Enlarge image

2024 Schedule SB Instructions

Subtractions from Income

Purpose of Schedule SB

Schedule SB is used to report differences between federal and Wisconsin income. These differences are called modifications

and may affect the amount you report as a subtraction modification on line 6 of Form 1.

Who Must File Schedule SB

Your federal income may include items that aren’t taxable for Wisconsin, or it may not include items that are deductible for Wis-

consin. You may have to subtract these items from your federal income to arrive at the correct Wisconsin income. Schedule SB

must be filed by persons for whom the subtraction modifications described below apply.

Other Schedules and Publications

These instructions will refer to other Wisconsin schedules that may be needed to compute and the claim an addition or subtrac-

tion along with publications that may contain additional information. The schedules and any related instructions can be found

on the department’s website at https://www.revenue.wi.gov/Pages/Form/2024Individual.aspx. The Wisconsin publications ref-

erenced are located at https://www.revenue.wi.gov/Pages/HTML/taxpubs.aspx.

Line Instructions

Line 1 – Taxable Refund of State Income Tax

Refunds of state and local income taxes are not taxable for Wisconsin. Fill in the amount of taxable refunds, credits, or offsets

of state and local income taxes from line 1 of federal Schedule 1 (Form 1040).

Line 2 – United States Government Interest

Fill in the amount of interest on U.S. bonds and interest and dividends of certain U.S. government corporations that is included

on line 3 of Form 1. This income is not taxable.

A mutual fund may invest in U.S. government securities. If it does, a portion or all of its ordinary dividend may not be taxable

by Wisconsin. If a mutual fund advised you that all or a portion of its ordinary dividend is from investments in U.S. government

securities, include that portion on line 2.

Caution: Do not fill in on line 2, interest from Ginnie Mae (Government National Mortgage Association) securities and other

similar securities which are “guaranteed” by the United States government. You must include interest from these securities in

your Wisconsin taxable income.

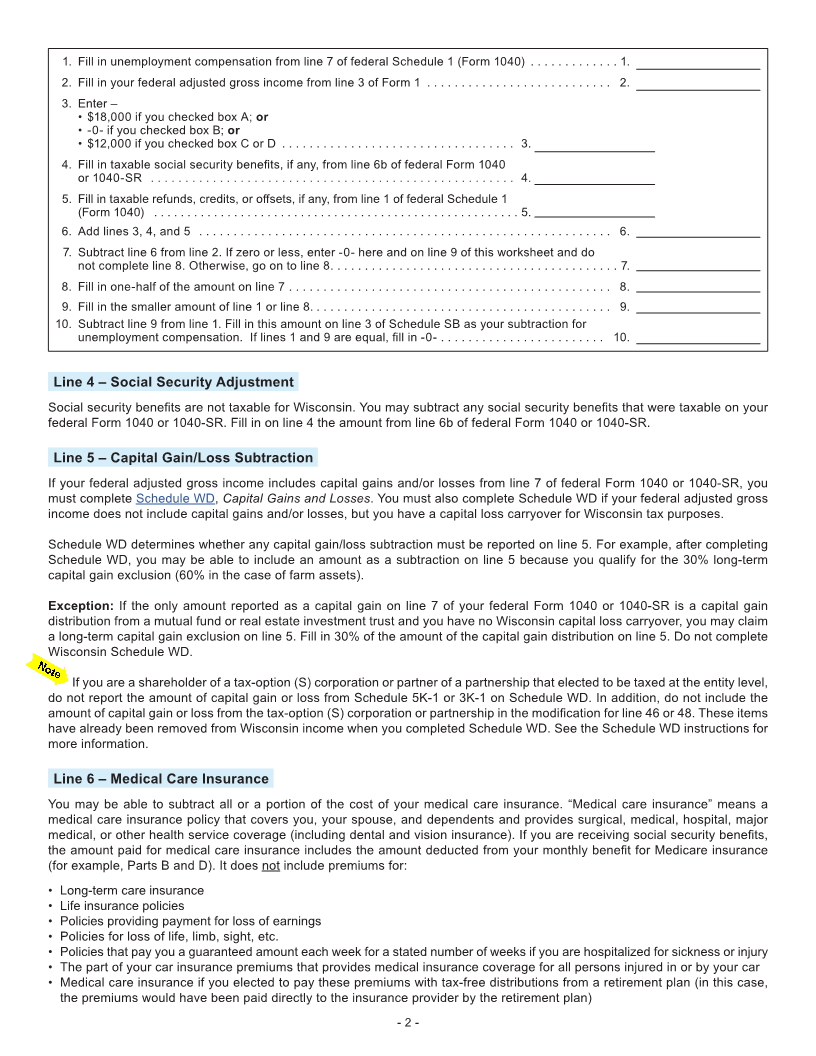

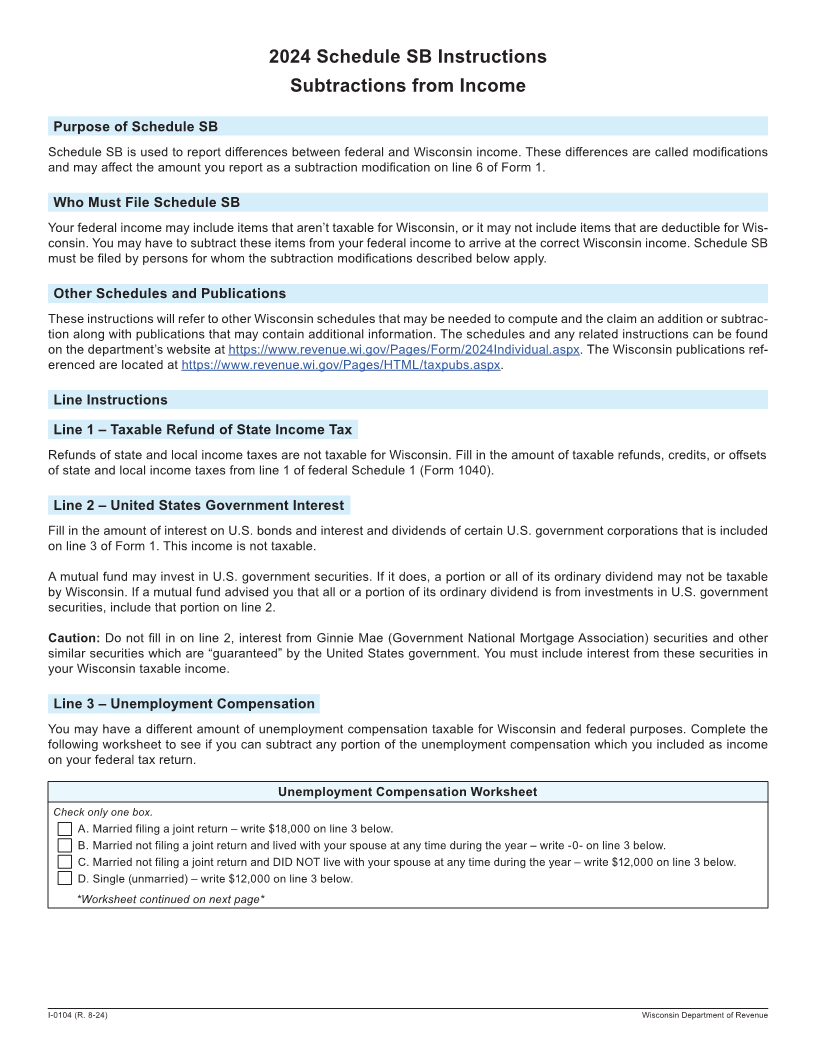

Line 3 – Unemployment Compensation

You may have a different amount of unemployment compensation taxable for Wisconsin and federal purposes. Complete the

following worksheet to see if you can subtract any portion of the unemployment compensation which you included as income

on your federal tax return.

Unemployment Compensation Worksheet

Check only one box.

A. Married filing a joint return – write $18,000 on line 3 below.

B. Married not filing a joint return and lived with your spouse at any time during the year – write -0- on line 3 below.

C. Married not filing a joint return and DID NOT live with your spouse at any time during the year – write $12,000 on line 3 below.

D. Single (unmarried) – write $12,000 on line 3 below.

*Worksheet continued on next page*

I-0104 (R. 8-24) Wisconsin Department of Revenue