Enlarge image

SC1040 Instructions 2023 Individual Income Tax Instructions South Carolina Department of Revenue | dor.sc.gov | December 2023

Enlarge image | SC1040 Instructions 2023 Individual Income Tax Instructions South Carolina Department of Revenue | dor.sc.gov | December 2023 |

Enlarge image | Contents Contents � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � ii Before You Begin � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �1 Identification and Filing Status � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �1 Social Security Number, Name, and Address � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 1 Checkboxes � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �2 Dependent Exemption � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �2 Line Instructions � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �3 Federal Taxable Income � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �3 Additions to Federal Taxable Income � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 3 Subtractions From Federal Taxable Income � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 6 South Carolina Tax � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �14 Nonrefundable Credits � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �15 Tax Payments and Refundable Credits � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �17 Refund or Amount You Owe � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �21 Important Reminders � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � �23 |

Enlarge image | Before You Begin ● For tax year 2023, unless you have a valid extension, the due date is April 15, 2024, and the deadline to claim a refund is April 15, 2027� ● Complete your federal return before you begin your SC1040. You will need information from your federal return when preparing your South Carolina return� ● South Carolina conforms to the Internal Revenue Code as amended through December 31, 2022, except as otherwise provided. If Internal Revenue Code sections adopted by South Carolina which expired on December 31, 2022 are extended, but otherwise not amended, by congressional enactment during 2023, these sections are also extended for South Carolina Income Tax purposes in the same manner that they are extended for federal Income Tax purposes� ● The references to form numbers and line descriptions on federal Income Tax forms were correct at the time of printing. If they have changed and you are unable to determine the proper line to use, contact the SCDOR Individual Income Tax section at 1-844-898-8542. ● Use these instructions as a guide when preparing your SC1040. They are not intended to cover all provisions of the law� ● If you used federal schedules C, D, E, or F when filing your federal return or filed a Schedule NR, SC1040TC, I-319, or I-335 with your South Carolina return, attach a copy of your federal return and schedules to your South Carolina return� ● If you need to amend your return, file a new SC1040 and check the Amended Return box on the front. Complete the return as it should have been filed, including all schedules and attachments. Complete the SCH AMD, Amended Return Schedule, and submit it with your amended SC1040� Identification and Filing Status Social Security Number, Name, and Address ● Enter your Social Security Number (SSN)� Check the appropriate box if the taxpayer is deceased� ● Enter your name, mailing address, and the county code of the county where you live� You can find a list of county codes on page 24. Check the box to let us know if this is a new address. To avoid delays, be sure your mailing address is complete and accurate on your return. ● For a foreign address, check the appropriate box to let us know the address is outside the US. Print or type the complete foreign address, including postal code. ● If you are married and filing a joint return, enter your spouse's name and SSN. Check the appropriate box if the taxpayer is deceased� ● If you are married and filing separate returns, do not include your spouse's name or SSN in this section. Enter your spouse's SSN next to box 3 in the filing status section� 1 SCDOR | SC1040 Instructions |

Enlarge image | Social Security Privacy Act Disclosure It is mandatory that you provide your Social Security Number on this tax form if you are an individual taxpayer� 42 U�S�C� 405(c)(2)(C)(i) permits a state to use an individual’s Social Security Number as means of identification in administration of any tax. SC Regulation 117-201 mandates that any person required to make a return to the SCDOR must provide identifying numbers, as prescribed, for securing proper identification. Your Social Security Number is used for identification purposes. Individual Taxpayer Identification Number (ITIN) If you are a nonresident or resident alien and cannot get an SSN, contact the IRS to apply for an Individual Taxpayer Identification Number (ITIN) for the purpose of filing Income Tax returns. South Carolina will accept this number in place of an SSN to process your Individual Income Tax returns. For more information, contact the IRS at 1-800-829-1040 or visit irs.gov� We cannot accept your return for processing without complete SSNs or ITINs. Checkboxes 1� If you are filing an amended SC1040, check the Amended Return box� Complete the return as it should have been filed. Complete the SCH AMD, Amended Return Schedule, and submit it with your amended SC1040� Your amended return cannot be processed without the SCH AMD. 2� If you are a nonresident for the entire year or a part-year resident electing to file as a nonresident, check the appropriate box and attach your Schedule NR to the completed SC1040. Do not submit the Schedule NR separately. 3� If you are filing a composite return for a partnership or S Corporation, check the appropriate box. See the I-348, Composite Filing Instructions, available at dor.sc.gov/forms for more information on filing a composite return. Do not check the box if you are an individual. 4� If you filed a federal or state extension, check the appropriate box. 5� If you served in a Military Combat Zone during the filing period, check the appropriate box and enter the combat zone� Filing Status Choose the same filing status that you used on your federal return. Check only one box. Dependent Exemption ● You can take a South Carolina dependent exemption for each eligible dependent, including both qualifying children and qualifying relatives. ● Enter the total number of eligible dependents. The total number of dependents claimed on your South Carolina return must equal the number of dependents claimed on your federal return. ● Attach the federal 8332, Release/Revocation of Release of Claim to Exemption for Child by Custodial Parent, if you are required to file this form with your federal return. ● Claim your deduction for dependent exemptions on line w. ● If you are claiming a deduction for dependent children under age 6, enter the number of children under age 6. Claim your deduction for dependents under age 6 on line t. ● Enter the number of taxpayers who are age 65 or older� ● Enter the first and last name, SSN, relationship, and date of birth of each dependent. 2 SCDOR | SC1040 Instructions |

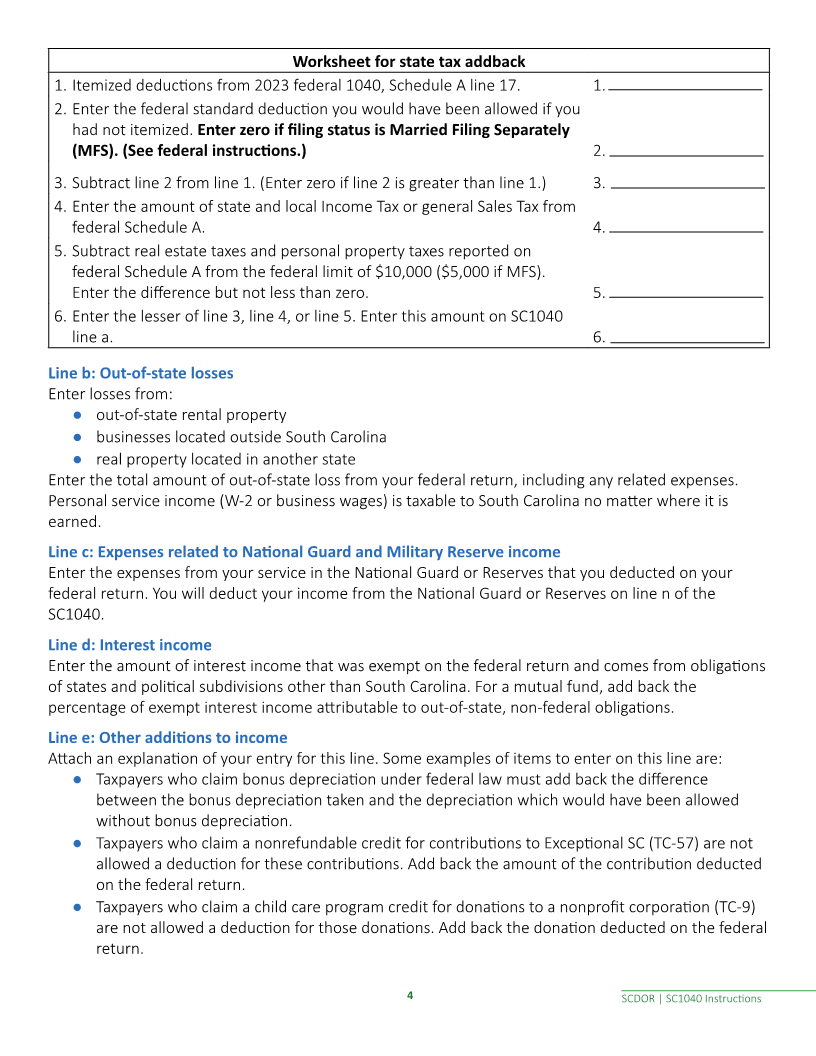

Enlarge image | Line Instructions Round all amounts to the nearest whole dollar. Federal Taxable Income Line 1: Federal Taxable Income Enter your taxable income from your federal form� If your federal taxable income is zero or less, enter zero here and enter your negative amount on line r. STOP! Nonresident/Part-year filers must complete the Schedule NR and go to line 5. See the Schedule NR instructions, available at dor.sc.gov/forms� Additions to Federal Taxable Income Enter all numbers on line a through line e as positive numbers even if they are negative numbers on the federal return� Line a through line e are adjustments which must be added to your federal taxable income to determine your South Carolina taxable income. Line 2 is the total of these additions. Line a: State tax addback If you itemized your deductions on your federal Income Tax return and deducted state and local Income Tax or general Sales Tax, you may be required to add back all or part of this amount to your federal taxable income when computing your South Carolina taxable income. Federal law limits your total deduction for state and local Income, Sales, and Property Taxes to a combined total deduction of $10,000 ($5,000 if Married Filing Separately). You can’t deduct any state or local taxes paid above this amount� In determining the state tax addback for a taxpayer whose tax deduction is limited to $10,000, you may first apply real or personal Property Taxes reported on federal Schedule A, lines 5b and 5c before applying state and local Income Taxes or general Sales Taxes reported on federal Schedule A, line 5a. The state tax addback required for South Carolina is the lesser of your: a� itemized deductions in excess of the standard deduction that would have been allowed if you had used the standard deduction for federal Income Tax purposes; b� state and local Income Taxes or general Sales Taxes from your federal 1040, Schedule A, line 5a; or c� the $10,000 federal tax deduction limit less deductible Property Taxes. Use the worksheet below to compute the state tax addback on the SC1040� Do not submit this worksheet with your return� Keep it with your tax records� 3 SCDOR | SC1040 Instructions |

Enlarge image |

Worksheet for state tax addback

1� Itemized deductions from 2023 federal 1040, Schedule A line 17. 1�

2� Enter the federal standard deduction you would have been allowed if you

had not itemized� Enter zero if filing status is Married Filing Separately

(MFS). (See federal instructions.) 2�

3� Subtract line 2 from line 1� (Enter zero if line 2 is greater than line 1�) 3�

4� Enter the amount of state and local Income Tax or general Sales Tax from

federal Schedule A� 4�

5� Subtract real estate taxes and personal property taxes reported on

federal Schedule A from the federal limit of $10,000 ($5,000 if MFS).

Enter the difference but not less than zero. 5�

6� Enter the lesser of line 3, line 4, or line 5� Enter this amount on SC1040

line a� 6�

Line b: Out-of-state losses

Enter losses from:

● out-of-state rental property

● businesses located outside South Carolina

● real property located in another state

Enter the total amount of out-of-state loss from your federal return, including any related expenses.

Personal service income (W-2 or business wages) is taxable to South Carolina no matter where it is

earned�

Line c: Expenses related to National Guard and Military Reserve income

Enter the expenses from your service in the National Guard or Reserves that you deducted on your

federal return. You will deduct your income from the National Guard or Reserves on line n of the

SC1040�

Line d: Interest income

Enter the amount of interest income that was exempt on the federal return and comes from obligations

of states and political subdivisions other than South Carolina. For a mutual fund, add back the

percentage of exempt interest income attributable to out-of-state, non-federal obligations.

Line e: Other additions to income

Attach an explanation of your entry for this line. Some examples of items to enter on this line are:

● Taxpayers who claim bonus depreciation under federal law must add back the difference

between the bonus depreciation taken and the depreciation which would have been allowed

without bonus depreciation.

● Taxpayers who claim a nonrefundable credit for contributions to Exceptional SC (TC-57) are not

allowed a deduction for these contributions. Add back the amount of the contribution deducted

on the federal return�

● Taxpayers who claim a child care program credit for donations to a nonprofit corporation (TC-9)

are not allowed a deduction for those donations. Add back the donation deducted on the federal

return�

4 SCDOR | SC1040 Instructions

|

Enlarge image | ● Taxpayers who claim credits such as the Community Development Credit (TC-14), the Industry Partnership Fund Credit (TC-36), and the Credit for Child Care Program (TC-9), may not claim a deduction for the same qualified contribution which results in the credit. Add back the amount deducted on the federal return� ● Add back the federal net operating loss when it is larger than the South Carolina net operating loss being claimed� ● Add back any expenses deducted on the federal return related to any income not taxed by South Carolina. Some examples are investment interest to out-of-state partnerships and interest paid to purchase US obligations. ● Add back foreign area allowances, cost of living allowances, and income from US possessions� ● For qualifying investments made after June 30, 1998, taxpayers must reduce the basis of the qualifying property to the extent the Capital Investment Tax Credit is claimed. Add back any resulting reduction in depreciation. ● Add back the qualified business income deduction under IRC Section 199A. ● Add back any charitable contribution of land deducted under IRC Section 170 unless it meets the donative intent requirements of SC Code Section 12-6-5590. ● Include any withdrawals during the tax year from a Catastrophe Savings Account that were: 1� necessary because contributions were more than the allowable limits; or 2� more than the amount needed to cover qualified catastrophe expenses. Do not include any withdrawals made by the surviving spouse of the account owner� Qualified catastrophe expenses are expenses paid or incurred because of a major disaster as declared by the Governor. ● A business must add back any amount paid for services performed by an unauthorized alien if the amount is $600 or more a year. Depending on how a particular item was reported or deducted, the following may be additions or subtractions. ● A change in the accounting method to conform in the same manner and the same amount to the federal. At the end of the federal adjustment, any balance will continue until fully adjusted. ● Adjust the installment method of reporting if: ■ the entire sale has been reported for state purposes, or ■ the entire sale was reported for federal purposes and you wish to continue on an installment basis for state purposes� ● Adjust the federal gain or loss to reflect any difference in the South Carolina basis and federal basis� Line 2: Add line a through line e� 5 SCDOR | SC1040 Instructions |

Enlarge image | Subtractions From Federal Taxable Income Enter all numbers on line f through line w as positive numbers even if they are negative numbers on the federal return� Line f through line w are adjustments which are subtracted from your federal taxable income to determine your South Carolina taxable income� Line f: State tax refund If you included your state tax refund on your federal 1040, enter that amount on this line� Line g: Total and permanent disability retirement income If disability retirement income was taxed on your federal Income Tax return and you are totally and permanently disabled, you may be able to deduct this income from your South Carolina taxable income� You must be totally and permanently disabled, unable to be substantially gainfully employed, receiving income from a disability retirement plan, and eligible for the homestead exemption under SC Code Section 12-37-250. Attach a copy of the physician’s statement establishing that you are totally and permanently disabled� The deduction is limited to payments received from retirement plans. Third-party sick pay reported on a W-2 does not qualify for the total and permanent disability retirement deduction. If you deduct total and permanent disability retirement income on this line, do not include that income in your qualified retirement income in the worksheets for line p-1 or line p-2. A surviving spouse may take a disability retirement deduction for amounts received in the year the disabled spouse died. In following years, a surviving spouse is eligible for the retirement deduction on line p but not the disability deduction. Line h: Out-of-state income/gain Enter: ● income from out-of-state rental property ● income from a business located outside South Carolina, or ● gain from real property located in another state� Enter the amount as reported on your federal return� Check the appropriate box to indicate the type of income or gain� Personal service income (W-2 or business wages) is taxable to South Carolina no matter where it is earned. Line i: Net capital gain deduction Net capital gains included in taxable income are reduced by 44% for South Carolina Income Tax purposes� Net capital gain means the excess of the net long-term capital gain for the tax year over the net short- term capital loss for the tax year. The South Carolina holding period for long-term capital gains is the same as the federal holding period. Income received from installment sales and capital gain distribution qualifies for this deduction if the more than one year holding period has been met. Multiply the net capital gain by 44% and enter the result� 6 SCDOR | SC1040 Instructions |

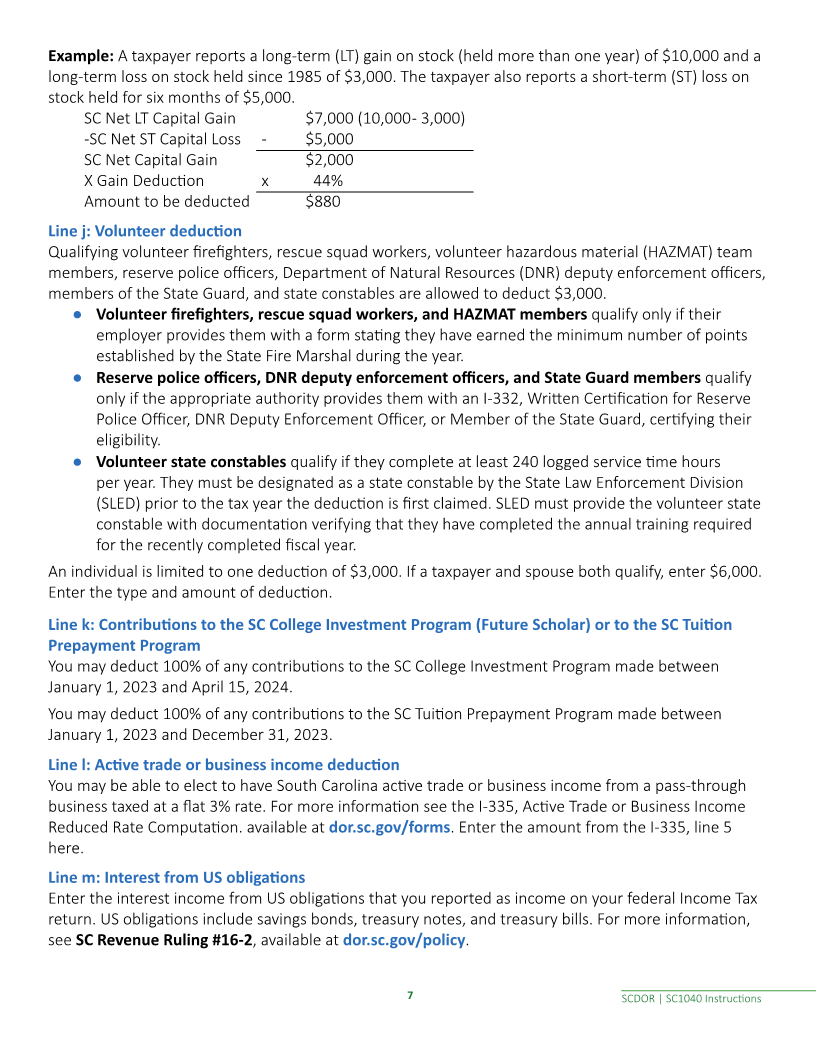

Enlarge image | Example: A taxpayer reports a long-term (LT) gain on stock (held more than one year) of $10,000 and a long-term loss on stock held since 1985 of $3,000. The taxpayer also reports a short-term (ST) loss on stock held for six months of $5,000. SC Net LT Capital Gain $7,000 (10,000 - 3,000) -SC Net ST Capital Loss - $5,000 SC Net Capital Gain $2,000 X Gain Deduction x 44% Amount to be deducted $880 Line j: Volunteer deduction Qualifying volunteer firefighters, rescue squad workers, volunteer hazardous material (HAZMAT) team members, reserve police officers, Department of Natural Resources (DNR) deputy enforcement officers, members of the State Guard, and state constables are allowed to deduct $3,000. ● Volunteer firefighters, rescue squad workers, and HAZMAT members qualify only if their employer provides them with a form stating they have earned the minimum number of points established by the State Fire Marshal during the year. ● Reserve police officers, DNR deputy enforcement officers, and State Guard members qualify only if the appropriate authority provides them with an I-332, Written Certification for Reserve Police Officer, DNR Deputy Enforcement Officer, or Member of the State Guard, certifying their eligibility� ● Volunteer state constables qualify if they complete at least 240 logged service time hours per year. They must be designated as a state constable by the State Law Enforcement Division (SLED) prior to the tax year the deduction is first claimed. SLED must provide the volunteer state constable with documentation verifying that they have completed the annual training required for the recently completed fiscal year. An individual is limited to one deduction of $3,000. If a taxpayer and spouse both qualify, enter $6,000. Enter the type and amount of deduction. Line k: Contributions to the SC College Investment Program (Future Scholar) or to the SC Tuition Prepayment Program You may deduct 100% of any contributions to the SC College Investment Program made between January 1, 2023 and April 15, 2024. You may deduct 100% of any contributions to the SC Tuition Prepayment Program made between January 1, 2023 and December 31, 2023. Line l: Active trade or business income deduction You may be able to elect to have South Carolina active trade or business income from a pass-through business taxed at a flat 3% rate. For more information see the I-335, Active Trade or Business Income Reduced Rate Computation. available at dor.sc.gov/forms. Enter the amount from the I-335, line 5 here� Line m: Interest from US obligations Enter the interest income from US obligations that you reported as income on your federal Income Tax return. US obligations include savings bonds, treasury notes, and treasury bills. For more information, see SC Revenue Ruling #16-2, available at dor.sc.gov/policy� 7 SCDOR | SC1040 Instructions |

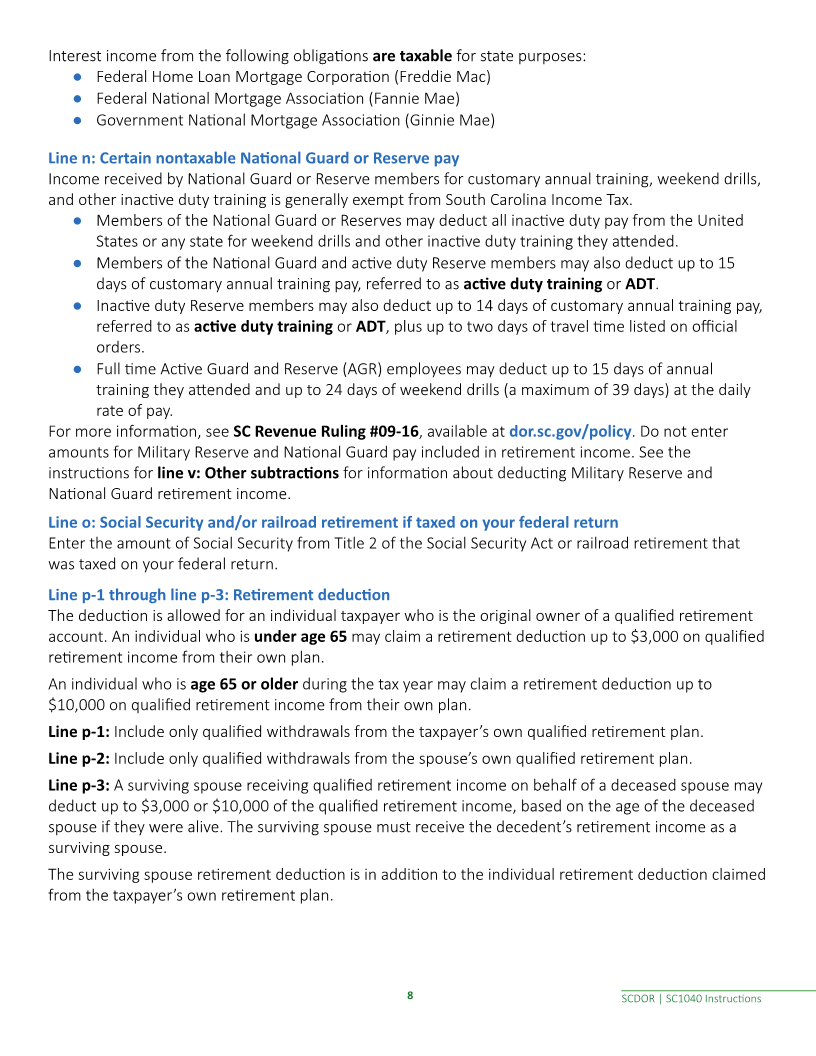

Enlarge image | Interest income from the following obligations are taxable for state purposes: ● Federal Home Loan Mortgage Corporation (Freddie Mac) ● Federal National Mortgage Association (Fannie Mae) ● Government National Mortgage Association (Ginnie Mae) Line n: Certain nontaxable National Guard or Reserve pay Income received by National Guard or Reserve members for customary annual training, weekend drills, and other inactive duty training is generally exempt from South Carolina Income Tax. ● Members of the National Guard or Reserves may deduct all inactive duty pay from the United States or any state for weekend drills and other inactive duty training they attended. ● Members of the National Guard and active duty Reserve members may also deduct up to 15 days of customary annual training pay, referred to as active duty training or ADT� ● Inactive duty Reserve members may also deduct up to 14 days of customary annual training pay, referred to as active duty training or ADT, plus up to two days of travel time listed on official orders� ● Full time Active Guard and Reserve (AGR) employees may deduct up to 15 days of annual training they attended and up to 24 days of weekend drills (a maximum of 39 days) at the daily rate of pay� For more information, see SC Revenue Ruling #09-16, available at dor.sc.gov/policy� Do not enter amounts for Military Reserve and National Guard pay included in retirement income. See the instructions for line v: Other subtractions for information about deducting Military Reserve and National Guard retirement income. Line o: Social Security and/or railroad retirement if taxed on your federal return Enter the amount of Social Security from Title 2 of the Social Security Act or railroad retirement that was taxed on your federal return� Line p-1 through line p-3: Retirement deduction The deduction is allowed for an individual taxpayer who is the original owner of a qualified retirement account� An individual who is under age 65 may claim a retirement deduction up to $3,000 on qualified retirement income from their own plan. An individual who is age 65 or older during the tax year may claim a retirement deduction up to $10,000 on qualified retirement income from their own plan. Line p-1: Include only qualified withdrawals from the taxpayer’s own qualified retirement plan. Line p-2: Include only qualified withdrawals from the spouse’s own qualified retirement plan. Line p-3: A surviving spouse receiving qualified retirement income on behalf of a deceased spouse may deduct up to $3,000 or $10,000 of the qualified retirement income, based on the age of the deceased spouse if they were alive. The surviving spouse must receive the decedent’s retirement income as a surviving spouse� The surviving spouse retirement deduction is in addition to the individual retirement deduction claimed from the taxpayer’s own retirement plan. 8 SCDOR | SC1040 Instructions |

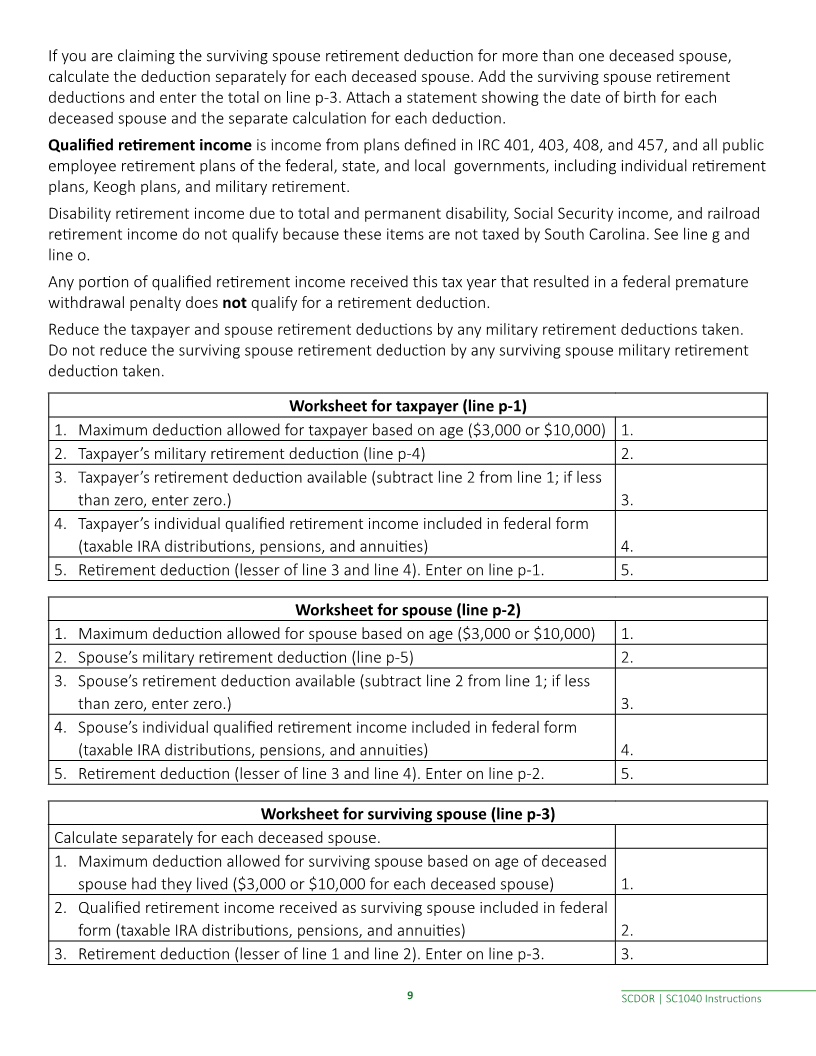

Enlarge image | If you are claiming the surviving spouse retirement deduction for more than one deceased spouse, calculate the deduction separately for each deceased spouse. Add the surviving spouse retirement deductions and enter the total on line p-3. Attach a statement showing the date of birth for each deceased spouse and the separate calculation for each deduction. Qualified retirement income is income from plans defined in IRC 401, 403, 408, and 457, and all public employee retirement plans of the federal, state, and local governments, including individual retirement plans, Keogh plans, and military retirement. Disability retirement income due to total and permanent disability, Social Security income, and railroad retirement income do not qualify because these items are not taxed by South Carolina. See line g and line o� Any portion of qualified retirement income received this tax year that resulted in a federal premature withdrawal penalty does not qualify for a retirement deduction. Reduce the taxpayer and spouse retirement deductions by any military retirement deductions taken. Do not reduce the surviving spouse retirement deduction by any surviving spouse military retirement deduction taken. Worksheet for taxpayer (line p-1) 1. Maximum deduction allowed for taxpayer based on age ($3,000 or $10,000) 1� 2. Taxpayer’s military retirement deduction (line p-4) 2� 3. Taxpayer’s retirement deduction available (subtract line 2 from line 1; if less than zero, enter zero�) 3� 4. Taxpayer’s individual qualified retirement income included in federal form (taxable IRA distributions, pensions, and annuities) 4� 5. Retirement deduction (lesser of line 3 and line 4). Enter on line p-1. 5� Worksheet for spouse (line p-2) 1. Maximum deduction allowed for spouse based on age ($3,000 or $10,000) 1� 2. Spouse’s military retirement deduction (line p-5) 2� 3. Spouse’s retirement deduction available (subtract line 2 from line 1; if less than zero, enter zero�) 3� 4. Spouse’s individual qualified retirement income included in federal form (taxable IRA distributions, pensions, and annuities) 4� 5. Retirement deduction (lesser of line 3 and line 4). Enter on line p-2. 5� Worksheet for surviving spouse (line p-3) Calculate separately for each deceased spouse� 1. Maximum deduction allowed for surviving spouse based on age of deceased spouse had they lived ($3,000 or $10,000 for each deceased spouse) 1� 2. Qualified retirement income received as surviving spouse included in federal form (taxable IRA distributions, pensions, and annuities) 2� 3. Retirement deduction (lesser of line 1 and line 2). Enter on line p-3. 3� 9 SCDOR | SC1040 Instructions |

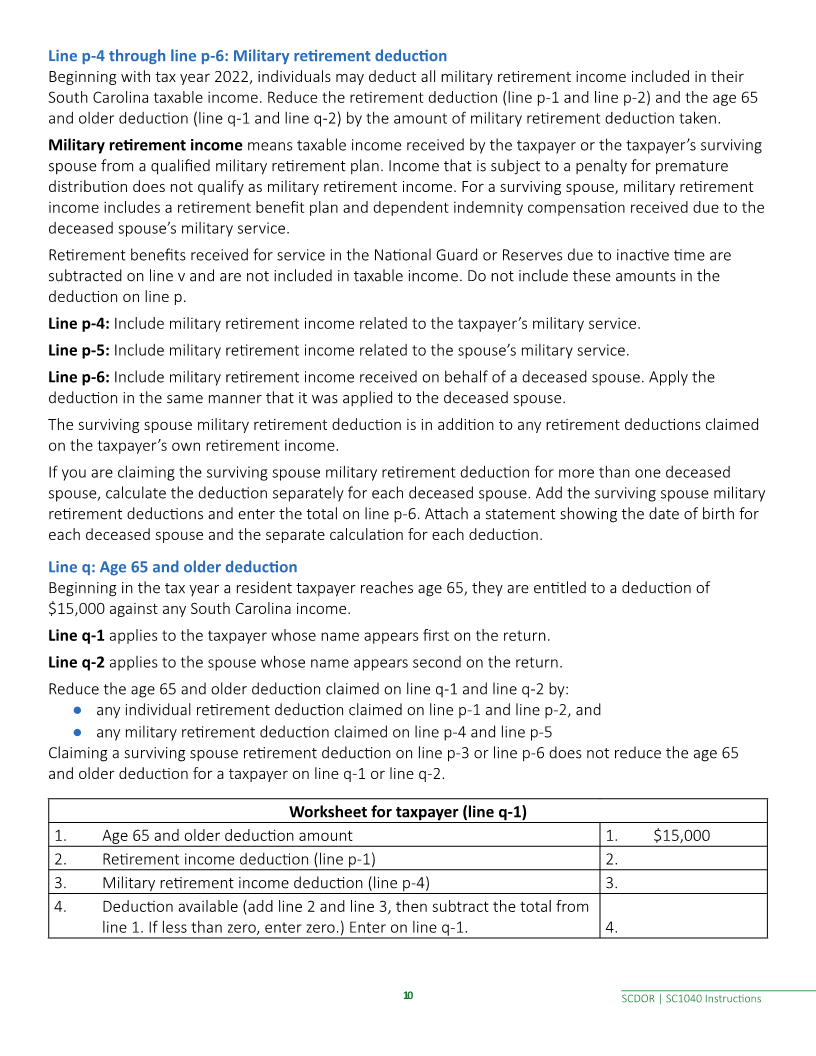

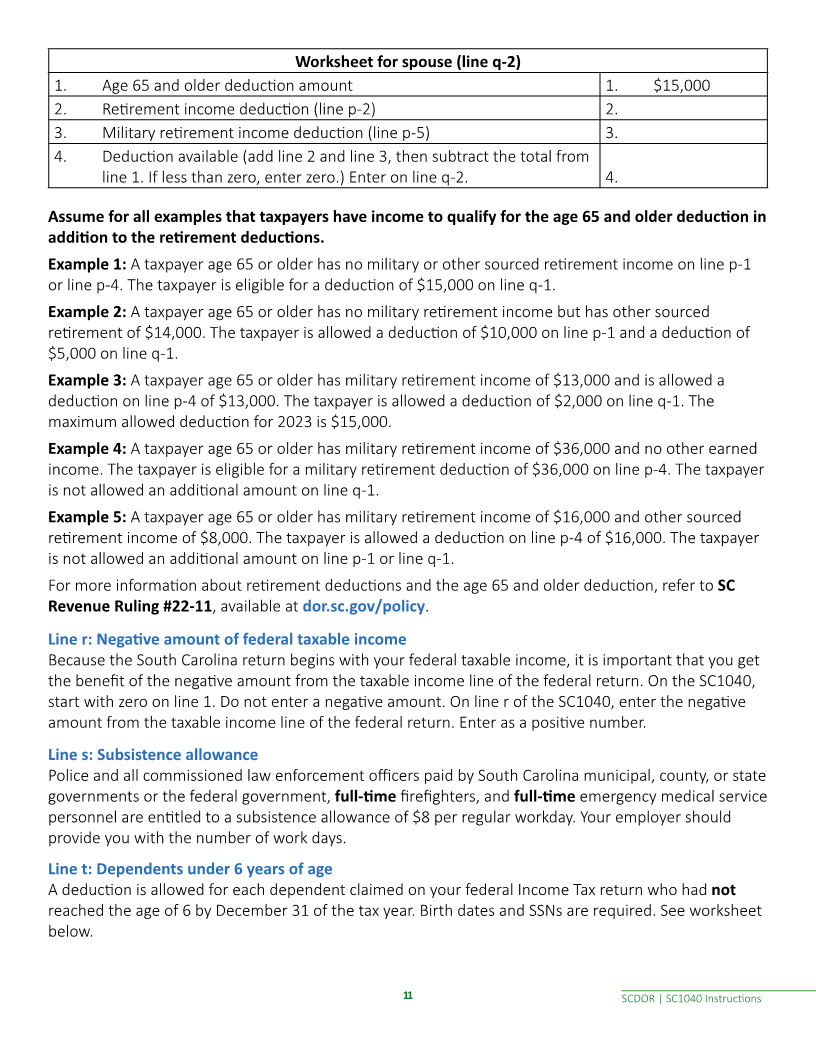

Enlarge image | Line p-4 through line p-6: Military retirement deduction Beginning with tax year 2022, individuals may deduct all military retirement income included in their South Carolina taxable income. Reduce the retirement deduction (line p-1 and line p-2) and the age 65 and older deduction (line q-1 and line q-2) by the amount of military retirement deduction taken. Military retirement income means taxable income received by the taxpayer or the taxpayer’s surviving spouse from a qualified military retirement plan. Income that is subject to a penalty for premature distribution does not qualify as military retirement income. For a surviving spouse, military retirement income includes a retirement benefit plan and dependent indemnity compensation received due to the deceased spouse’s military service� Retirement benefits received for service in the National Guard or Reserves due to inactive time are subtracted on line v and are not included in taxable income� Do not include these amounts in the deduction on line p. Line p-4: Include military retirement income related to the taxpayer’s military service. Line p-5: Include military retirement income related to the spouse’s military service. Line p-6: Include military retirement income received on behalf of a deceased spouse. Apply the deduction in the same manner that it was applied to the deceased spouse. The surviving spouse military retirement deduction is in addition to any retirement deductions claimed on the taxpayer’s own retirement income. If you are claiming the surviving spouse military retirement deduction for more than one deceased spouse, calculate the deduction separately for each deceased spouse. Add the surviving spouse military retirement deductions and enter the total on line p-6. Attach a statement showing the date of birth for each deceased spouse and the separate calculation for each deduction. Line q: Age 65 and older deduction Beginning in the tax year a resident taxpayer reaches age 65, they are entitled to a deduction of $15,000 against any South Carolina income. Line q-1 applies to the taxpayer whose name appears first on the return. Line q-2 applies to the spouse whose name appears second on the return� Reduce the age 65 and older deduction claimed on line q-1 and line q-2 by: ● any individual retirement deduction claimed on line p-1 and line p-2, and ● any military retirement deduction claimed on line p-4 and line p-5 Claiming a surviving spouse retirement deduction on line p-3 or line p-6 does not reduce the age 65 and older deduction for a taxpayer on line q-1 or line q-2. Worksheet for taxpayer (line q-1) 1. Age 65 and older deduction amount 1. $15,000 2. Retirement income deduction (line p-1) 2� 3. Military retirement income deduction (line p-4) 3� 4. Deduction available (add line 2 and line 3, then subtract the total from line 1. If less than zero, enter zero.) Enter on line q-1. 4� 10 SCDOR | SC1040 Instructions |

Enlarge image |

Worksheet for spouse (line q-2)

1. Age 65 and older deduction amount 1. $15,000

2. Retirement income deduction (line p-2) 2�

3. Military retirement income deduction (line p-5) 3�

4. Deduction available (add line 2 and line 3, then subtract the total from

line 1. If less than zero, enter zero.) Enter on line q-2. 4�

Assume for all examples that taxpayers have income to qualify for the age 65 and older deduction in

addition to the retirement deductions.

Example 1: A taxpayer age 65 or older has no military or other sourced retirement income on line p-1

or line p-4. The taxpayer is eligible for a deduction of $15,000 on line q-1.

Example 2: A taxpayer age 65 or older has no military retirement income but has other sourced

retirement of $14,000. The taxpayer is allowed a deduction of $10,000 on line p-1 and a deduction of

$5,000 on line q-1.

Example 3: A taxpayer age 65 or older has military retirement income of $13,000 and is allowed a

deduction on line p-4 of $13,000. The taxpayer is allowed a deduction of $2,000 on line q-1. The

maximum allowed deduction for 2023 is $15,000.

Example 4: A taxpayer age 65 or older has military retirement income of $36,000 and no other earned

income. The taxpayer is eligible for a military retirement deduction of $36,000 on line p-4. The taxpayer

is not allowed an additional amount on line q-1.

Example 5: A taxpayer age 65 or older has military retirement income of $16,000 and other sourced

retirement income of $8,000. The taxpayer is allowed a deduction on line p-4 of $16,000. The taxpayer

is not allowed an additional amount on line p-1 or line q-1.

For more information about retirement deductions and the age 65 and older deduction, refer to SC

Revenue Ruling #22-11, available at dor.sc.gov/policy�

Line r: Negative amount of federal taxable income

Because the South Carolina return begins with your federal taxable income, it is important that you get

the benefit of the negative amount from the taxable income line of the federal return. On the SC1040,

start with zero on line 1. Do not enter a negative amount. On line r of the SC1040, enter the negative

amount from the taxable income line of the federal return. Enter as a positive number.

Line s: Subsistence allowance

Police and all commissioned law enforcement officers paid by South Carolina municipal, county, or state

governments or the federal government, full-time firefighters, and full-time emergency medical service

personnel are entitled to a subsistence allowance of $8 per regular workday. Your employer should

provide you with the number of work days�

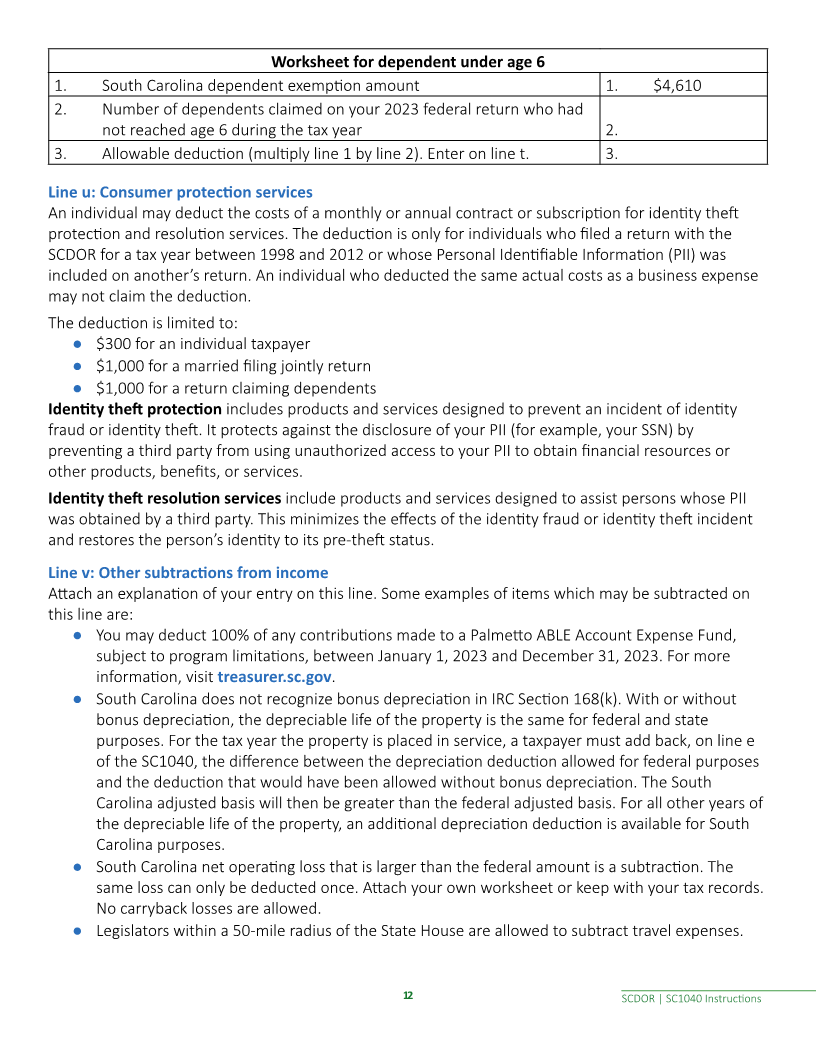

Line t: Dependents under 6 years of age

A deduction is allowed for each dependent claimed on your federal Income Tax return who had not

reached the age of 6 by December 31 of the tax year. Birth dates and SSNs are required. See worksheet

below�

11 SCDOR | SC1040 Instructions

|

Enlarge image |

Worksheet for dependent under age 6

1� South Carolina dependent exemption amount 1. $4,610

2� Number of dependents claimed on your 2023 federal return who had

not reached age 6 during the tax year 2�

3� Allowable deduction (multiply line 1 by line 2). Enter on line t. 3�

Line u: Consumer protection services

An individual may deduct the costs of a monthly or annual contract or subscription for identity theft

protection and resolution services. The deduction is only for individuals who filed a return with the

SCDOR for a tax year between 1998 and 2012 or whose Personal Identifiable Information (PII) was

included on another’s return� An individual who deducted the same actual costs as a business expense

may not claim the deduction.

The deduction is limited to:

● $300 for an individual taxpayer

● $1,000 for a married filing jointly return

● $1,000 for a return claiming dependents

Identity theft protection includes products and services designed to prevent an incident of identity

fraud or identity theft. It protects against the disclosure of your PII (for example, your SSN) by

preventing a third party from using unauthorized access to your PII to obtain financial resources or

other products, benefits, or services.

Identity theft resolution services include products and services designed to assist persons whose PII

was obtained by a third party. This minimizes the effects of the identity fraud or identity theft incident

and restores the person’s identity to its pre-theft status.

Line v: Other subtractions from income

Attach an explanation of your entry on this line. Some examples of items which may be subtracted on

this line are:

● You may deduct 100% of any contributions made to a Palmetto ABLE Account Expense Fund,

subject to program limitations, between January 1, 2023 and December 31, 2023. For more

information, visit treasurer.sc.gov�

● South Carolina does not recognize bonus depreciation in IRC Section 168(k). With or without

bonus depreciation, the depreciable life of the property is the same for federal and state

purposes. For the tax year the property is placed in service, a taxpayer must add back, on line e

of the SC1040, the difference between the depreciation deduction allowed for federal purposes

and the deduction that would have been allowed without bonus depreciation. The South

Carolina adjusted basis will then be greater than the federal adjusted basis. For all other years of

the depreciable life of the property, an additional depreciation deduction is available for South

Carolina purposes�

● South Carolina net operating loss that is larger than the federal amount is a subtraction. The

same loss can only be deducted once. Attach your own worksheet or keep with your tax records.

No carryback losses are allowed�

● Legislators within a 50-mile radius of the State House are allowed to subtract travel expenses.

12 SCDOR | SC1040 Instructions

|

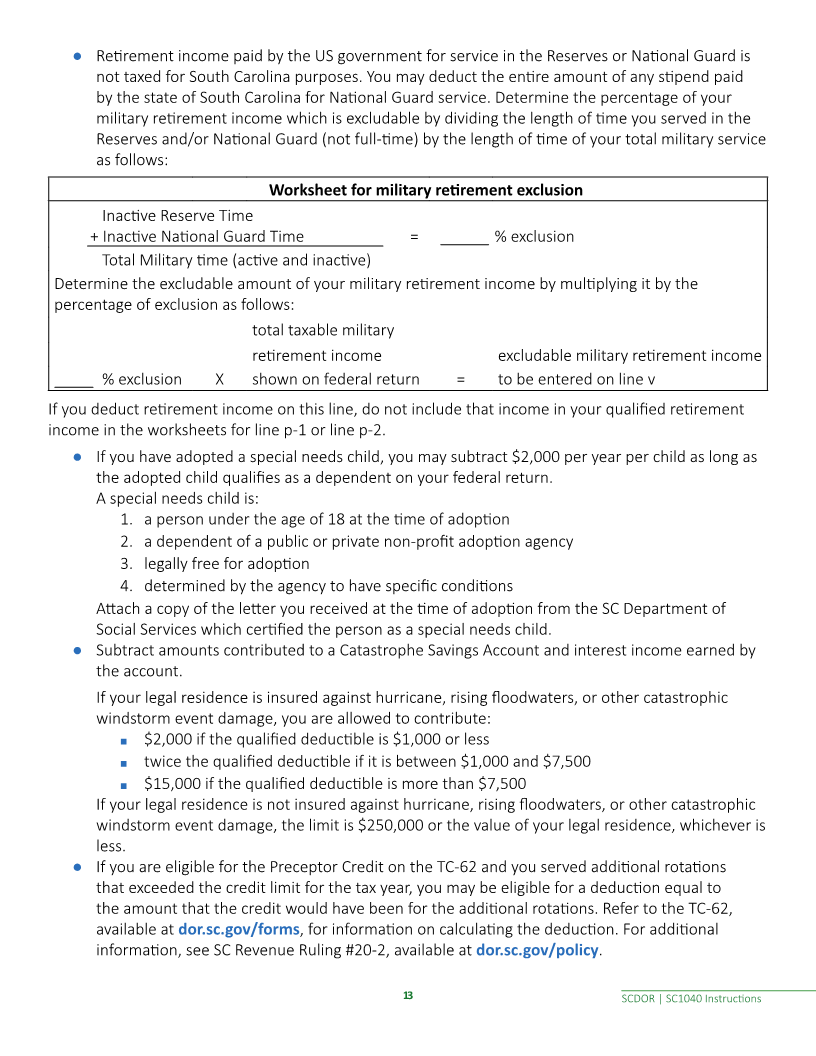

Enlarge image | ● Retirement income paid by the US government for service in the Reserves or National Guard is not taxed for South Carolina purposes. You may deduct the entire amount of any stipend paid by the state of South Carolina for National Guard service. Determine the percentage of your military retirement income which is excludable by dividing the length of time you served in the Reserves and/or National Guard (not full-time) by the length of time of your total military service as follows: Worksheet for military retirement exclusion Inactive Reserve Time + Inactive National Guard Time = % exclusion Total Military time (active and inactive) Determine the excludable amount of your military retirement income by multiplying it by the percentage of exclusion as follows: total taxable military retirement income excludable military retirement income % exclusion X shown on federal return = to be entered on line v If you deduct retirement income on this line, do not include that income in your qualified retirement income in the worksheets for line p-1 or line p-2. ● If you have adopted a special needs child, you may subtract $2,000 per year per child as long as the adopted child qualifies as a dependent on your federal return. A special needs child is: 1� a person under the age of 18 at the time of adoption 2� a dependent of a public or private non-profit adoption agency 3� legally free for adoption 4� determined by the agency to have specific conditions Attach a copy of the letter you received at the time of adoption from the SC Department of Social Services which certified the person as a special needs child. ● Subtract amounts contributed to a Catastrophe Savings Account and interest income earned by the account� If your legal residence is insured against hurricane, rising floodwaters, or other catastrophic windstorm event damage, you are allowed to contribute: ■ $2,000 if the qualified deductible is $1,000 or less ■ twice the qualified deductible if it is between $1,000 and $7,500 ■ $15,000 if the qualified deductible is more than $7,500 If your legal residence is not insured against hurricane, rising floodwaters, or other catastrophic windstorm event damage, the limit is $250,000 or the value of your legal residence, whichever is less� ● If you are eligible for the Preceptor Credit on the TC-62 and you served additional rotations that exceeded the credit limit for the tax year, you may be eligible for a deduction equal to the amount that the credit would have been for the additional rotations. Refer to the TC-62, available at dor.sc.gov/forms, for information on calculating the deduction. For additional information, see SC Revenue Ruling #20-2, available at dor.sc.gov/policy� 13 SCDOR | SC1040 Instructions |

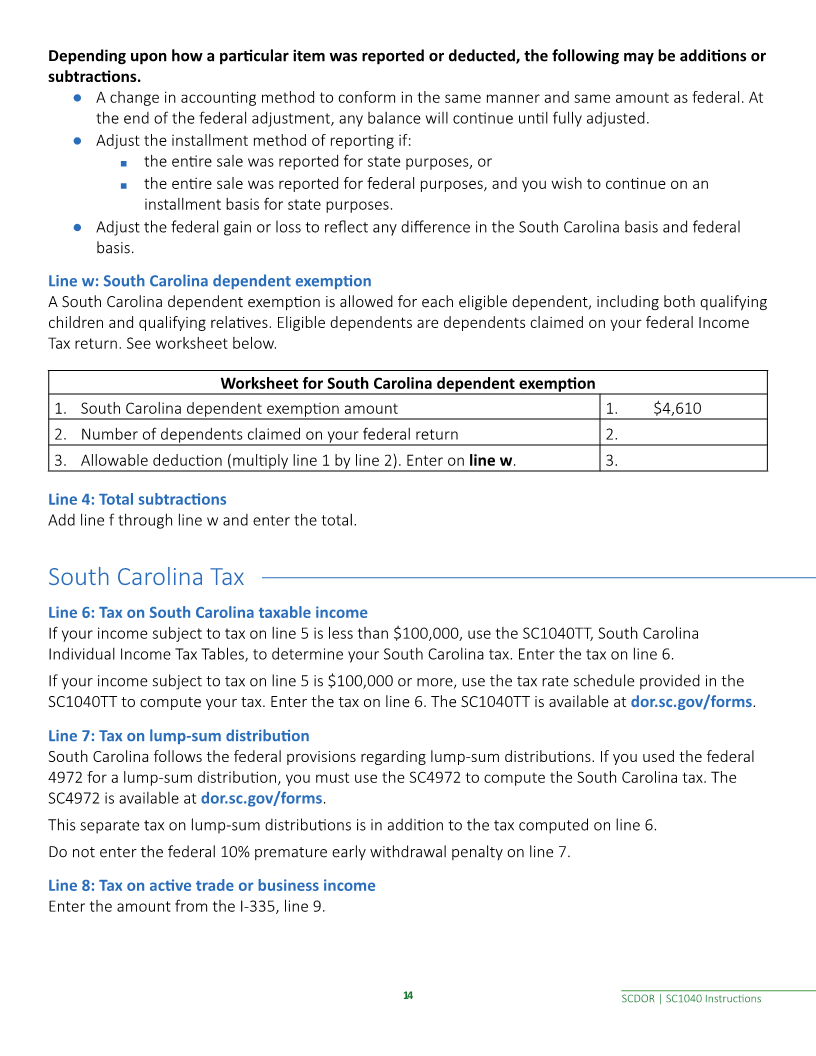

Enlarge image | Depending upon how a particular item was reported or deducted, the following may be additions or subtractions. ● A change in accounting method to conform in the same manner and same amount as federal. At the end of the federal adjustment, any balance will continue until fully adjusted. ● Adjust the installment method of reporting if: ■ the entire sale was reported for state purposes, or ■ the entire sale was reported for federal purposes, and you wish to continue on an installment basis for state purposes� ● Adjust the federal gain or loss to reflect any difference in the South Carolina basis and federal basis� Line w: South Carolina dependent exemption A South Carolina dependent exemption is allowed for each eligible dependent, including both qualifying children and qualifying relatives. Eligible dependents are dependents claimed on your federal Income Tax return. See worksheet below. Worksheet for South Carolina dependent exemption 1� South Carolina dependent exemption amount 1. $4,610 2� Number of dependents claimed on your federal return 2� 3� Allowable deduction (multiply line 1 by line 2). Enter on line w� 3� Line 4: Total subtractions Add line f through line w and enter the total� South Carolina Tax Line 6: Tax on South Carolina taxable income If your income subject to tax on line 5 is less than $100,000, use the SC1040TT, South Carolina Individual Income Tax Tables, to determine your South Carolina tax. Enter the tax on line 6. If your income subject to tax on line 5 is $100,000 or more, use the tax rate schedule provided in the SC1040TT to compute your tax. Enter the tax on line 6. The SC1040TT is available at dor.sc.gov/forms� Line 7: Tax on lump-sum distribution South Carolina follows the federal provisions regarding lump-sum distributions. If you used the federal 4972 for a lump-sum distribution, you must use the SC4972 to compute the South Carolina tax. The SC4972 is available at dor.sc.gov/forms� This separate tax on lump-sum distributions is in addition to the tax computed on line 6. Do not enter the federal 10% premature early withdrawal penalty on line 7� Line 8: Tax on active trade or business income Enter the amount from the I-335, line 9. 14 SCDOR | SC1040 Instructions |

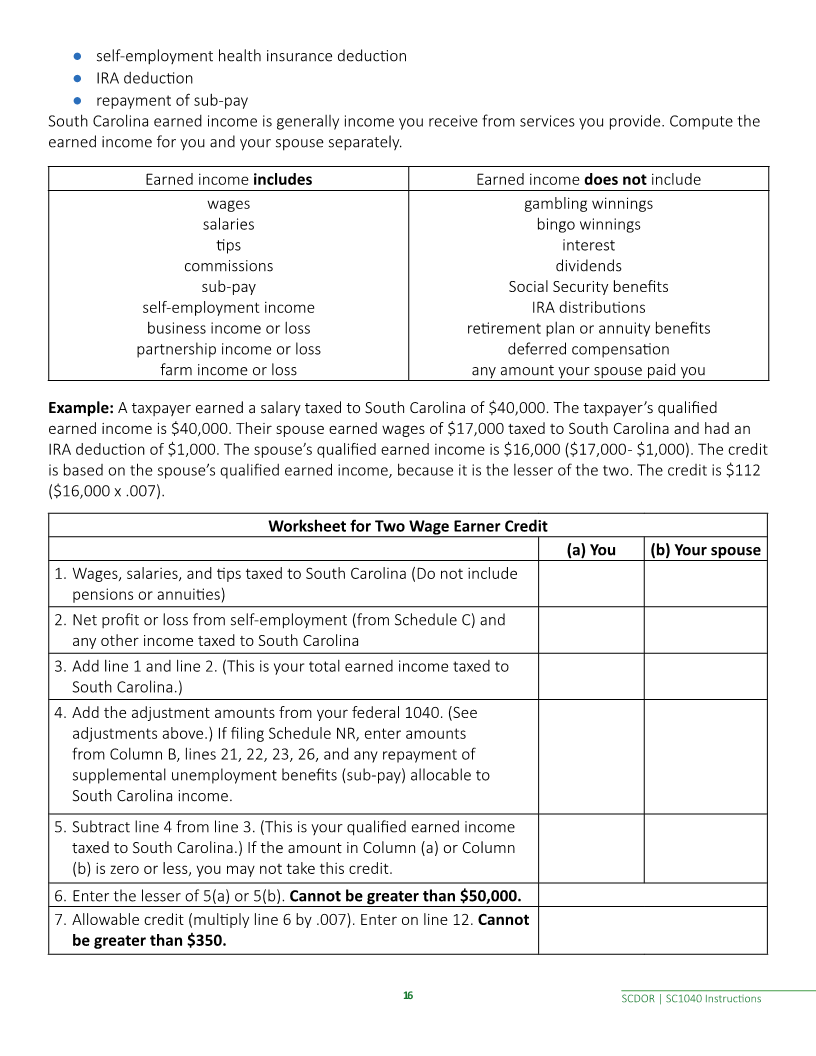

Enlarge image | Line 9: Tax on excess withdrawals from catastrophe savings accounts Excess withdrawals from a Catastrophe Savings Account are taxed an additional 2.5% unless: ● the taxpayer no longer owns a qualifying legal residence in South Carolina ● the amount contributed was within the allowable limits, and the withdrawal occurred after the taxpayer reached age 70, or ● the withdrawal followed the death of the individual who set up the account or the surviving spouse� Nonrefundable Credits Line 11: Child and Dependent Care Credit For a full-year resident, the credit is calculated at 7% of the federal child and dependent care expense. If you are a part-year resident or nonresident, you are not eligible for this credit if you are a resident of a state that does not offer a credit for child and dependent care expense to nonresidents of that state. If you are an eligible part-year resident or nonresident, calculate the credit at 7% of the prorated federal expenses using your proration percentage from the Schedule NR. The maximum credit allowed is $210 for one child or $420 for two or more children. You cannot claim this credit if your filing status is Married Filing Separately. Example A: Full-year resident Federal child care expense from the federal 2441 is $2,000 $2,000 x .07 = $140 (allowable credit) Example B: Part-year resident or nonresident Federal child care expense from the federal 2441 is $2,000, and the proration percent from line 45 of Schedule NR is 30%� $2,000 x .30 = $600 x .07 = $42 (allowable credit) Line 12: Two Wage Earner Credit This credit is available to a married couple filing jointly when both spouses have earned income taxed to South Carolina. This credit is not allowed on returns with a filing status of Single, Married Filing Separately, or Head of Household� The multiplier used in computing the Two Wage Earner Credit increases by $3,333 each year beginning in 2018, until fully phased-in for tax year 2023. For 2023, the credit is computed at .007 of the lesser of $50,000 or the South Carolina qualified earned income of the spouse with the lower South Carolina qualified earned income for the taxable year. Use your South Carolina qualified earned income to calculate the credit. Compute your South Carolina qualified earned income by subtracting certain adjustments reported on your federal 1040 from your South Carolina earned income� Adjustments to subtract are: ● deductible part of self-employment tax ● self-employment SEP, simple and qualified plans 15 SCDOR | SC1040 Instructions |

Enlarge image | ● self-employment health insurance deduction ● IRA deduction ● repayment of sub-pay South Carolina earned income is generally income you receive from services you provide� Compute the earned income for you and your spouse separately� Earned income includes Earned income does not include wages gambling winnings salaries bingo winnings tips interest commissions dividends sub-pay Social Security benefits self-employment income IRA distributions business income or loss retirement plan or annuity benefits partnership income or loss deferred compensation farm income or loss any amount your spouse paid you Example: A taxpayer earned a salary taxed to South Carolina of $40,000. The taxpayer’s qualified earned income is $40,000. Their spouse earned wages of $17,000 taxed to South Carolina and had an IRA deduction of $1,000. The spouse’s qualified earned income is $16,000 ($17,000 - $1,000). The credit is based on the spouse’s qualified earned income, because it is the lesser of the two. The credit is $112 ($16,000 x .007). Worksheet for Two Wage Earner Credit (a) You (b) Your spouse 1. Wages, salaries, and tips taxed to South Carolina (Do not include pensions or annuities) 2. Net profit or loss from self-employment (from Schedule C) and any other income taxed to South Carolina 3. Add line 1 and line 2. (This is your total earned income taxed to South Carolina�) 4. Add the adjustment amounts from your federal 1040. (See adjustments above.) If filing Schedule NR, enter amounts from Column B, lines 21, 22, 23, 26, and any repayment of supplemental unemployment benefits (sub-pay) allocable to South Carolina income� 5. Subtract line 4 from line 3. (This is your qualified earned income taxed to South Carolina�) If the amount in Column (a) or Column (b) is zero or less, you may not take this credit� 6� Enter the lesser of 5(a) or 5(b)� Cannot be greater than $50,000. 7. Allowable credit (multiply line 6 by .007). Enter on line 12. Cannot be greater than $350. 16 SCDOR | SC1040 Instructions |

Enlarge image | Line 13: Other nonrefundable credits Refer to the instructions for the SC1040TC for descriptions of the nonrefundable tax credits along with the required tax credit schedule for each credit. Most tax credits are computed on separate tax credit schedules� Attach tax credit schedules for all tax credits you claim, along with the SC1040TC Worksheet and the SC1040TC, to your Income Tax return. We may disallow your tax credits if you do not attach necessary schedules to your return. Forms are available at dor.sc.gov/forms� Tax Payments and Refundable Credits Line 16: South Carolina Income Tax withheld from wages Enter the total South Carolina tax withheld: ● from your wages and reported on your W-2s as state Income Tax, and ● by a fiduciary on your behalf and reported on your SC41s Do not include: ● withholding paid to another state ● federal withholding paid to the IRS ● withholding from a federal 1099 ● amounts reported on a South Carolina substitute 1099G/INT Attach readable copies of your W-2s to the front of your return. If filing an amended return, you must enter your South Carolina Income Tax withheld from wages on line 16 of your SC1040 and on line 1 of your SCH AMD� Your employer is responsible for providing you with a W-2. If you do not have a W-2, complete the SC4852 and provide proof of tax withheld. The SC4852 is available at dor.sc.gov/forms� Line 17: 2023 Estimated Tax payments Enter the total Estimated Tax payments you made, including any amount transferred from your 2022 tax return. Do not include nonresident sale of real estate withholding paid on an I-290. Report it on line 19. Line 18: Amount paid with extension Enter the amount you paid with your extension request. Check the box on the front of the return to indicate you requested an extension of time to file your return. Line 19: Nonresident sale of real estate A nonresident of South Carolina who sells real property located in this state is subject to withholding of South Carolina Income Tax. The sale is reported to South Carolina on an Individual Income Tax return. The state Income Tax withheld at the time of the sale is reported to you on an I-290 provided by the closing attorney. Enter the withholding from the I-290 and attach the form to your return. 17 SCDOR | SC1040 Instructions |

Enlarge image | Line 20: Other SC withholding Enter the total South Carolina tax withheld from federal 1099s. Attach copies of all 1099s to the front of your return� Do not include: ● withholding from a W-2 ● amounts reported on a South Carolina substitute 1099G/INT ● federal withholding paid to the IRS If filing an amended return, you must enter your Other SC withholding on line 20 of your SC1040 and on line 1 of your SCH AMD� Line 21: Tuition tax credit Refer to the I-319, available at dor.sc.gov/forms, to see if you qualify to claim this credit. If you qualify, complete all information on the I-319 and attach it to your return. If you have more than one qualifying student, complete a separate I-319 for each student. Attach a copy of your federal return. Line 22: Other refundable credits Refer to the I-333, I-334, I-360, and I-361, available at dor.sc.gov/forms, to see if you qualify to claim the credit. Attach the appropriate credit form to the SC1040. ● Enter the amount from the I-333, refundable credit for Anhydrous Ammonia Additive on line 22a� ● Enter the amount from the I-334, refundable credit for Production and Sale of Milk on line 22b. ● Enter the amount from the I-360, refundable credit for Classroom Teacher Expenses on line 22c. ● Enter the amount from the I-361, Parental Refundable Credit on line 22d. ● Enter the total other refundable credits on line 22� Line 23: Total payments Add line 16 through line 22 and enter the total� Amended return: Enter the amount from line 24 on line 30� (Do not enter amounts on line 26 through line 29.) Example 1 (amended return) Line 15 = 200 Line 23 = 250 (calculated on SCH AMD) Line 24 = 50 (250 - 200) Enter the $50 refund amount on line 30. 18 SCDOR | SC1040 Instructions |

Enlarge image | Line 25: Amount due If line 15 is larger than line 23, subtract line 23 from line 15 and enter the amount due� Amended return: Enter the amount from line 25 on line 31. (Do not enter amounts on line 26 through line 29.) Example 1 (amended return) Line 15 = 200 Line 23 = <125> (negative number, calculated on SCH AMD) Line 25 = 325 (200 - <125>) Enter the $325 tax due amount on line 31. Example 2 (amended return) Line 15 = 200 Line 23 = 125 (positive number, calculated on SCH AMD) Line 25 = 75 (200 - 125) Enter the $75 tax due amount on line 31. Line 26: South Carolina Use Tax Use Tax is due on purchases outside of South Carolina for use, storage, or consumption in South Carolina. Use Tax is paid to the SCDOR when state Sales and Use Tax has not been collected by the seller� You may need to pay Use Tax if you make purchases: ● from retailers online ● from out-of-state catalog companies ● from home shopping networks ● when visiting another state The tax rate for the Use Tax is the same as the Sales Tax. The rate is determined by where the tangible personal property will be used, stored, or consumed, regardless of where the sale takes place. For more information and updated tax rates, visit dor.sc.gov/tax/use� You have three options for reporting and paying Use Tax: 1� On line 26 of your SC1040, Individual Income Tax Return. Calculate your Use Tax using the SC Use Tax Worksheet below. No additional form or paperwork is required. 2� Online using our free, secure tax portal, MyDORWAY, at MyDORWAY.dor.sc.gov� Sign in to your existing account or create a new account to get started. No additional form or paperwork is required. 3� Mail the UT-3 with your check to: SCDOR, Sales Taxable, PO Box 100193, Columbia, SC 29202� Make your check payable to SCDOR. Include your name, SSN, and UT-3 in the memo. Do not send cash� If you have paid your Use Tax during the year or have no Use Tax due, check the box on line 26. Use Tax rates The state Sales and Use Tax rate is 6% plus the applicable local Use Tax rate of the county in which you are located or other applicable rate wherever tangible personal property was delivered� Sales of unprepared food are exempt from state Sales and Use Tax. Local taxes still apply to sales of unprepared food unless the local tax law exempts such sales� 19 SCDOR | SC1040 Instructions |

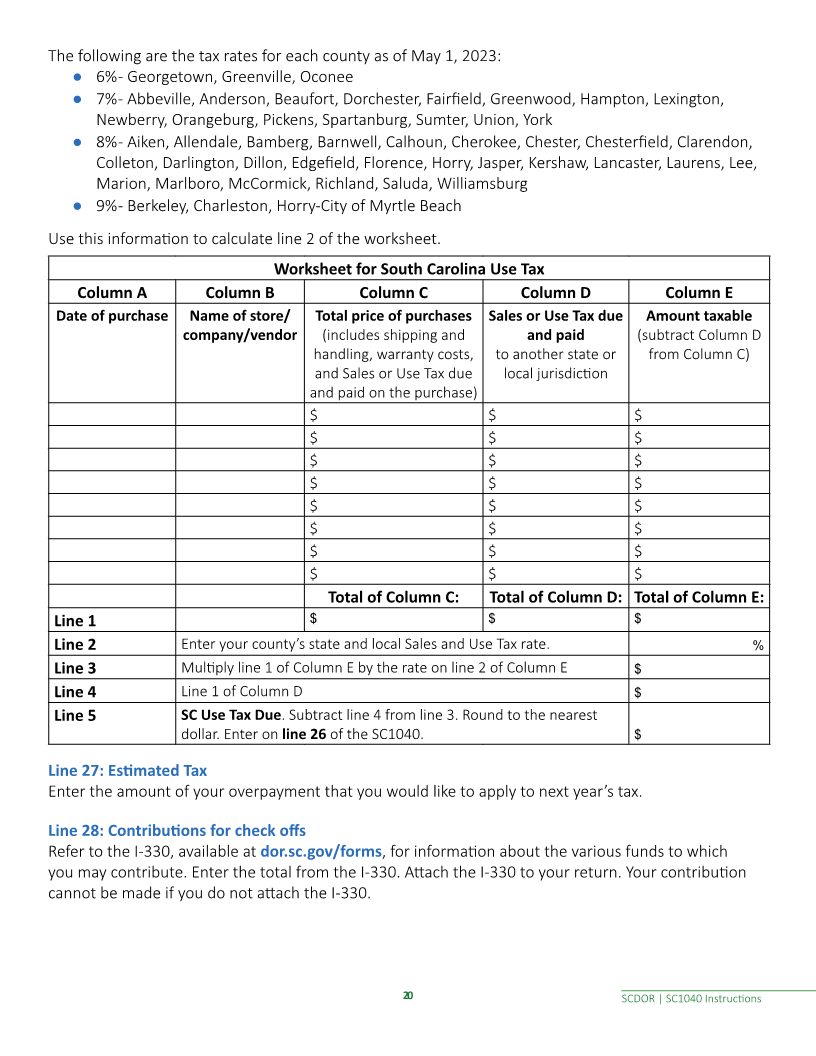

Enlarge image | The following are the tax rates for each county as of May 1, 2023: ● 6% - Georgetown, Greenville, Oconee ● 7% - Abbeville, Anderson, Beaufort, Dorchester, Fairfield, Greenwood, Hampton, Lexington, Newberry, Orangeburg, Pickens, Spartanburg, Sumter, Union, York ● 8% - Aiken, Allendale, Bamberg, Barnwell, Calhoun, Cherokee, Chester, Chesterfield, Clarendon, Colleton, Darlington, Dillon, Edgefield, Florence, Horry, Jasper, Kershaw, Lancaster, Laurens, Lee, Marion, Marlboro, McCormick, Richland, Saluda, Williamsburg ● 9% - Berkeley, Charleston, Horry-City of Myrtle Beach Use this information to calculate line 2 of the worksheet. Worksheet for South Carolina Use Tax Column A Column B Column C Column D Column E Date of purchase Name of store/ Total price of purchases Sales or Use Tax due Amount taxable company/vendor (includes shipping and and paid (subtract Column D handling, warranty costs, to another state or from Column C) and Sales or Use Tax due local jurisdiction and paid on the purchase) $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ Total of Column C: Total of Column D: Total of Column E: Line 1 $ $ $ Line 2 Enter your county’s state and local Sales and Use Tax rate. % Line 3 Multiply line 1 of Column E by the rate on line 2 of Column E $ Line 4 Line 1 of Column D $ Line 5 SC Use Tax Due� Subtract line 4 from line 3� Round to the nearest dollar� Enter on line 26 of the SC1040� $ Line 27: Estimated Tax Enter the amount of your overpayment that you would like to apply to next year’s tax� Line 28: Contributions for check offs Refer to the I-330, available at dor.sc.gov/forms, for information about the various funds to which you may contribute. Enter the total from the I-330. Attach the I-330 to your return. Your contribution cannot be made if you do not attach the I-330. 20 SCDOR | SC1040 Instructions |

Enlarge image | Refund or Amount You Owe Line 30: Refund If line 29 is larger than line 24, go to line 31. Otherwise, subtract line 29 from line 24 and enter the amount to be refunded to you on line 30. We will not automatically issue a refund under $5. However, upon notification, we can release the refund. You are required to mark your refund choice on line 35. Line 31: Net tax Add line 25 and line 29. Line 32: Late filing and late payment penalties and interest If you calculated failure to file or failure to pay penalties and interest, enter in the appropriate blanks and put the total of both on line 32� A failure to file penalty is charged for failing to file a tax return on or before its due date, considering any extension of time for filing. The penalty is 5% of the tax amount if the failure is for not more than one month, with an additional 5% for each additional month or fraction of a month the failure continues, not to exceed 25% in total. A failure to pay penalty is charged for failing to pay the tax on any return on or before its due date. The penalty is 0.5% of the tax if the failure is for not more than one month, with an additional 0.5% for each additional month or fraction of a month the failure continues, not to exceed 25% in total. Any unpaid portion of the final tax due will accrue interest at the prevailing federal rates. This amount is computed from the original due date of the tax return to the date of the payment� Find a Penalty and Interest Calculator on our free online tax portal, MyDORWAY, at dor.sc.gov/calculator� Line 33: Underpayment of Estimated Tax penalty You may owe a penalty for underpayment if you did not pay in the lesser of 90% of your tax liability for 2023 or 100% of your liability for 2022 in four equal amounts by the required dates. If your adjusted gross income is $150,000 or more, the 100% rule is modified to be 110% of the tax shown on your 2022 Income Tax return. Refer to the SC2210, available at dor.sc.gov/forms, to calculate any penalty that may be due� Exceptions to the underpayment of Estimated Tax: ● Enter an A in the box if you completed federal Schedule AI-Annualized Income Installment Method for South Carolina purposes when determining the amount to enter on line 33� ● Enter an F in the box if you are a farmer or fisherman who receives at least two-thirds of your gross income for the year from farming and fishing and you pay your tax due by March 1, 2024. ● Enter a W if you are requesting a waiver of your penalty for any other reason. See the SC2210 instructions, available at dor.sc.gov/forms, for information on what qualifies for a waiver of penalty� Calculate your penalty for underpayment and enter the amount on line 33� If you are due a refund, subtract the penalty amount from the difference of line 24 and line 29 and enter the result on line 30. Attach the SC2210 to your tax return when using an exception to waive the penalty. 21 SCDOR | SC1040 Instructions |

Enlarge image | Line 34: Balance due Add line 31 through line 33 and enter the total on line 34. This is the amount you owe. If you owe $15,000 or more in connection with any SCDOR return, you must pay electronically according to SC Code Sections 12-54-250 and 12-54-210. Line 35: Refund options (select one). Direct deposit is fast and safe! You can receive your refund by direct deposit or paper check� Mark an Xin one box to indicate your choice� ● Direct deposit - The SCDOR deposits your funds into your bank account. This is the fastest, easiest option for most filers. Enter your bank information on line 37. ● Paper check - The SCDOR can mail you a paper check to the address provided on your return. To avoid delays, make sure the address on your return is correct. This is the slowest, least secure way to receive your funds� Line 36: Payment options (select one). Paying electronically is quick and easy! You can pay your balance using our free online tax portal, MyDORWAY, or by using ACH Debit� Mark an X in one box to indicate your choice� ● MyDORWAY - The quickest, easiest way to pay is using our free online tax portal, MyDORWAY, at dor.sc.gov/pay� Select Individual Income Tax Payment to get started. Choose the 31-Dec-2023 filing period. ● ACH Debit - Pay electronically by ACH Debit when you file your return. Enter your payment withdrawal date and payment withdrawal amount on line 36. Enter your bank information on line 37. The SCDOR will make a request to your bank for payment of the South Carolina taxes you owe. Your bank will automatically debit your account for the requested funds. No further action is needed on your part! Line 37: Bank information You must enter complete and correct account information. If you are requesting direct deposit of your refund and your account information is not complete and correct, we will mail a paper check to the address listed on your return� If you are making a payment by ACH Debit, the withdrawal of the funds will not be successful if your account information is not complete and correct. You cannot have your funds directly deposited into an account located outside the United States or an ACH Debit withdrawn from an account located outside the United States� Enter your account information. 1� Mark an Xto choose checking or savings account� 2� Enter your 9 digit routing transit number (RTN). The RTN should begin with 01 through 12 or 21 through 32. Do not use a deposit slip to verify the RTN. 3� Enter your bank account number (BAN). The BAN contains 17 or fewer alphanumeric digits. Enter the BAN from left to right. Do not enter hyphens, spaces, special symbols, or the check number� 22 SCDOR | SC1040 Instructions |

Enlarge image | Sign and date your return You must sign your return. If your filing status is Married Filing Jointly, both spouses must sign. The return for a deceased taxpayer must be signed by a surviving spouse, an executor, or an administrator� If you are signing as a surviving spouse, write filing as surviving spouse by your signature� If signing as a personal representative, sign in your official capacity and attach a completed SC1310, Statement of Person Claiming Refund Due a Deceased Taxpayer, available at dor.sc.gov/forms� Any refund check will be issued to the decedent’s surviving spouse or estate� Authorization The signature section of the return contains a check the box authorization for release of confidential information. A check in the yes box authorizes the Director of the SCDOR or delegate to discuss the return; its attachments; and any notices, adjustments, or assessments with the preparer. If a person is paid to prepare the Income Tax return, their signature and Preparer Tax Identification Number (PTIN) or Federal Employer Identification Number (FEIN) are required in the spaces provided. Penalties are applicable for failure to comply. Important Reminders Filing online is faster and more accurate. ● You may qualify to file online or submit your return electronically for free. Even if you don’t qualify for free filing options, we recommend you file electronically - It’s our fastest, easiest, and safest option. Visit dor.sc.gov/iit-filing to learn more about your options. Getting a refund? Direct deposit is fast, accurate, and secure! ● With direct deposit, you: ■ get your refund deposited directly into your bank account, giving you the fastest access to your refund� ■ help save tax dollars� ■ get your refund sooner� Have a balance due? Pay electronically! It’s fast and easy! ● Paying online is quick and easy! Use our free and secure tax portal, MyDORWAY, at dor.sc.gov/pay to make your payment� Select Individual Income Tax Payment to get started� Choose the 31-Dec-2023 filing period. ● On MyDORWAY, you can pay by credit card or from your bank account� ● Pay electronically by ACH Debit when you file your return. Enter your bank information on line 37� ■ The SCDOR will make a request to your bank for payment of the South Carolina taxes you owe� ■ Your bank will automatically debit your account for the requested funds. No further action is needed on your part! 23 SCDOR | SC1040 Instructions |

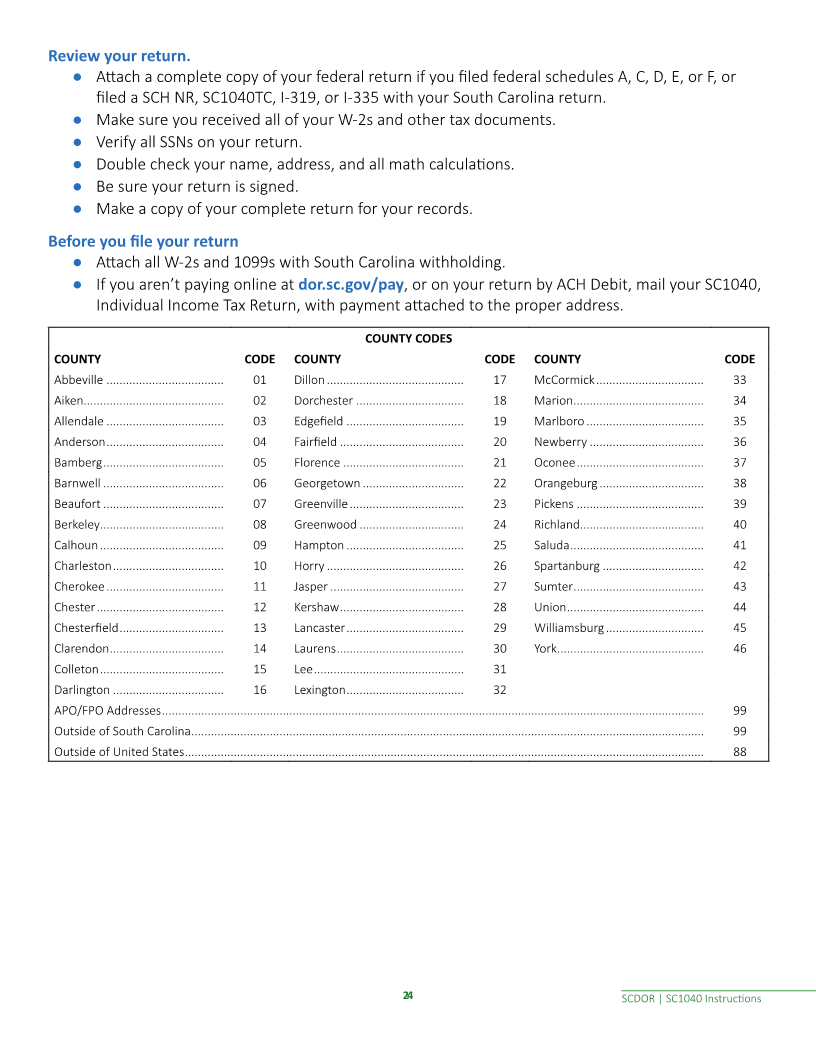

Enlarge image | Review your return. ● Attach a complete copy of your federal return if you filed federal schedules A, C, D, E, or F, or filed a SCH NR, SC1040TC, I-319, or I-335 with your South Carolina return. ● Make sure you received all of your W-2s and other tax documents. ● Verify all SSNs on your return. ● Double check your name, address, and all math calculations. ● Be sure your return is signed� ● Make a copy of your complete return for your records� Before you file your return ● Attach all W-2s and 1099s with South Carolina withholding. ● If you aren’t paying online at dor.sc.gov/pay, or on your return by ACH Debit, mail your SC1040, Individual Income Tax Return, with payment attached to the proper address. COUNTY CODES COUNTY CODE COUNTY CODE COUNTY CODE Abbeville ������������������������������������ 01 Dillon ������������������������������������������ 17 McCormick ��������������������������������� 33 Aiken������������������������������������������� 02 Dorchester ��������������������������������� 18 Marion ���������������������������������������� 34 Allendale ������������������������������������ 03 Edgefield ������������������������������������ 19 Marlboro ������������������������������������ 35 Anderson ������������������������������������ 04 Fairfield �������������������������������������� 20 Newberry ����������������������������������� 36 Bamberg ������������������������������������� 05 Florence ������������������������������������� 21 Oconee ��������������������������������������� 37 Barnwell ������������������������������������� 06 Georgetown ������������������������������� 22 Orangeburg �������������������������������� 38 Beaufort ������������������������������������� 07 Greenville ����������������������������������� 23 Pickens ��������������������������������������� 39 Berkeley�������������������������������������� 08 Greenwood �������������������������������� 24 Richland�������������������������������������� 40 Calhoun �������������������������������������� 09 Hampton ������������������������������������ 25 Saluda ����������������������������������������� 41 Charleston ���������������������������������� 10 Horry ������������������������������������������ 26 Spartanburg ������������������������������� 42 Cherokee ������������������������������������ 11 Jasper ����������������������������������������� 27 Sumter ���������������������������������������� 43 Chester ��������������������������������������� 12 Kershaw �������������������������������������� 28 Union ������������������������������������������ 44 Chesterfield �������������������������������� 13 Lancaster ������������������������������������ 29 Williamsburg ������������������������������ 45 Clarendon ����������������������������������� 14 Laurens ��������������������������������������� 30 York ��������������������������������������������� 46 Colleton �������������������������������������� 15 Lee ���������������������������������������������� 31 Darlington ���������������������������������� 16 Lexington ������������������������������������ 32 APO/FPO Addresses ���������������������������������������������������������������������������������������������������������������������������������������������������������������������� 99 Outside of South Carolina ������������������������������������������������������������������������������������������������������������������������������������������������������������� 99 Outside of United States ��������������������������������������������������������������������������������������������������������������������������������������������������������������� 88 24 SCDOR | SC1040 Instructions |