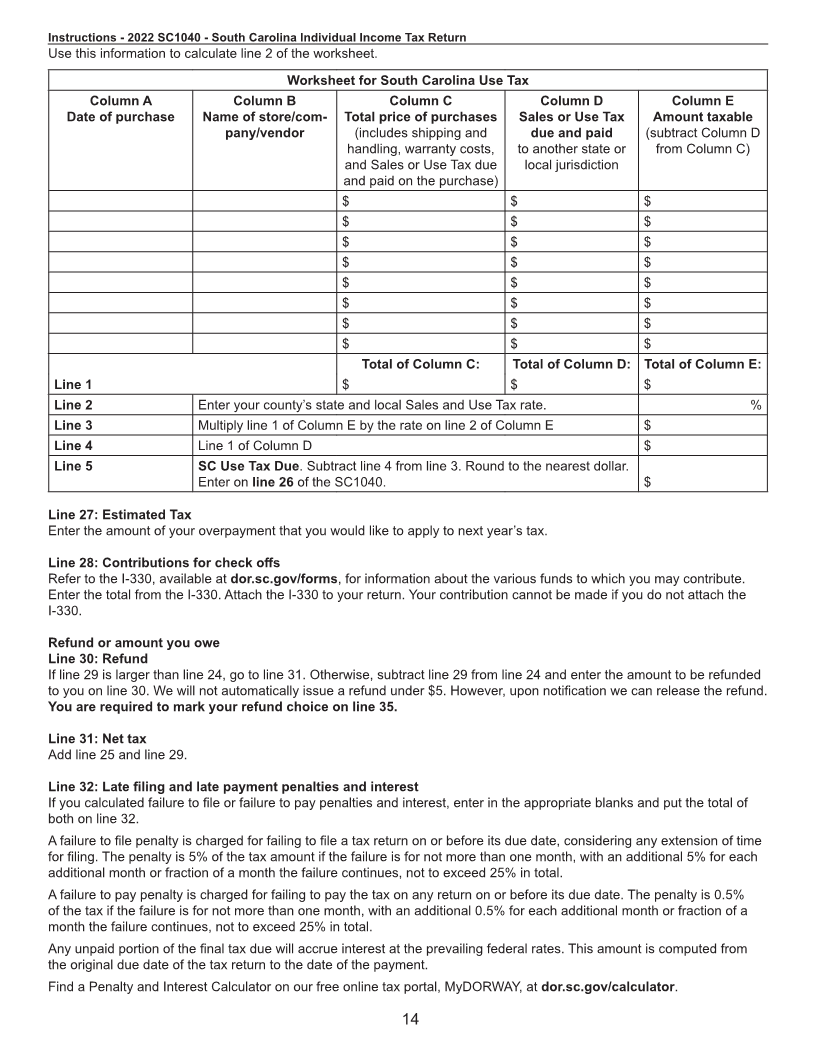

Enlarge image

SC1040 INSTRUCTIONS 2022 (Rev 10/13/2022)

Things to know before you begin:

● For tax year 2022, unless you have a valid extension, the due date is April 18, 2023 and the deadline to claim a

refund is April 18, 2026.

● Complete your federal return before you begin your SC1040. You will need information from your federal return

when preparing your South Carolina return.

● South Carolina conforms to the Internal Revenue Code as amended through December 31, 2021, except as oth-

erwise provided. If Internal Revenue Code sections adopted by South Carolina which expired on December 31,

2021 are extended, but otherwise not amended, by congressional enactment during 2022, these sections are also

extended for South Carolina Income Tax purposes in the same manner that they are extended for federal Income

Tax purposes.

● The references to form numbers and line descriptions on federal Income Tax forms were correct at the time of

printing. If they have changed and you are unable to determine the proper line to use, contact the SCDOR Individ-

ual Income Tax section at 1-844-898-8542 or by email at IITax@dor.sc.gov.

● Use these instructions as a guide when preparing your SC1040. They are not intended to cover all provisions of

the law.

● If you used federal schedules C, D, E, or F when filing your federal return or filed a Schedule NR, SC1040TC,

I-319, or I-335 with your South Carolina return, attach a copy of your federal return and schedules to your South

Carolina return.

● Beginning with tax year 2019, if you need to amend your return, file a new SC1040 and check the Amended Re-

turn box on the front. Complete the return as it should have been filed, including all schedules and attachments.

Complete the SCH AMD, Amended Return Schedule, and submit it with your amended SC1040.

● For tax years 2018 and before, use the SC1040X to amend your return. Forms are available at dor.sc.gov/forms.

Social Security Number, name, and address:

● Enter your Social Security Number (SSN). Check the appropriate box if the taxpayer is deceased.

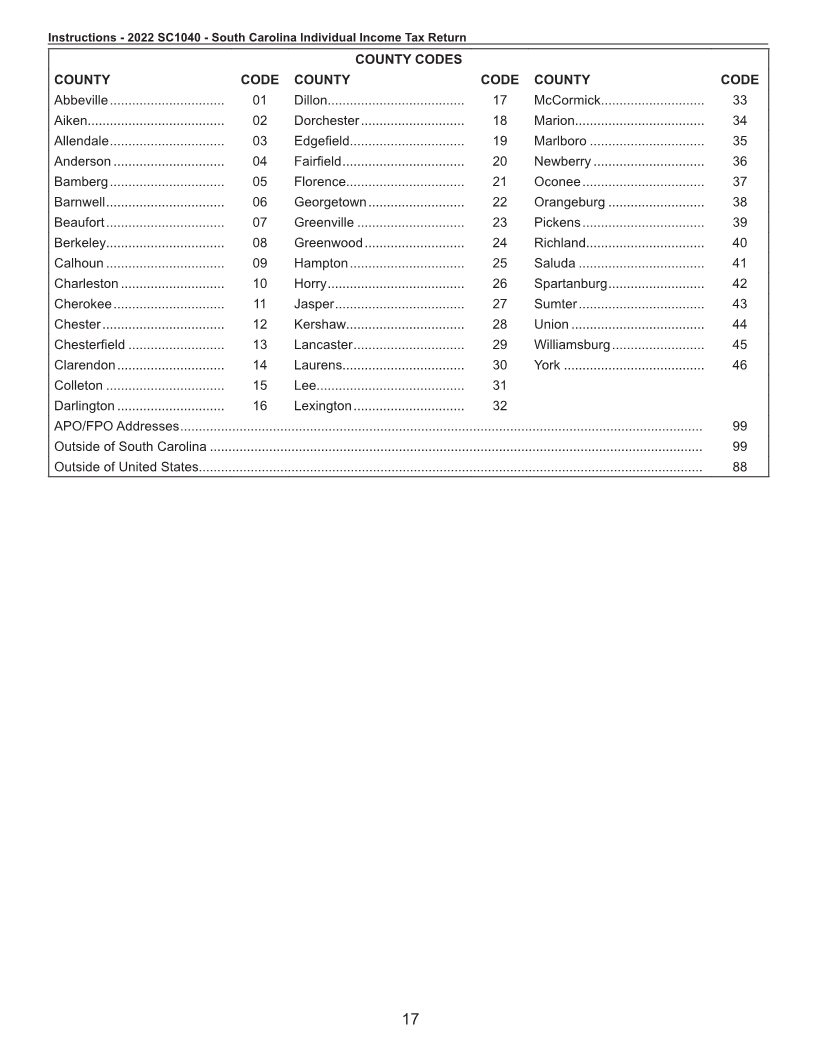

● Enter your name, mailing address, and the county code of the county where you live. You can find a list of county

codes on page 17. Check the box to let us know if this is a new address. To avoid delays, be sure your mailing

address is complete and accurate on your return.

● For a foreign address, check the appropriate box to let us know the address is outside the US. Print or type the

complete foreign address, including postal code.

● If you are married and filing a joint return, enter your spouse's name and SSN. Check the appropriate box if the

taxpayer is deceased.

● If you are married and filing separate returns, do not include your spouse's name or SSN in this section. En-

ter your spouse's SSN next to box 3 in the filing status section.

Social Security Privacy Act Disclosure

It is mandatory that you provide your Social Security Number on this tax form if you are an individual taxpayer. 42 U.S.C.

405(c)(2)(C)(i) permits a state to use an individual’s Social Security Number as means of identification in administration of

any tax. SC Regulation 117-201 mandates that any person required to make a return to the SCDOR must provide iden-

tifying numbers, as prescribed, for securing proper identification. Your Social Security Number is used for identification

purposes.

Individual Taxpayer Identification Number (ITIN)

If you are a nonresident or resident alien and cannot get an SSN, contact the IRS to apply for an Individual Taxpayer Iden-

tification Number (ITIN) for the purpose of filing Income Tax returns. South Carolina will accept this number in place of an

SSN to process your Individual Income Tax returns. For more information, contact the IRS at 1-800-829-1040 or visit

irs.gov. We cannot accept your return for processing without complete SSNs or ITINs.

Checkboxes:

● If you are filing an amended SC1040, check the Amended Return box. Complete the return as it should have

been filed. Complete the SCH AMD, Amended Return Schedule, and submit it with your amended SC1040. Your

amended return cannot be processed without the SCH AMD.

● If you are a nonresident for the entire year or a part-year resident electing to file as a nonresident, check the ap-

propriate box and attach your Schedule NR to the completed SC1040. Do not submit the Schedule NR sepa-

rately.

1