Enlarge image

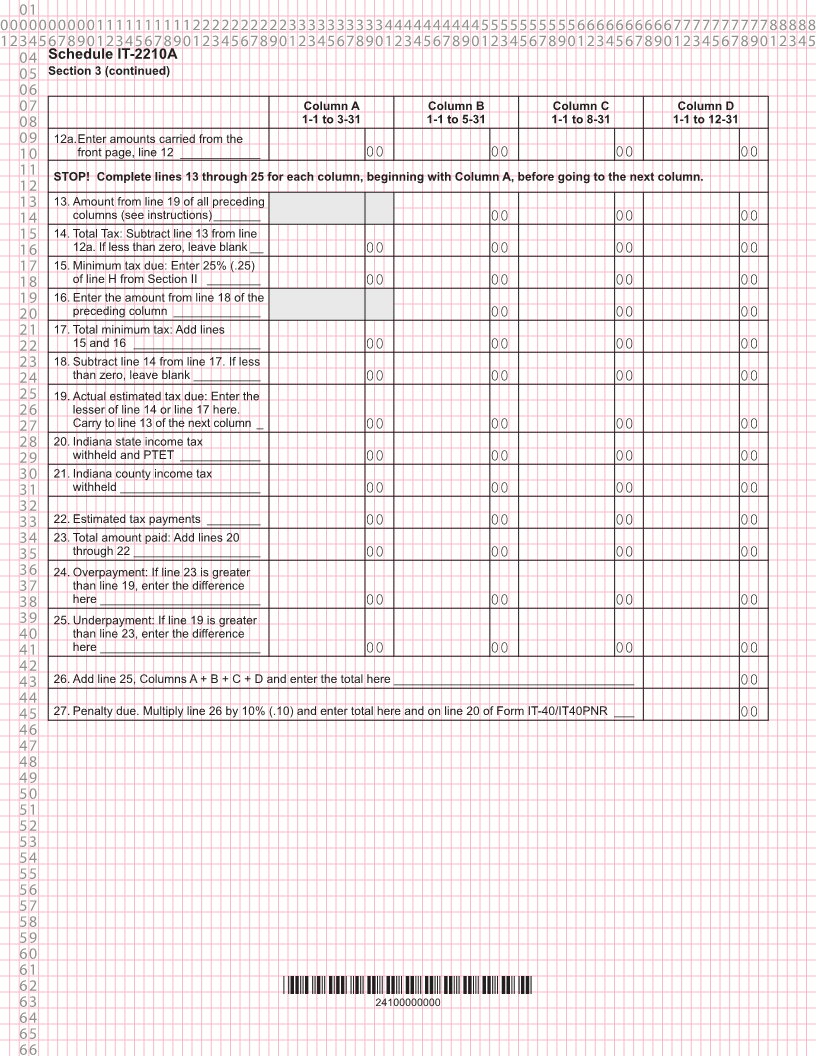

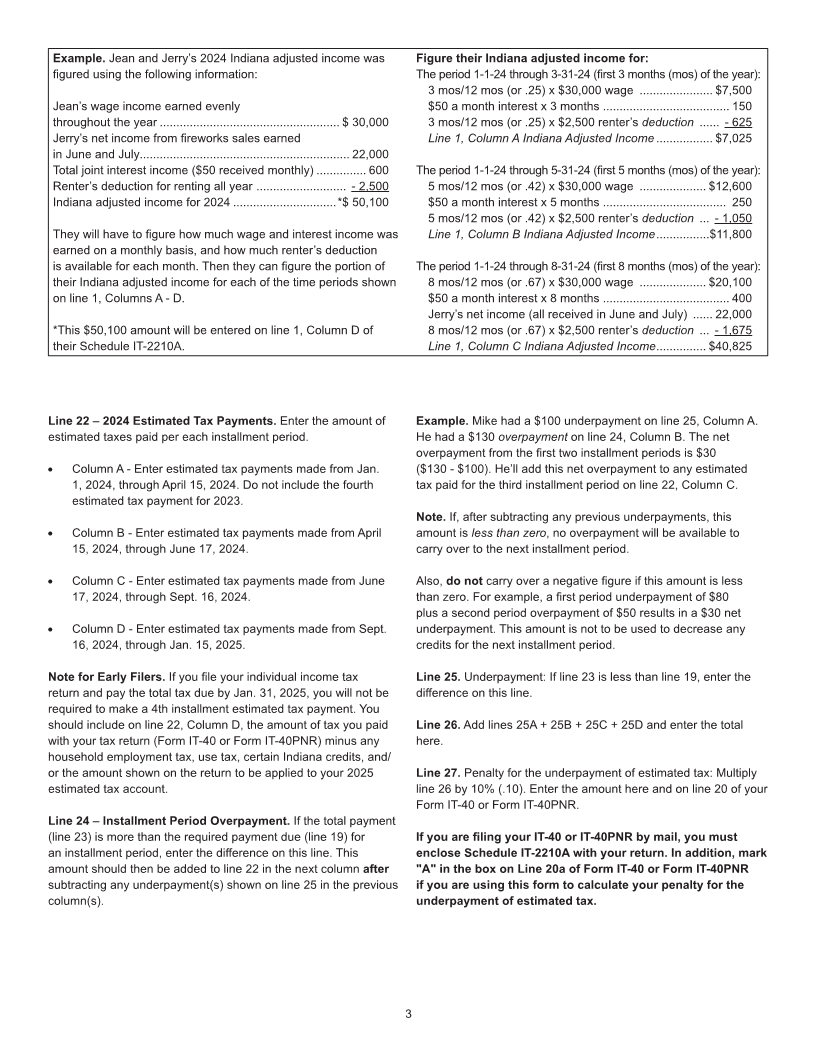

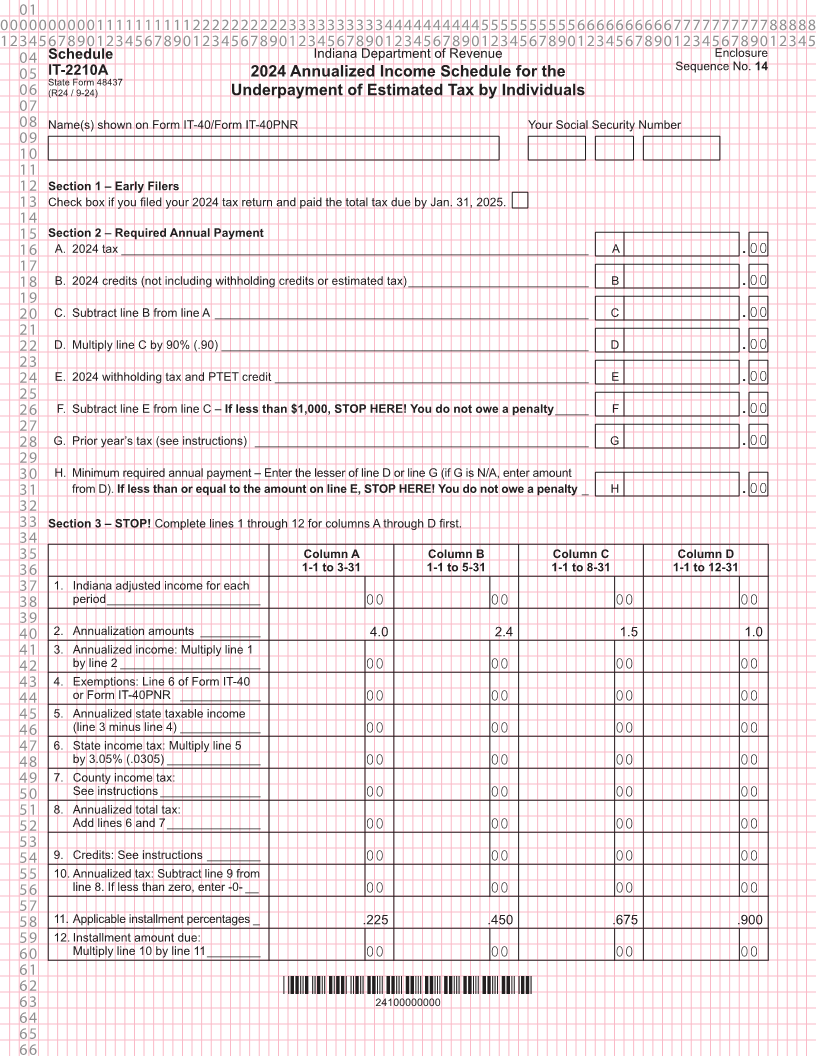

01 0000000000111111111122222222223333333333444444444455555555556666666666777777777788888 1234567890123456789012345678901234567890123456789012345678901234567890123456789012345 04 Schedule Indiana Department of Revenue Enclosure 05 IT-2210A 2024 Annualized Income Schedule for the Sequence No. 14 State Form 48437 06 (R24 / 9-24) Underpayment of Estimated Tax by Individuals 07 08 Name(s) shown on Form IT-40/Form IT-40PNR Your Social Security Number 09 10 11 12 Section 1 – Early Filers 13 Check box if you filed your 2024 tax return and paid the total tax due by Jan. 31, 2025. 14 15 Section 2 – Required Annual Payment 16 A. 2024 tax ______________________________________________________________________ A .00 17 18 B. 2024 credits (not including withholding credits or estimated tax) ___________________________ B .00 19 20 C. Subtract line B from line A ________________________________________________________ C .00 21 22 D. Multiply line C by 90% (.90) _______________________________________________________ D .00 23 24 E. 2024 withholding tax and PTET credit _______________________________________________ E .00 25 26 F. Subtract line E from line C – If less than $1,000, STOP HERE! You do not owe a penalty _____ F .00 27 28 G. Prior year’s tax (see instructions) __________________________________________________ G .00 29 30 H. Minimum required annual payment – Enter the lesser of line D or line G (if G is N/A, enter amount 31 from D). If less than or equal to the amount on line E, STOP HERE! You do not owe a penalty _ H .00 32 33 Section 3 – STOP! Complete lines 1 through 12 for columns A through D first. 34 35 Column A Column B Column C Column D 36 1-1 to 3-31 1-1 to 5-31 1-1 to 8-31 1-1 to 12-31 37 1. Indiana adjusted income for each 38 period _______________________ 00 00 00 00 39 40 2. Annualization amounts _________ 4.0 2.4 1.5 1.0 41 3. Annualized income: Multiply line 1 42 by line 2 _____________________ 00 00 00 00 43 4. Exemptions: Line 6 of Form IT-40 44 or Form IT-40PNR ____________ 00 00 00 00 45 5. Annualized state taxable income 46 (line 3 minus line 4) ____________ 00 00 00 00 47 6. State income tax: Multiply line 5 48 by 3.05% (.0305) ______________ 00 00 00 00 49 7. County income tax: 50 See instructions _______________ 00 00 00 00 51 8. Annualized total tax: 52 Add lines 6 and 7 ______________ 00 00 00 00 53 54 9. Credits: See instructions ________ 00 00 00 00 55 10. Annualized tax: Subtract line 9 from 56 line 8. If less than zero, enter -0- __ 00 00 00 00 57 58 11. Applicable installment percentages _ .225 .450 .675 .900 59 12. Installment amount due: 60 Multiply line 10 by line 11 ________ 00 00 00 00 61 62 *24100000000* 63 24100000000 64 65 66