1 month or less. If the short

taxable year is more than 1 month, installments are due as

Federal Employer Identification Number shown:

Enter the corporation’s federal employer identification number Number of Number of Installment

(EIN). If you have not yet applied for a federal EIN, you may do Months in Short Required Due

so by filing federal Form SS-4 with the Internal Revenue Service, Taxable Year Installments Dates

calling (800) 829-4933, or applying online at www.irs.gov.

2-3 1 D

Who Must Pay Estimated Tax and Economic Development 4-6 2 A D

Surcharge 7-9 3 A B D

10-11 4 A B C D

Corporations must make estimated tax and surcharge

installment payments if the sum of the net tax and economic A = the 15th day of the 4th month of the taxable year*

development surcharge for the taxable year that begins in 2025 B = the 15th day of the 6th month of the taxable year

will be $500 or more. C = the 15th day of the 9th month of the taxable year

D = the 15th day of the last month of the taxable year

Exception: You do not have to make estimated payments if

the taxable year that began in 2024 was a taxable year of 12 *Exception: For fiscal years beginning in April, the first estimated

months, you did not have any liability for tax for the taxable year tax due date is the 15th day of the 3rd month of the taxable

that began in 2024, and you will have net income of less than year (June 15th).

$250,000 for the taxable year that begins in 2025.

If any due date falls on a Saturday, Sunday, or legal holiday,

For a tax-option (S) corporation, net income for purposes of the use the next business day.

$250,000 threshold is the amount from Form 5S, Schedule S,

line 3, plus income from the election to be taxed at the entity For more information, see section Tax 2.89, Wisconsin

level from Schedule 5S-ET, line 17. Administrative Code.

When to Pay Estimated Tax and Economic Development New Corporations

Surcharge The first franchise or income tax return filed by a corporation is

In general, the first estimated tax and surcharge payment is considered to cover an entire 12-month period for purposes of

due the 15th day of the 4th month of the taxable year and is determining estimated tax and surcharge installment due dates,

equal to 1/4 of the total estimated tax and surcharge due (1/4 of even though the corporation’s first year of Wisconsin operations

the amount on Schedule A, line 8). Exception: For fiscal years may cover less than 12 months.

beginning in April, the first estimated tax due date is the 15th day

of the 3rd month of the taxable year (June 15th). The payment The portion of the estimated tax and surcharge due for each

amounts and due dates for a calendar-year corporation that first payment period varies, depending on the number of installments

meets the filing requirements after February 28 are as follows: required. If 3 installments are required, 1/2 of the estimated tax

and surcharge is due for the first installment and 1/4 is due for

If the requirement each of the 2 remaining installments.

is met after: Payment is due:

For example, a new corporation, which begins operations in

February 28 and Wisconsin on March 1, 2025, and which elects to file franchise or

before June 1 ......... June 15 income tax returns on a calendar-year basis, will be required to

May 31 and make 3 installment payments due June 15, September 15, and

before September 1 .... September 15 December 15. If this new corporation’s 2025 estimated tax and

surcharge is $4,000, $2,000 would be due June 15 and $1,000

August 31 ............. December 15 would be payable for each of the installments due September

DC-045A (R. 2-24) 15 and December 15.