Enlarge image

Illinois Department of Revenue

2023 Schedule IL-E/EIC IL-1040 Instructions

General Information

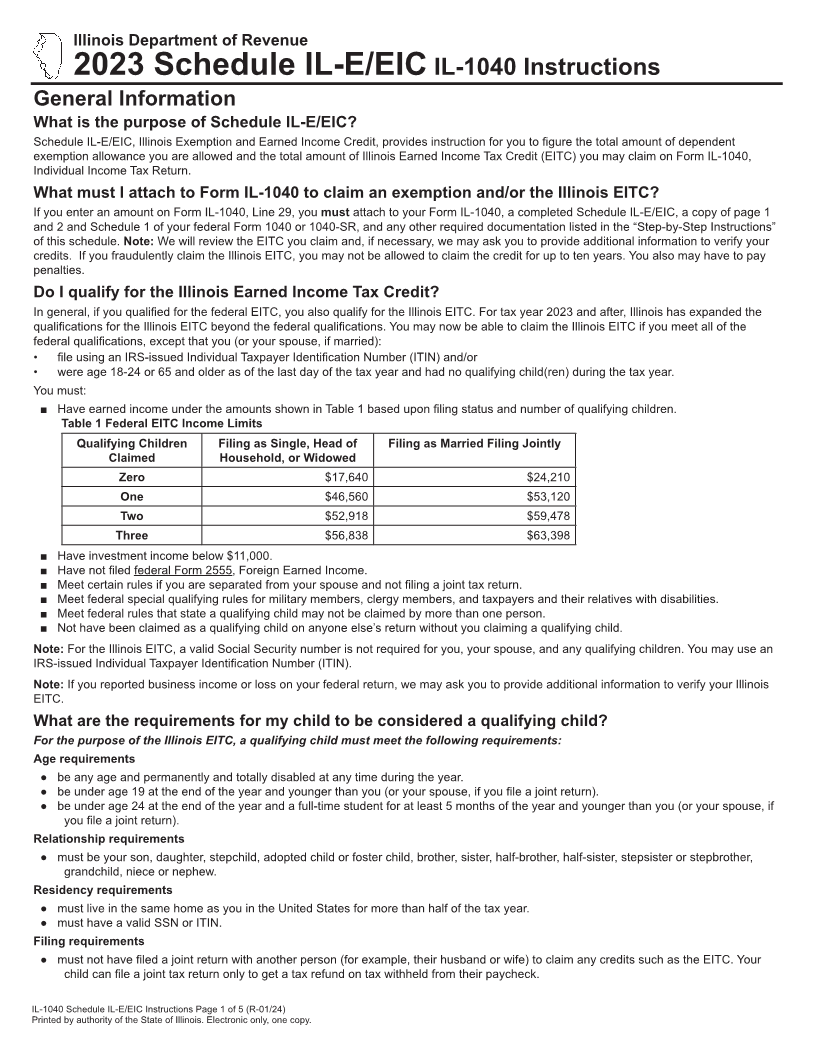

What is the purpose of Schedule IL-E/EIC?

Schedule IL-E/EIC, Illinois Exemption and Earned Income Credit, provides instruction for you to figure the total amount of dependent

exemption allowance you are allowed and the total amount of Illinois Earned Income Tax Credit (EITC) you may claim on Form IL-1040,

Individual Income Tax Return.

What must I attach to Form IL-1040 to claim an exemption and/or the Illinois EITC?

If you enter an amount on Form IL-1040, Line 29, you must attach to your Form IL-1040, a completed Schedule IL-E/EIC, a copy of page 1

and 2 and Schedule 1 of your federal Form 1040 or 1040-SR, and any other required documentation listed in the “Step-by-Step Instructions”

of this schedule. Note: We will review the EITC you claim and, if necessary, we may ask you to provide additional information to verify your

credits. If you fraudulently claim the Illinois EITC, you may not be allowed to claim the credit for up to ten years. You also may have to pay

penalties.

Do I qualify for the Illinois Earned Income Tax Credit?

In general, if you qualified for the federal EITC, you also qualify for the Illinois EITC. For tax year 2023 and after, Illinois has expanded the

qualifications for the Illinois EITC beyond the federal qualifications. You may now be able to claim the Illinois EITC if you meet all of the

federal qualifications, except that you (or your spouse, if married):

• file using an IRS-issued Individual Taxpayer Identification Number (ITIN) and/or

• were age 18-24 or 65 and older as of the last day of the tax year and had no qualifying child(ren) during the tax year.

You must:

■ Have earned income under the amounts shown in Table 1 based upon filing status and number of qualifying children.

Table 1 Federal EITC Income Limits

Qualifying Children Filing as Single, Head of Filing as Married Filing Jointly

Claimed Household, or Widowed

Zero $17,640 $24,210

One $46,560 $53,120

Two $52,918 $59,478

Three $56,838 $63,398

■ Have investment income below $11,000.

■ Have not filed federal Form 2555, Foreign Earned Income.

■ Meet certain rules if you are separated from your spouse and not filing a joint tax return.

■ Meet federal special qualifying rules for military members, clergy members, and taxpayers and their relatives with disabilities.

■ Meet federal rules that state a qualifying child may not be claimed by more than one person.

■ Not have been claimed as a qualifying child on anyone else’s return without you claiming a qualifying child.

Note: For the Illinois EITC, a valid Social Security number is not required for you, your spouse, and any qualifying children. You may use an

IRS-issued Individual Taxpayer Identification Number (ITIN).

Note: If you reported business income or loss on your federal return, we may ask you to provide additional information to verify your Illinois

EITC.

What are the requirements for my child to be considered a qualifying child?

For the purpose of the Illinois EITC, a qualifying child must meet the following requirements:

Age requirements

● be any age and permanently and totally disabled at any time during the year.

● be under age 19 at the end of the year and younger than you (or your spouse, if you file a joint return).

● be under age 24 at the end of the year and a full-time student for at least 5 months of the year and younger than you (or your spouse, if

you file a joint return).

Relationship requirements

● must be your son, daughter, stepchild, adopted child or foster child, brother, sister, half-brother, half-sister, stepsister or stepbrother,

grandchild, niece or nephew.

Residency requirements

● must live in the same home as you in the United States for more than half of the tax year.

● must have a valid SSN or ITIN.

Filing requirements

● must not have filed a joint return with another person (for example, their husband or wife) to claim any credits such as the EITC. Your

child can file a joint tax return only to get a tax refund on tax withheld from their paycheck.

IL-1040 Schedule IL-E/EIC Instructions Page 1 of 5 (R-01/24)

Printed by authority of the State of Illinois. Electronic only, one copy.