Enlarge image

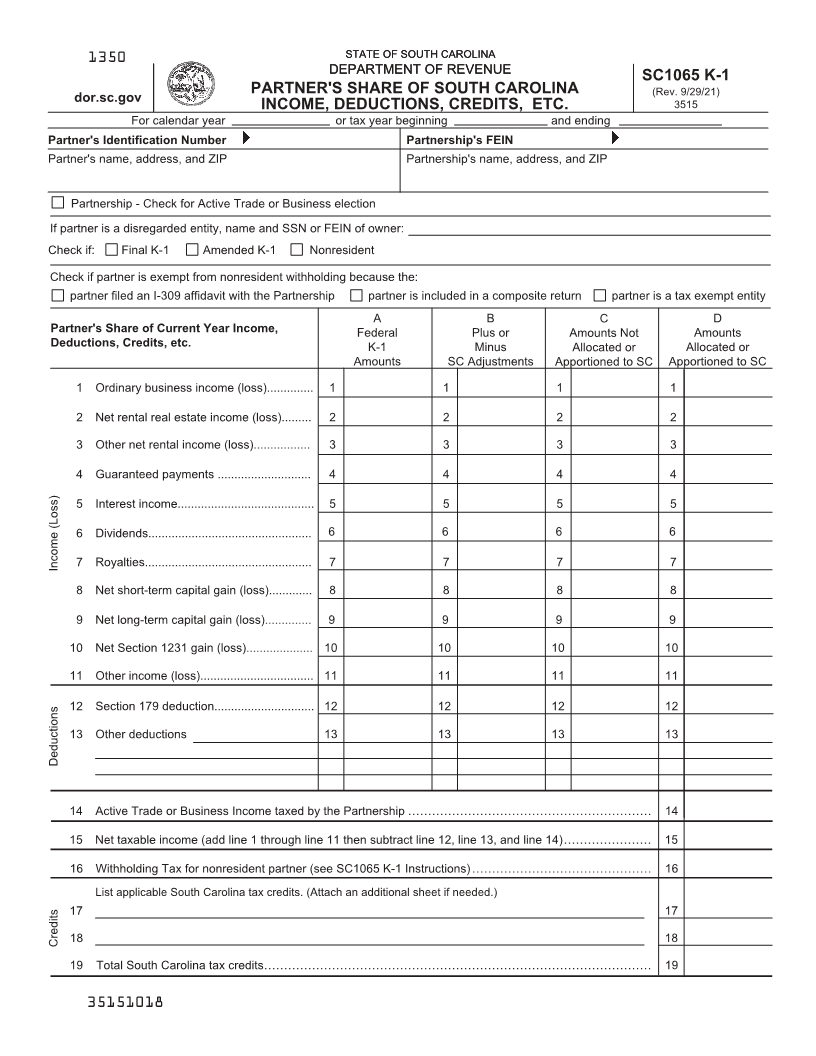

1350 STATE OF SOUTH CAROLINASTATE OF SOUTH CAROLINA

DEPARTMENT OF REVENUEDEPARTMENT OF REVENUE

SC1065 K-1

PARTNER'S SHARE OF SOUTH CAROLINA (Rev. 9/29/21)

dor.sc.gov

INCOME, DEDUCTIONS, CREDITS, ETC. 3515

For calendar year or tax year beginning and ending

Partner's Identification Number Partnership's FEIN

Partner's name, address, and ZIP Partnership's name, address, and ZIP

Partnership - Check for Active Trade or Business election

If partner is a disregarded entity, name and SSN or FEIN of owner:

Check if: Final K-1 Amended K-1 Nonresident

Check if partner is exempt from nonresident withholding because the:

partner filed an I-309 affidavit with the Partnership partner is included in a composite return partner is a tax exempt entity

A B C D

Partner's Share of Current Year Income, Federal Plus or Amounts Not Amounts

Deductions, Credits, etc. K-1 Minus Allocated or Allocated or

Amounts SC Adjustments Apportioned to SC Apportioned to SC

1 Ordinary business income (loss).............. 1 1 1 1

2 Net rental real estate income (loss)......... 2 2 2 2

3 Other net rental income (loss)................. 3 3 3 3

4 Guaranteed payments ............................ 4 4 4 4

5 Interest income......................................... 5 5 5 5

6 Dividends................................................. 6 6 6 6

Income (Loss) 7 Royalties.................................................. 7 7 7 7

8 Net short-term capital gain (loss)............. 8 8 8 8

9 Net long-term capital gain (loss).............. 9 9 9 9

10 Net Section 1231 gain (loss).................... 10 10 10 10

11 Other income (loss).................................. 11 11 11 11

12 Section 179 deduction.............................. 12 12 12 12

13 Other deductions 13 13 13 13

Deductions

14 Active Trade or Business Income taxed by the Partnership ............................................................. 14

15 Net taxable income (add line 1 through line 11 then subtract line 12, line 13, and line 14 )...................... 15

16 Withholding Tax for nonresident partner (see SC1065 K-1 Instructions)............................................. 16

List applicable South Carolina tax credits. (Attach an additional sheet if needed.)

17 17

Credits 18 18

19 Total South Carolina tax credits................................................................................................. 19

35151018