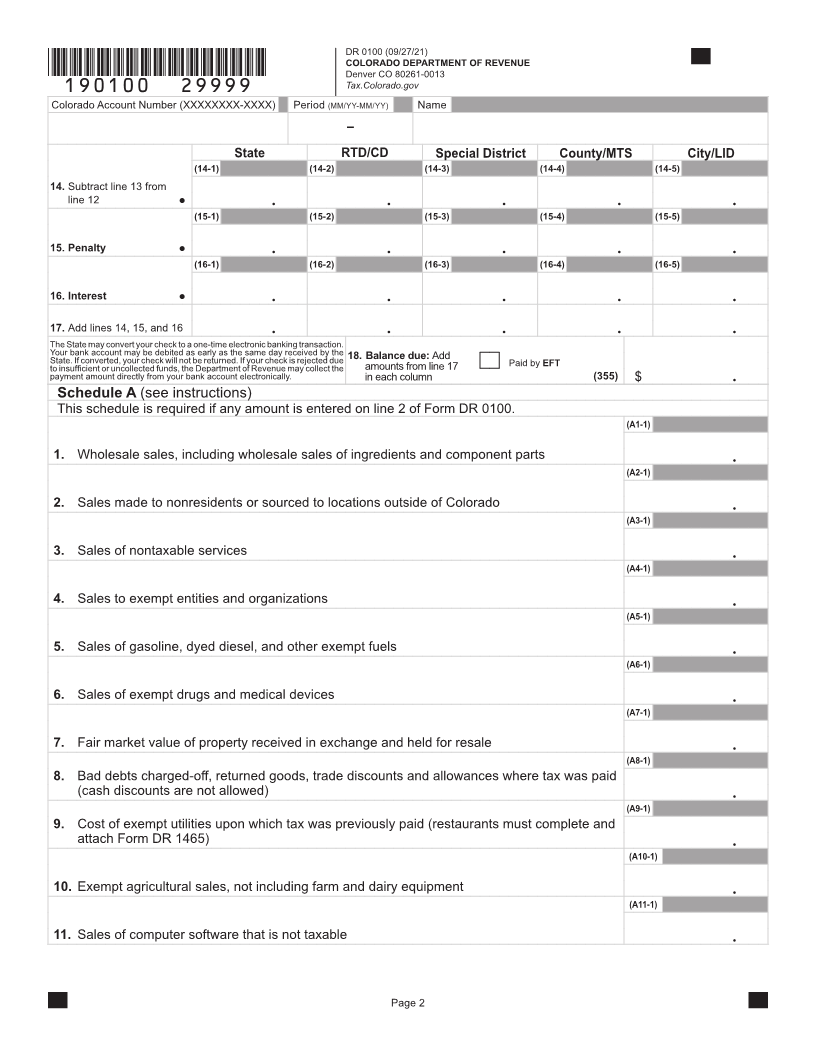

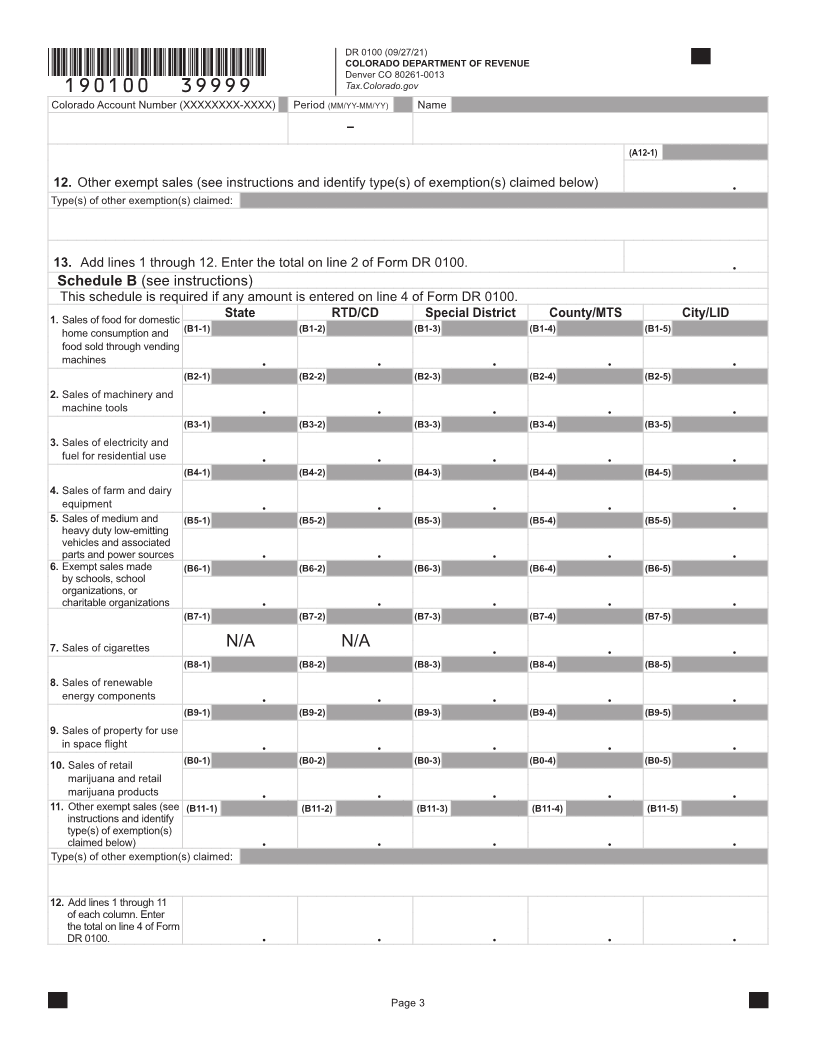

Enlarge image

DR 0100 (09/27/21)

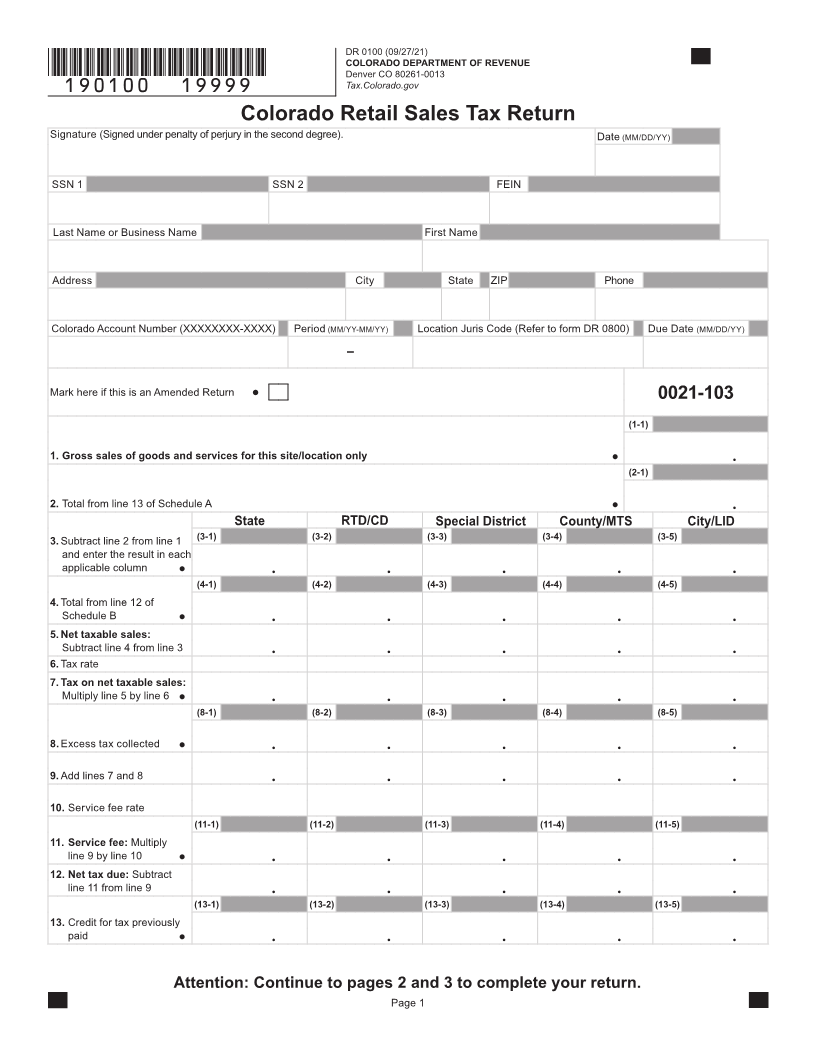

COLORADO DEPARTMENT OF REVENUE Colorado Retail

Denver CO 80261-0013

*DO*NOT*SEND* Tax.Colorado.gov Sales Tax Return

General Information Department before filing returns with an Excel

Retailers must file a sales tax return for every filing period, spreadsheet. Information can be found online at

even if the retailer made no sales during the period and no Tax.Colorado.gov/sales-tax-spreadsheet-filing.

tax is due. Typically, returns must be filed on a monthly basis.

See Part 7: Filing and Remittance in the Colorado Sales Tax Payment Information

Guide for additional information regarding filing frequency. The Department offers retailers several payment options for

remitting sales taxes.

A separate return must be filed for each business site or

location at which a retailer makes sales. If a retailer fails to Electronic Payments

file a return for any filing period, the Department will estimate Regardless of whether they file electronically or with a paper

the tax due and issue to the retailer a written notice of the return, retailers can remit payment electronically using one

estimated tax due. The Department may deactivate the sales of two payment methods. Retailers who remit electronic

tax account of a retailer who fails to file returns for successive payments should check the appropriate box on line 18 of the

filing periods. return to indicate their electronic payment.

• EFT Payment – Retailers can remit payment by

Electronic Filing Information

electronic funds transfer (EFT) via either ACH debit

The Department offers multiple electronic filing options that

or ACH credit. There is no processing fee for EFT

retailers may use as an alternative to filing paper returns.

payments. Retailers must register prior to making

• Revenue Online – Retailers must first create a Revenue payments via EFT and will not be able to make

Online account to file returns through Revenue Online. payments via EFT until 24-48 hours after registering.

Retailers who file returns through Revenue Online must See Electronic Funds Transferred (EFT) Program

file separate returns for each of the retailer’s business For Tax Payments (DR 5782) and Electronic Funds

sites or locations. Revenue Online can be accessed at Transfer (EFT) Account Setup For Tax Payments (DR

Colorado.gov/RevenueOnline. 5785) for additional information.

• XML Filing – Retailers may file returns electronically in • Credit Card and E-Check – Retailers can remit

an XML (Extensible Markup Language) format using payment electronically by credit card or electronic

any of the approved software options listed online check online at Colorado.gov/RevenueOnline. A

at Tax.Colorado.gov/software-developers-sales-tax. processing fee is charged for any payments remitted

Retailers do not need to obtain any special approval by credit card or electronic check.

from the Department to file using an approved

Paper Check

software option.

Regardless of whether they file electronically or with a paper

• Spreadsheet Filing – Retailers may file electronically return, retailers can remit payment with a paper check.

using an approved Microsoft Excel spreadsheet. Retailers should write “Sales Tax,” the account number, and

Each retailer must obtain approval from the the filing period on any paper check remitted to pay sales tax