Enlarge image

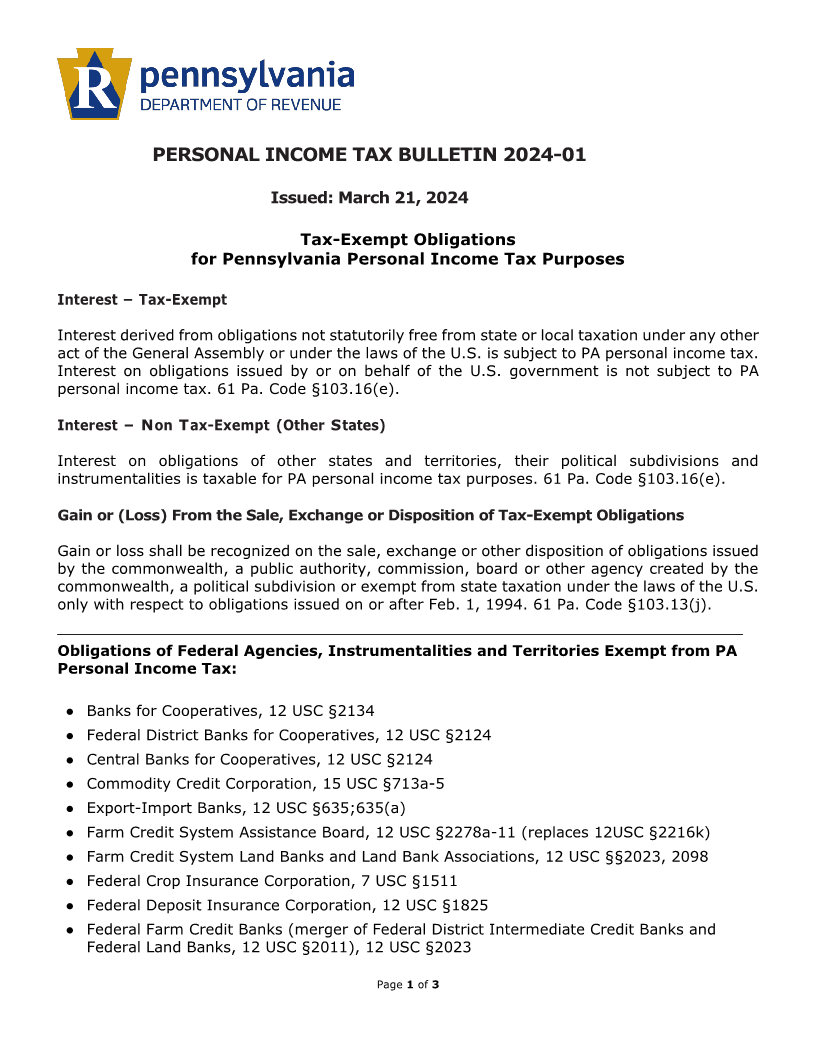

PERSONAL INCOME TAX BULLETIN 2024-01

Issued: March 21, 2024

Tax-Exempt Obligations

for Pennsylvania Personal Income Tax Purposes

Interest – Tax-Exempt

Interest derived from obligations not statutorily free from state or local taxation under any other

act of the General Assembly or under the laws of the U.S. is subject to PA personal income tax.

Interest on obligations issued by or on behalf of the U.S. government is not subject to PA

personal income tax. 61 Pa. Code §103.16(e).

Interest N– on Tax-Exempt (Other States)

Interest on obligations of other states and territories, their political subdivisions and

instrumentalities is taxable for PA personal income tax purposes. 61 Pa. Code §103.16(e).

Gain or (Loss) From the Sale, Exchange or Disposition of Tax-Exempt Obligations

Gain or loss shall be recognized on the sale, exchange or other disposition of obligations issued

by the commonwealth, a public authority, commission, board or other agency created by the

commonwealth, a political subdivision or exempt from state taxation under the laws of the U.S.

only with respect to obligations issued on or after Feb. 1, 1994. 61 Pa. Code §103.13(j).

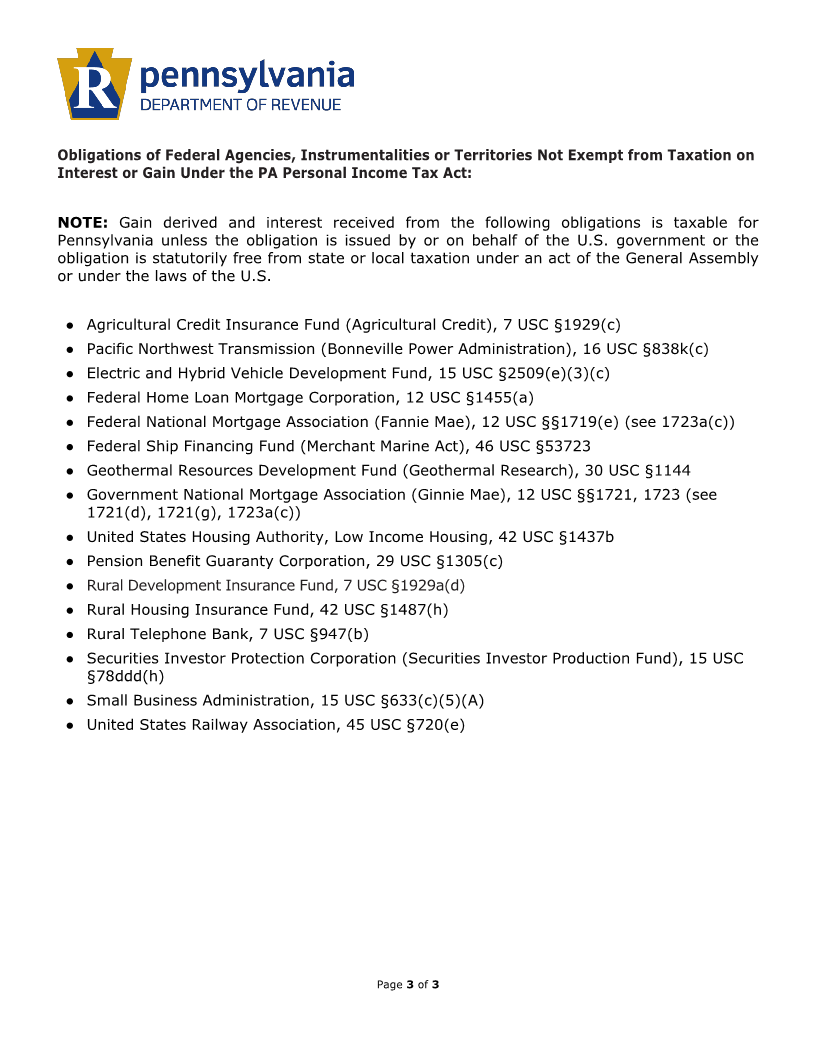

Obligations of Federal Agencies, Instrumentalities and Territories Exempt from PA

Personal Income Tax:

● Banks for Cooperatives, 12 USC §2134

● Federal District Banks for Cooperatives, 12 USC §2124

● Central Banks for Cooperatives, 12 USC §2124

● Commodity Credit Corporation, 15 USC §713a-5

● Export-Import Banks, 12 USC §635;635(a)

● Farm Credit System Assistance Board, 12 USC §2278a-11 (replaces 12USC §2216k)

● Farm Credit System Land Banks and Land Bank Associations, 12 USC §§2023, 2098

● Federal Crop Insurance Corporation, 7 USC §1511

● Federal Deposit Insurance Corporation, 12 USC §1825

● Federal Farm Credit Banks (merger of Federal District Intermediate Credit Banks and

Federal Land Banks, 12 USC §2011), 12 USC §2023

Page 1of 3