Enlarge image

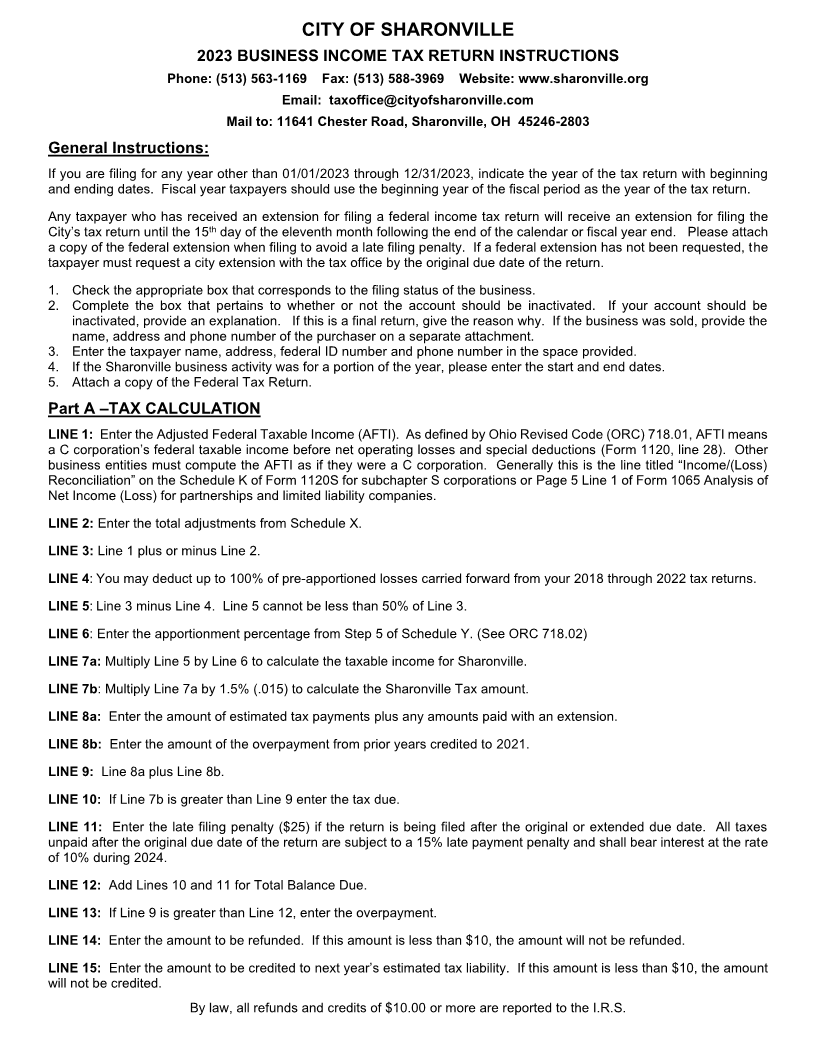

CITY OF SHARONVILLE

2023 BUSINESS INCOME TAX RETURN INSTRUCTIONS

Phone: (513) 563-1169 Fax: (513) 588-3969 Website: www.sharonville.org

Email: taxoffice@cityofsharonville.com

Mail to: 11641 Chester Road, Sharonville, OH 45246-2803

General Instructions:

If you are filing for any year other than 01/01/2023 through 12/31/2023, indicate the year of the tax return with beginning

and ending dates. Fiscal year taxpayers should use the beginning year of the fiscal period as the year of the tax return.

Any taxpayer who has received an extension for filing a federal income tax return will receive an extension for filing the

tax return until the 15 day of the eleventh month following the end of the calendar or fiscal year end. Please attach City’s th

a copy of the federal extension when filing to avoid a late filing penalty. If a federal extension has not been requested, the

taxpayer must request a city extension with the tax office by the original due date of the return.

1. Check the appropriate box that corresponds to the filing status of the business.

2. Complete the box that pertains to whether or not the account should be inactivated. If your account should be

inactivated, provide an explanation. If this is a final return, give the reason why. If the business was sold, provide the

name, address and phone number of the purchaser on a separate attachment.

3. Enter the taxpayer name, address, federal ID number and phone number in the space provided.

4. If the Sharonville business activity was for a portion of the year, please enter the start and end dates.

5. Attach a copy of the Federal Tax Return.

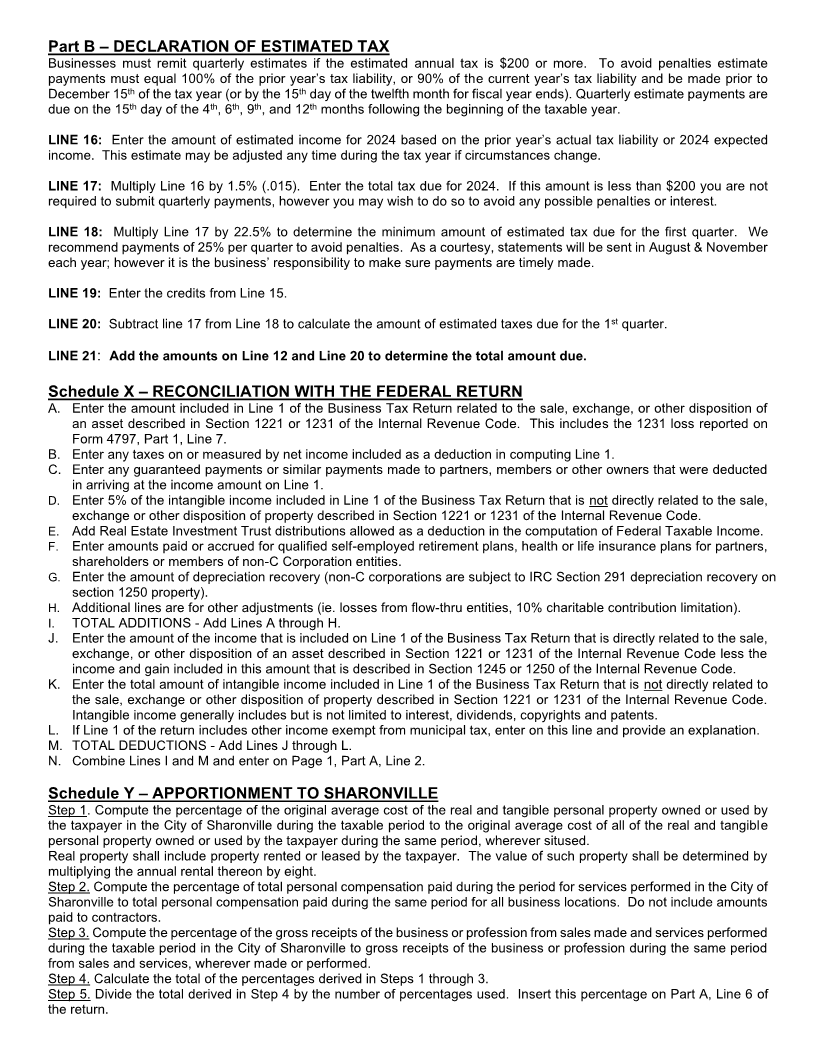

Part A –TAX CALCULATION

LINE 1: Enter the Adjusted Federal Taxable Income (AFTI). As defined by Ohio Revised Code (ORC) 718.01, AFTI means

a C corporation’s federal taxable income before net operating losses and special deductions (Form 1120, line 28). Other

business entities must compute the AFTI as if they were a C corporation. Generally this is the line titled “Income/(Loss)

Reconciliation” on the Schedule K of Form 1120S for subchapter S corporations or Page 5 Line 1 of Form 1065 Analysis of

Net Income (Loss) for partnerships and limited liability companies.

LINE 2: Enter the total adjustments from Schedule X.

LINE 3: Line 1 plus or minus Line 2.

LINE 4: You may deduct up to 100% of pre-apportioned losses carried forward from your 2018 through 2022 tax returns.

LINE 5: Line 3 minus Line 4. Line 5 cannot be less than 50% of Line 3.

LINE 6: Enter the apportionment percentage from Step 5 of Schedule Y. (See ORC 718.02)

LINE 7a: Multiply Line 5 by Line 6 to calculate the taxable income for Sharonville.

LINE 7b: Multiply Line 7a by 1.5% (.015) to calculate the Sharonville Tax amount.

LINE 8a: Enter the amount of estimated tax payments plus any amounts paid with an extension.

LINE 8b: Enter the amount of the overpayment from prior years credited to 2021.

LINE 9: Line 8a plus Line 8b.

LINE 10: If Line 7b is greater than Line 9 enter the tax due.

LINE 11: Enter the late filing penalty ($25) if the return is being filed after the original or extended due date. All taxes

unpaid after the original due date of the return are subject to a 15% late payment penalty and shall bear interest at the rate

of 10% during 2024.

LINE 12: Add Lines 10 and 11 for Total Balance Due.

LINE 13: If Line 9 is greater than Line 12, enter the overpayment.

LINE 14: Enter the amount to be refunded. If this amount is less than $10, the amount will not be refunded.

LINE 15: Enter the amount to be credited to next year’s estimated tax liability. If this amount is less than $10, the amount

will not be credited.

By law, all refunds and credits of $10.00 or more are reported to the I.R.S.