Enlarge image

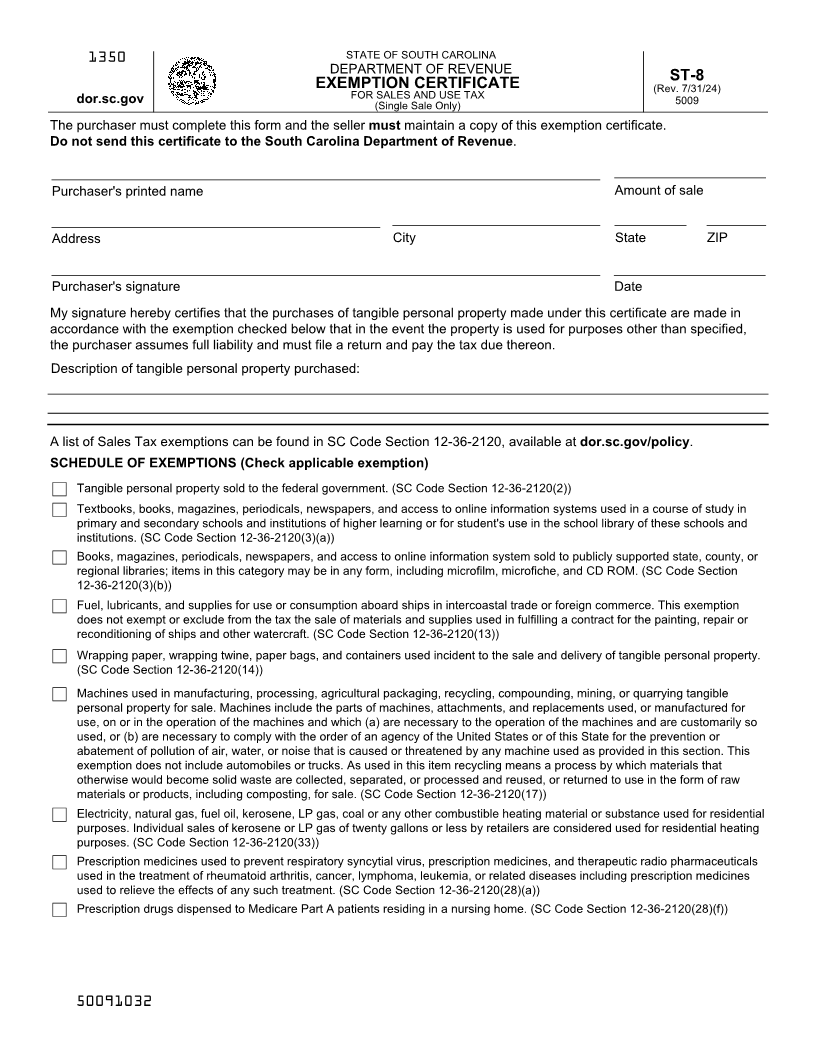

STATE OF SOUTH CAROLINA

DEPARTMENT OF REVENUE

ST-8

EXEMPTION CERTIFICATE (Rev. 7/31/24)

dor.sc.gov FOR SALES AND USE TAX 5009

(Single Sale Only)

The purchaser must complete this form and the seller must maintain a copy of this exemption certificate.

Do not send this certificate to the South Carolina Department of Revenue.

Purchaser's printed name Amount of sale

Address City State ZIP

Purchaser's signature Date

My signature hereby certifies that the purchases of tangible personal property made under this certificate are made in

accordance with the exemption checked below that in the event the property is used for purposes other than specified,

the purchaser assumes full liability and must file a return and pay the tax due thereon.

Description of tangible personal property purchased:

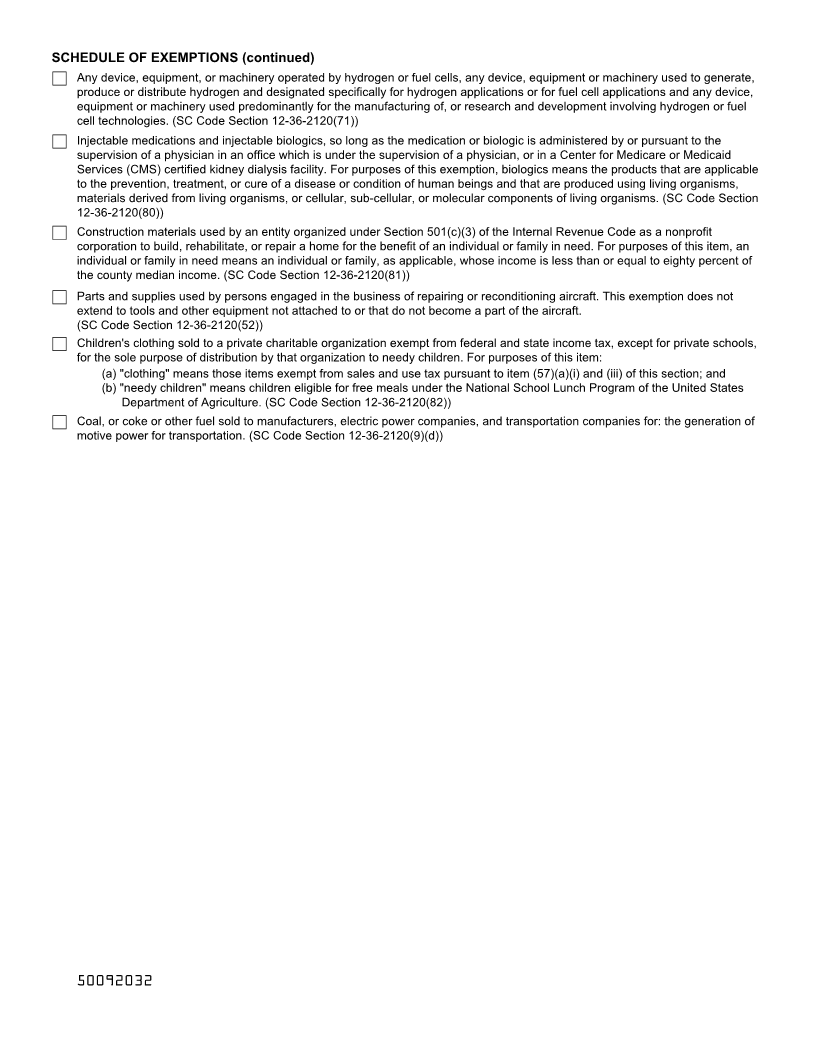

A list of Sales Tax exemptions can be found in SC Code Section 12-36-2120, available at dor.sc.gov/policy.

SCHEDULE OF EXEMPTIONS (Check applicable exemption)

Tangible personal property sold to the federal government. (SC Code Section 12-36-2120(2))

Textbooks, books, magazines, periodicals, newspapers, and access to online information systems used in a course of study in

primary and secondary schools and institutions of higher learning or for student's use in the school library of these schools and

institutions. (SC Code Section 12-36-2120(3)(a))

Books, magazines, periodicals, newspapers, and access to online information system sold to publicly supported state, county, or

regional libraries; items in this category may be in any form, including microfilm, microfiche, and CD ROM. (SC Code Section

12-36-2120(3)(b))

Fuel, lubricants, and supplies for use or consumption aboard ships in intercoastal trade or foreign commerce. This exemption

does not exempt or exclude from the tax the sale of materials and supplies used in fulfilling a contract for the painting, repair or

reconditioning of ships and other watercraft. (SC Code Section 12-36-2120(13))

Wrapping paper, wrapping twine, paper bags, and containers used incident to the sale and delivery of tangible personal property.

(SC Code Section 12-36-2120(14))

Machines used in manufacturing, processing, agricultural packaging, recycling, compounding, mining, or quarrying tangible

personal property for sale. Machines include the parts of machines, attachments, and replacements used, or manufactured for

use, on or in the operation of the machines and which (a) are necessary to the operation of the machines and are customarily so

used, or (b) are necessary to comply with the order of an agency of the United States or of this State for the prevention or

abatement of pollution of air, water, or noise that is caused or threatened by any machine used as provided in this section. This

exemption does not include automobiles or trucks. As used in this item recycling means a process by which materials that

otherwise would become solid waste are collected, separated, or processed and reused, or returned to use in the form of raw

materials or products, including composting, for sale. (SC Code Section 12-36-2120(17))

Electricity, natural gas, fuel oil, kerosene, LP gas, coal or any other combustible heating material or substance used for residential

purposes. Individual sales of kerosene or LP gas of twenty gallons or less by retailers are considered used for residential heating

purposes. (SC Code Section 12-36-2120(33))

Prescription medicines used to prevent respiratory syncytial virus, prescription medicines, and therapeutic radio pharmaceuticals

used in the treatment of rheumatoid arthritis, cancer, lymphoma, leukemia, or related diseases including prescription medicines

used to relieve the effects of any such treatment. (SC Code Section 12-36-2120(28)(a))

Prescription drugs dispensed to Medicare Part A patients residing in a nursing home. (SC Code Section 12-36-2120(28)(f))