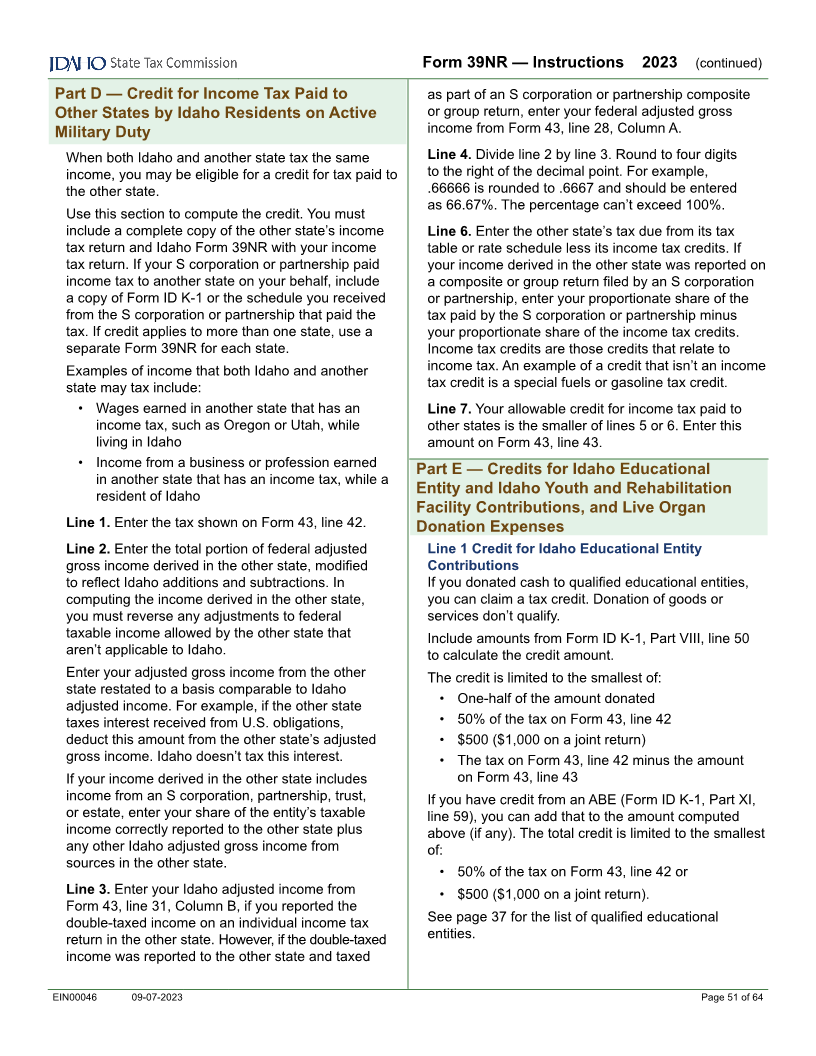

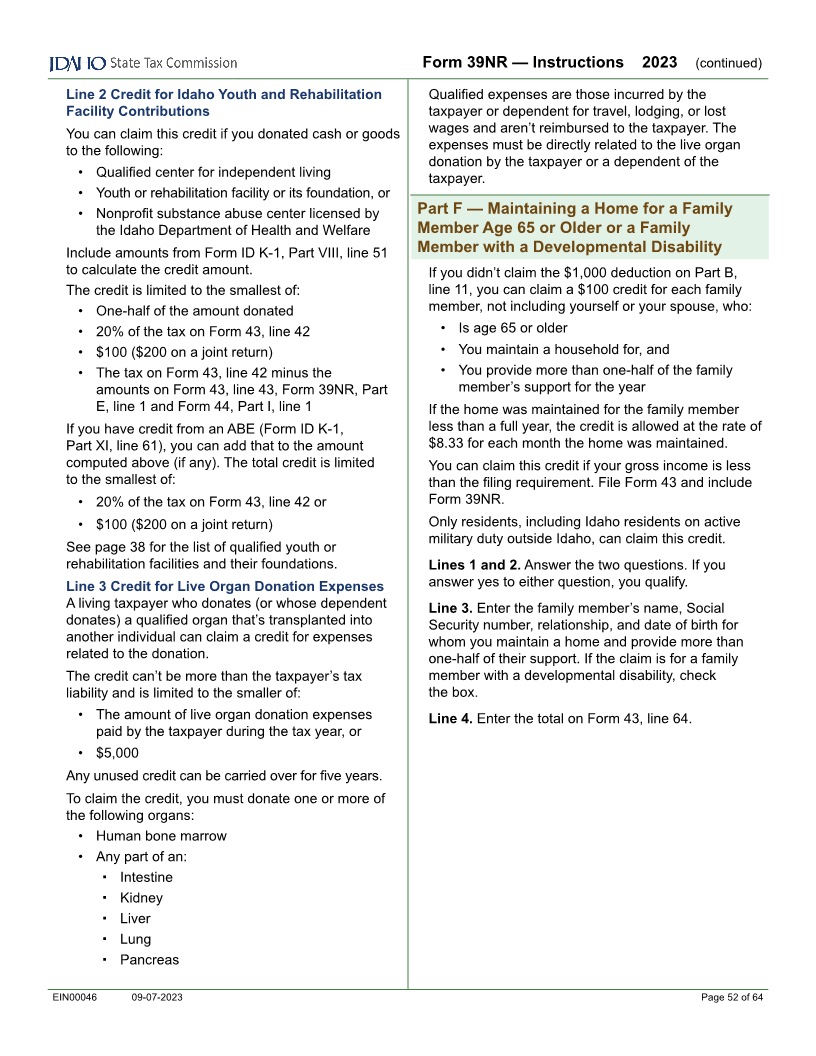

Enlarge image

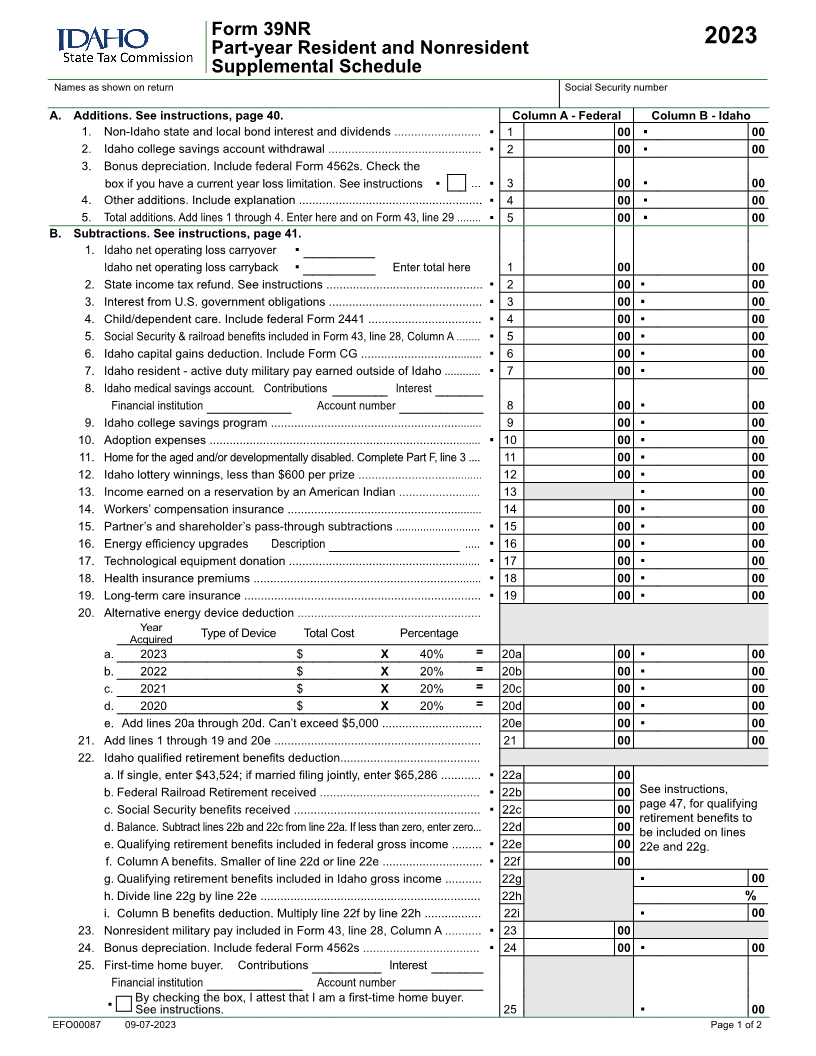

Form 39NR

2023

Part-year Resident and Nonresident

Supplemental Schedule

Names as shown on return Social Security number

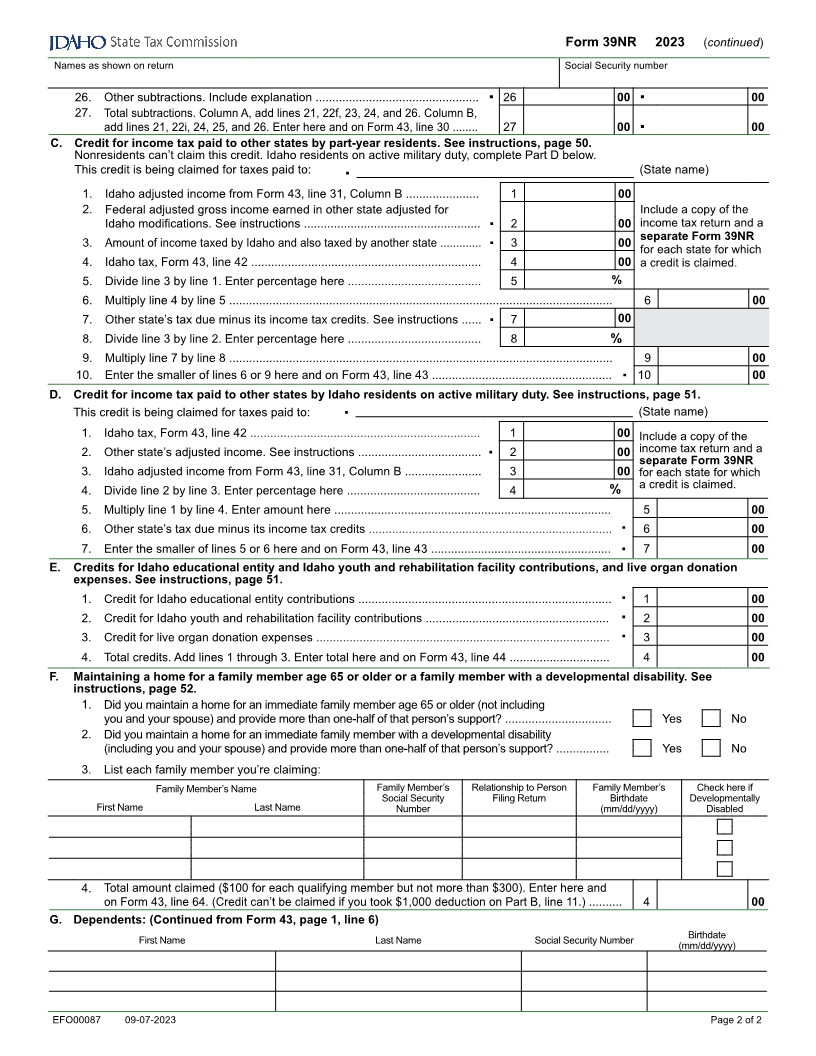

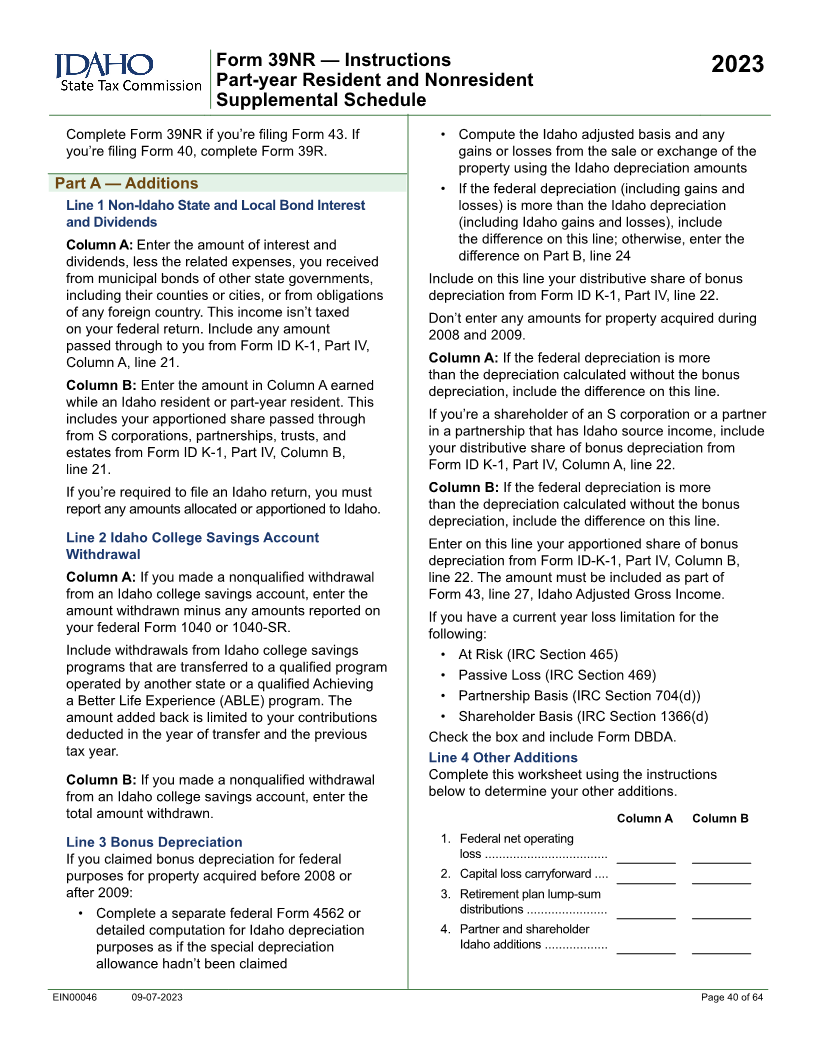

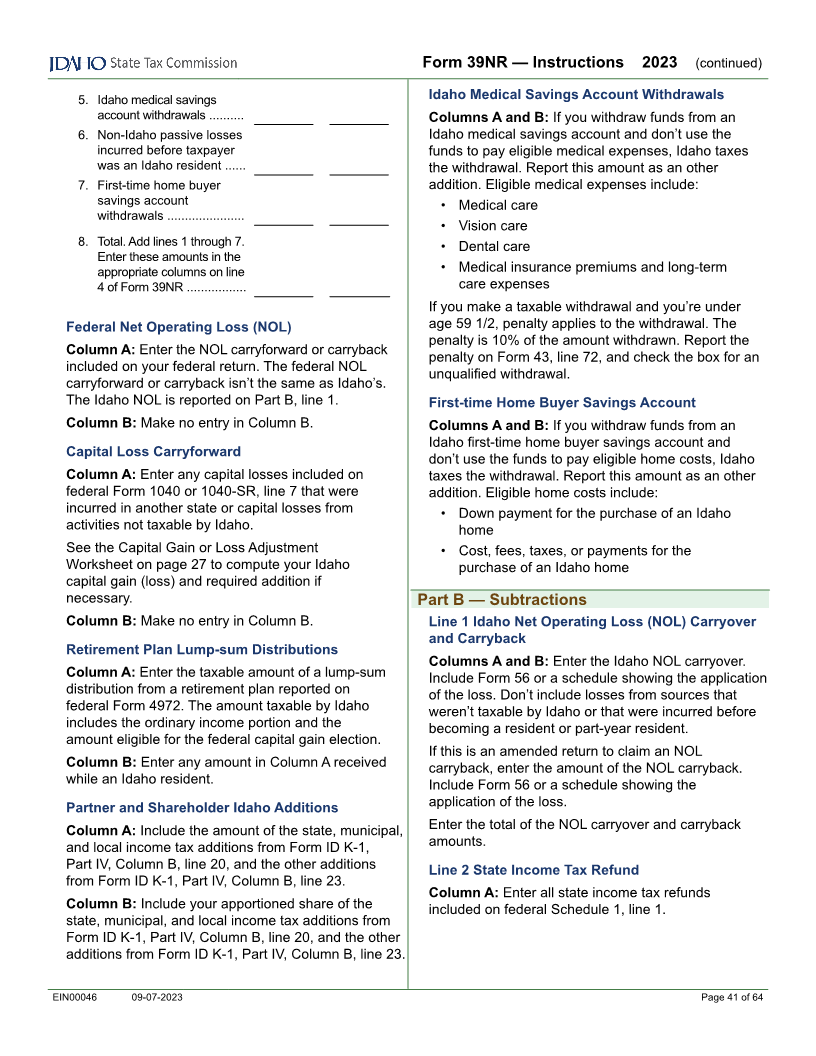

A. Additions. See instructions, page 40. Column A - Federal Column B - Idaho

1. Non-Idaho state and local bond interest and dividends .......................... ▪ 1 00 ▪ 00

2. Idaho college savings account withdrawal .............................................. ▪ 2 00 ▪ 00

3. Bonus depreciation. Include federal Form 4562s. Check the

box if you have a current year loss limitation. See instructions ▪ ... ▪ 3 00 ▪ 00

4. Other additions. Include explanation ....................................................... ▪ 4 00 ▪ 00

5. Total additions. Add lines 1 through 4. Enter here and on Form 43, line 29 ........ ▪ 5 00 ▪ 00

B. Subtractions. See instructions, page 41.

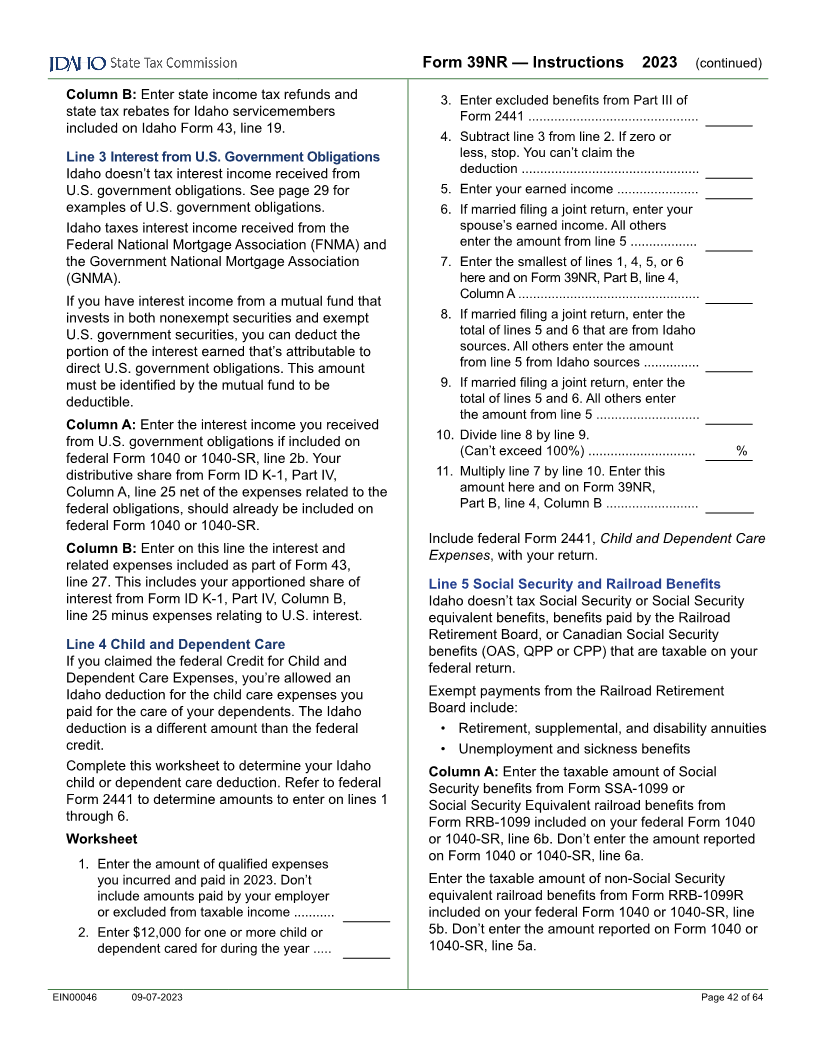

1. Idaho net operating loss carryover ▪

Idaho net operating loss carryback ▪ Enter total here 1 00 00

2. State income tax refund. See instructions ............................................... ▪ 2 00 ▪ 00

3. Interest from U.S. government obligations .............................................. ▪ 3 00 ▪ 00

4. Child/dependent care. Include federal Form 2441 .................................. ▪ 4 00 ▪ 00

5. Social Security & railroad benefits included in Form 43, line 28, Column A ........ ▪ 5 00 ▪ 00

6. Idaho capital gains deduction. Include Form CG ..................................... ▪ 6 00 ▪ 00

7. Idaho resident - active duty military pay earned outside of Idaho ............ ▪ 7 00 ▪ 00

8. Idaho medical savings account. Contributions Interest

Financial institution Account number 8 00 ▪ 00

9. Idaho college savings program ................................................................ 9 00 ▪ 00

10. Adoption expenses .................................................................................. ▪ 10 00 ▪ 00

11. Home for the aged and/or developmentally disabled. Complete Part F, line 3 .... 11 00 ▪ 00

12. Idaho lottery winnings, less than $600 per prize ...................................... 12 00 ▪ 00

13. Income earned on a reservation by an American Indian ......................... 13 ▪ 00

14. Workers’ compensation insurance ........................................................... 14 00 ▪ 00

15. Partner’s and shareholder’s pass-through subtractions ............................ ▪ 15 00 ▪ 00

16. Energy efficiency upgrades Description ..... ▪ 16 00 ▪ 00

17. Technological equipment donation .......................................................... ▪ 17 00 ▪ 00

18. Health insurance premiums ..................................................................... ▪ 18 00 ▪ 00

19. Long-term care insurance ....................................................................... ▪ 19 00 ▪ 00

20. Alternative energy device deduction .......................................................

Year Type of Device Total Cost Percentage

Acquired

a. 2023 $ X 40% = 20a 00 ▪ 00

b. 2022 $ X 20% = 20b 00 ▪ 00

c. 2021 $ X 20% = 20c 00 ▪ 00

d. 2020 $ X 20% = 20d 00 ▪ 00

e. Add lines 20a through 20d. Can’t exceed $5,000 .............................. 20e 00 ▪ 00

21. Add lines 1 through 19 and 20e .............................................................. 21 00 00

22. Idaho qualified retirement benefits deduction..........................................

a. If single, enter $43,524; if married filing jointly, enter $65,286 ............ ▪ 22a 00

b. Federal Railroad Retirement received ................................................ ▪ 22b 00 See instructions,

c. Social Security benefits received ........................................................ ▪ 22c 00 page 47, for qualifying

retirement benefits to

d. Balance. Subtract lines 22b and 22c from line 22a. If less than zero, enter zero... 22d 00 be included on lines

e. Qualifying retirement benefits included in federal gross income ......... ▪ 22e 00 22e and 22g.

f. Column A benefits. Smaller of line 22d or line 22e .............................. ▪ 22f 00

g. Qualifying retirement benefits included in Idaho gross income ........... 22g ▪ 00

h. Divide line 22g by line 22e .................................................................. 22h %

i. Column B benefits deduction. Multiply line 22f by line 22h ................. 22i ▪ 00

23. Nonresident military pay included in Form 43, line 28, Column A ........... ▪ 23 00

24. Bonus depreciation. Include federal Form 4562s ................................... ▪ 24 00 ▪ 00

25. First-time home buyer. Contributions Interest

Financial institution Account number

By checking the box, I attest that I am a first-time home buyer.

▪ See instructions. 25 ▪ 00

EFO00087 09-07-2023 Page 1 of 2