Enlarge image

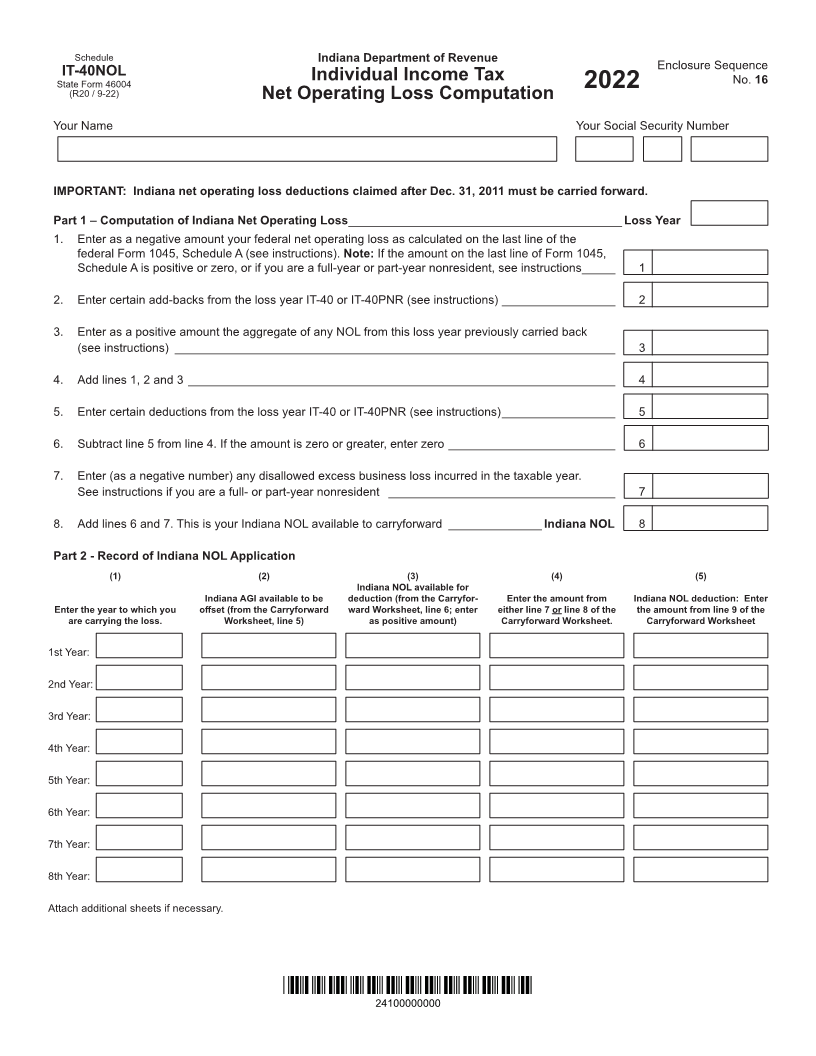

Schedule Indiana Department of Revenue

Enclosure Sequence

IT-40NOL

State Form 46004 Individual Income Tax No. 16

(R20 / 9-22) Net Operating Loss Computation 2022

Your Name Your Social Security Number

IMPORTANT: Indiana net operating loss deductions claimed after Dec. 31, 2011 must be carried forward.

Part 1 – Computation of Indiana Net Operating Loss _________________________________________ Loss Year

1. Enter as a negative amount your federal net operating loss as calculated on the last line of the

federal Form 1045, Schedule A (see instructions). Note: If the amount on the last line of Form 1045,

Schedule A is positive or zero, or if you are a full-year or part-year nonresident, see instructions _____ 1

2. Enter certain add-backs from the loss year IT-40 or IT-40PNR (see instructions) _________________ 2

3. Enter as a positive amount the aggregate of any NOL from this loss year previously carried back

(see instructions) __________________________________________________________________ 3

4. Add lines 1, 2 and 3 ________________________________________________________________ 4

5. Enter certain deductions from the loss year IT-40 or IT-40PNR (see instructions) _________________ 5

6. Subtract line 5 from line 4. If the amount is zero or greater, enter zero _________________________ 6

7. Enter (as a negative number) any disallowed excess business loss incurred in the taxable year.

See instructions if you are a full- or part-year nonresident __________________________________ 7

8. Add lines 6 and 7. This is your Indiana NOL available to carryforward ______________ Indiana NOL 8

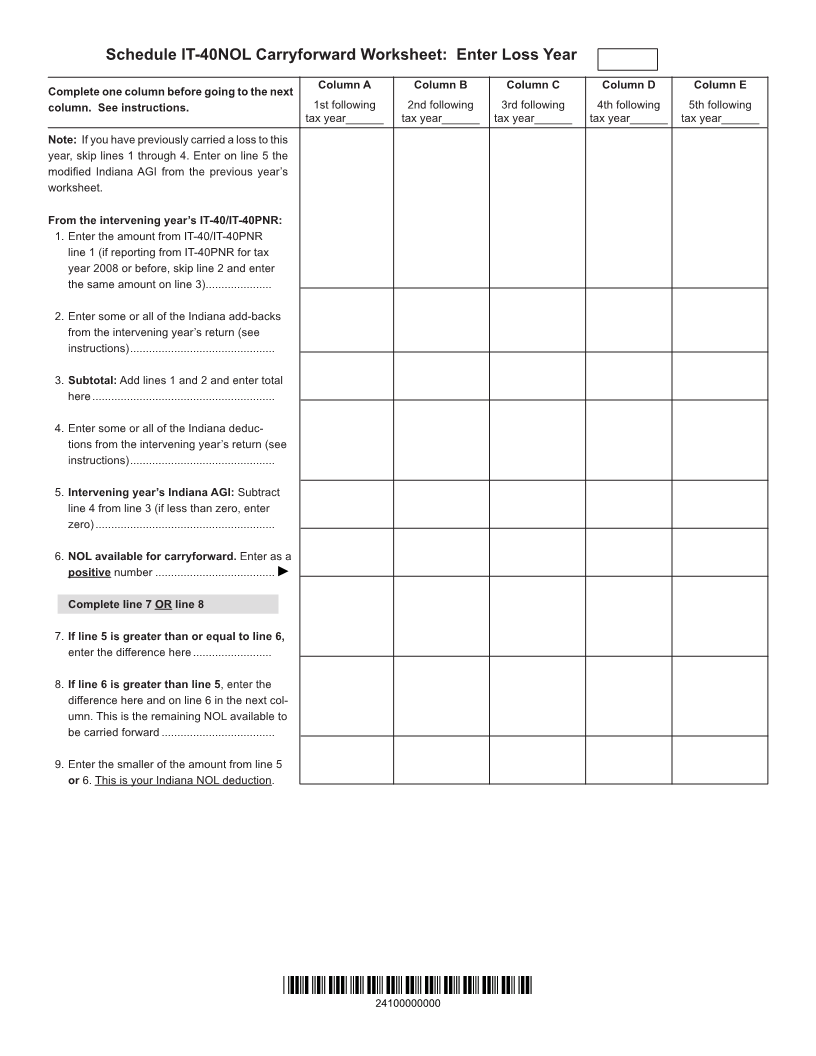

Part 2 - Record of Indiana NOL Application

(1) (2) (3) (4) (5)

Indiana NOL available for

Indiana AGI available to be deduction (from the Carryfor- Enter the amount from Indiana NOL deduction: Enter

Enter the year to which you offset (from the Carryforward ward Worksheet, line 6; enter either line 7 or line 8 of the the amount from line 9 of the

are carrying the loss. Worksheet, line 5) as positive amount) Carryforward Worksheet. Carryforward Worksheet

1st Year:

2nd Year:

3rd Year:

4th Year:

5th Year:

6th Year:

7th Year:

8th Year:

Attach additional sheets if necessary.

*24100000000*

24100000000