Enlarge image

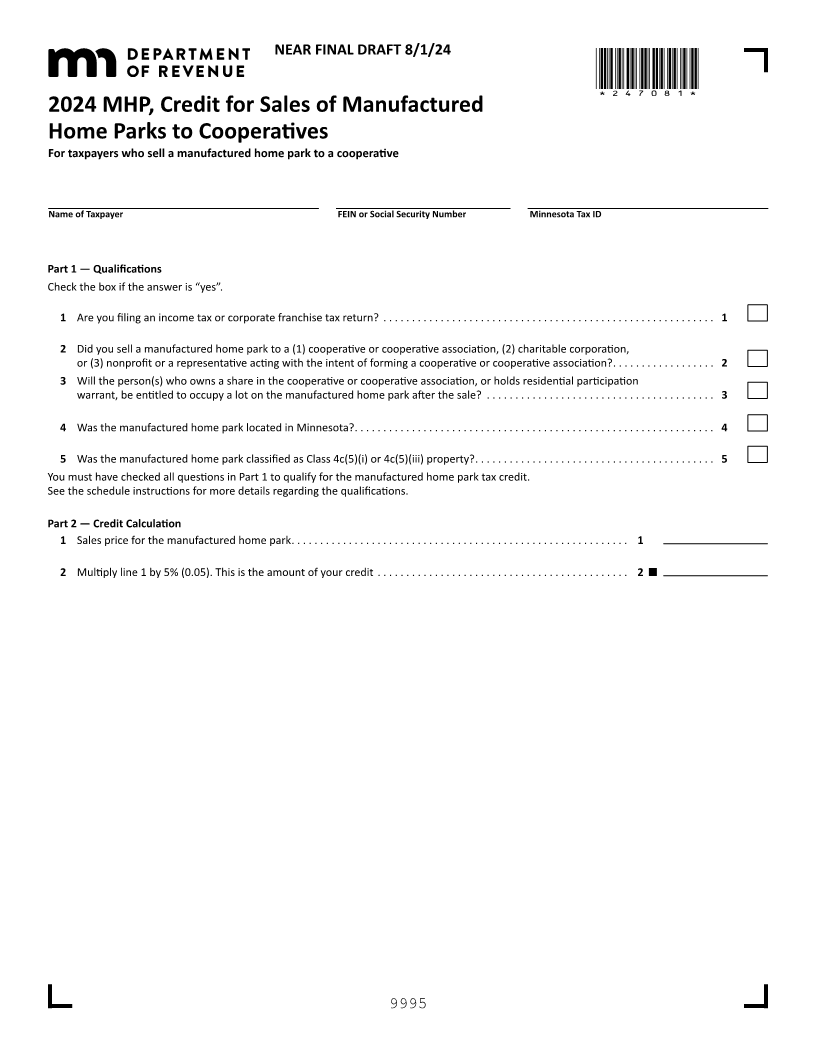

NEAR FINAL DRAFT 8/1/24

*247081*

2024 MHP, Credit for Sales of Manufactured

Home Parks to Cooperatives

For taxpayers who sell a manufactured home park to a cooperative

Name of Taxpayer FEIN or Social Security Number Minnesota Tax ID

Part 1 — Qualifications

Check the box if the answer is “yes”.

1 Are you filing an income tax or corporate franchise tax return? ..... ...... ...... ..... ...... ..... ....... ..... ..... ....... . 1

2 Did you sell a manufactured home park to a (1) cooperative or cooperative association, (2) charitable corporation,

or (3) nonprofit or a representative acting with the intent of forming a cooperative or cooperative association?... ...... ...... ... 2

3 Will the person(s) who owns a share in the cooperative or cooperative association, or holds residential participation

warrant, be entitled to occupy a lot on the manufactured home park after the sale? ..... ....... .... ...... ...... ...... ...... 3

4 Was the manufactured home park located in Minnesota?... ...... ..... ....... ..... ..... ...... ..... ...... ...... ...... ... 4

5 Was the manufactured home park classified as Class 4c(5)(i) or 4c(5)(iii) property? ... ...... ..... ....... ..... ...... ..... ..... 5

You must have checked all questions in Part 1 to qualify for the manufactured home park tax credit.

See the schedule instructions for more details regarding the qualifications.

Part 2 — Credit Calculation

1 Sales price for the manufactured home park... ...... ..... ....... ..... ...... ..... ..... ...... ...... ..... 1

2 Multiply line 1 by 5% (0.05). This is the amount of your credit ..... ...... ..... ...... ..... ....... ...... .... 2

9995