Enlarge image

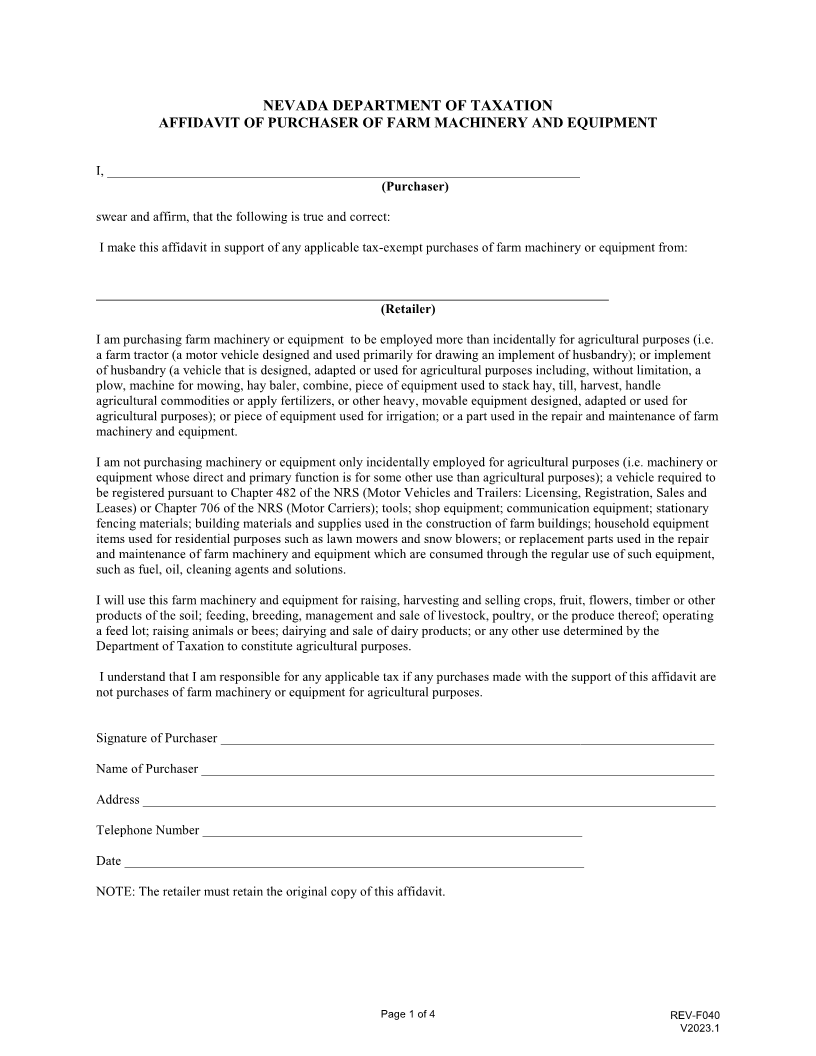

NEVADA DEPARTMENT OF TAXATION

AFFIDAVIT OF PURCHASER OF FARM MACHINERY AND EQUIPMENT

I, _______________________________________________________________________

(Purchaser)

swear and affirm, that the following is true and correct:

I make this affidavit in support of any applicable tax-exempt purchases of farm machinery or equipment from:

_____________________________________________________________________________

(Retailer)

I am purchasing farm machinery or equipment to be employed more than incidentally for agricultural purposes (i.e.

a farm tractor (a motor vehicle designed and used primarily for drawing an implement of husbandry); or implement

of husbandry (a vehicle that is designed, adapted or used for agricultural purposes including, without limitation, a

plow, machine for mowing, hay baler, combine, piece of equipment used to stack hay, till, harvest, handle

agricultural commodities or apply fertilizers, or other heavy, movable equipment designed, adapted or used for

agricultural purposes); or piece of equipment used for irrigation; or a part used in the repair and maintenance of farm

machinery and equipment.

I am not purchasing machinery or equipment only incidentally employed for agricultural purposes (i.e. machinery or

equipment whose direct and primary function is for some other use than agricultural purposes); a vehicle required to

be registered pursuant to Chapter 482 of the NRS (Motor Vehicles and Trailers: Licensing, Registration, Sales and

Leases) or Chapter 706 of the NRS (Motor Carriers); tools; shop equipment; communication equipment; stationary

fencing materials; building materials and supplies used in the construction of farm buildings; household equipment

items used for residential purposes such as lawn mowers and snow blowers; or replacement parts used in the repair

and maintenance of farm machinery and equipment which are consumed through the regular use of such equipment,

such as fuel, oil, cleaning agents and solutions.

I will use this farm machinery and equipment for raising, harvesting and selling crops, fruit, flowers, timber or other

products of the soil; feeding, breeding, management and sale of livestock, poultry, or the produce thereof; operating

a feed lot; raising animals or bees; dairying and sale of dairy products; or any other use determined by the

Department of Taxation to constitute agricultural purposes.

I understand that I am responsible for any applicable tax if any purchases made with the support of this affidavit are

not purchases of farm machinery or equipment for agricultural purposes.

Signature of Purchaser __________________________________________________________________________

Name of Purchaser _____________________________________________________________________________

Address ______________________________________________________________________________________

Telephone Number _________________________________________________________

Date _____________________________________________________________________

NOTE: The retailer must retain the original copy of this affidavit.

Page 1 of 4 REV-F040

V2023.1