Enlarge image

NEAR FINAL DRAFT 8/1/24

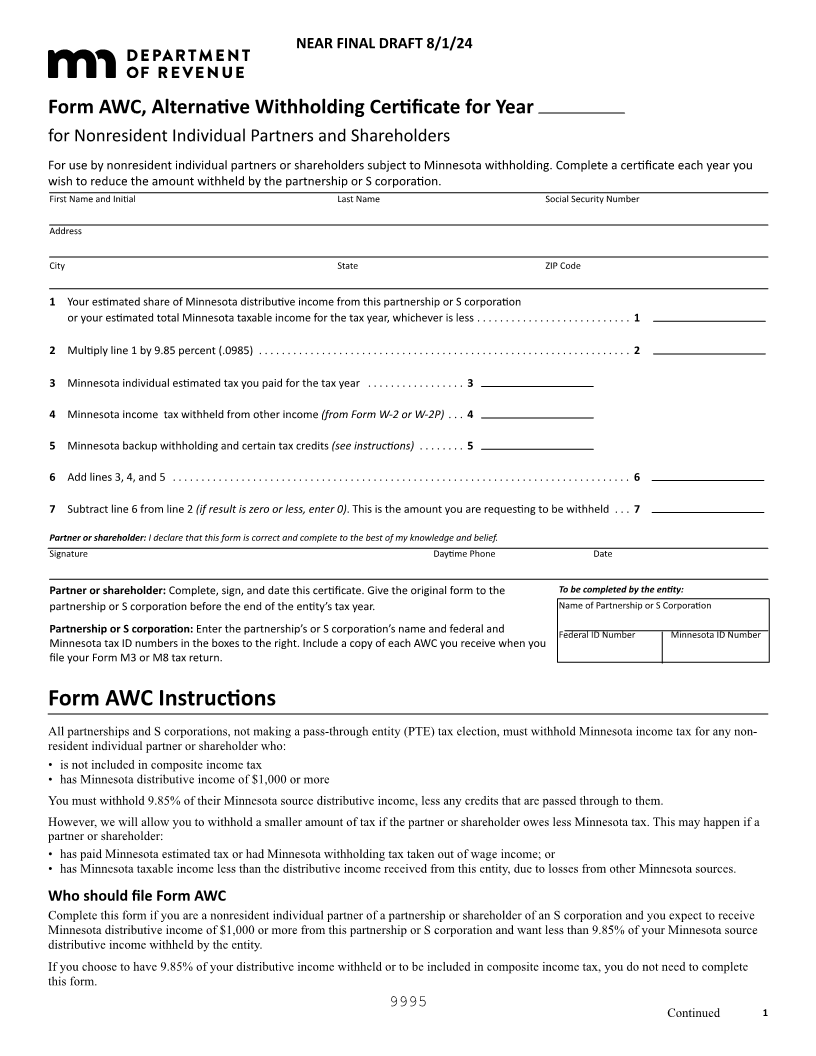

Form AWC, Alternative Withholding Certificate for Year

for Nonresident Individual Partners and Shareholders

For use by nonresident individual partners or shareholders subject to Minnesota withholding. Complete a certificate each year you

wish to reduce the amount withheld by the partnership or S corporation.

First Name and Initial Last Name Social Security Number

Address

City State ZIP Code

1 Your estimated share of Minnesota distributive income from this partnership or S corporation

or your estimated total Minnesota taxable income for the tax year, whichever is less . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

2 Multiply line 1 by 9.85 percent (.0985) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

3 Minnesota individual estimated tax you paid for the tax year . . . . . . . . . . . . . . . . . 3

4 Minnesota income tax withheld from other income (from Form W-2 or W-2P) . . . 4

5 Minnesota backup withholding and certain tax credits (see instructions) . . . . . . . . 5

6 Add lines 3, 4, and 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

7 Subtract line 6 from line 2 (if result is zero or less, enter 0). This is the amount you are requesting to be withheld . . . 7

Partner or shareholder: I declare that this form is correct and complete to the best of my knowledge and belief.

Signature Daytime Phone Date

Partner or shareholder: Complete, sign, and date this certificate. Give the original form to the To be completed by the entity:

partnership or S corporation before the end of the entity’s tax year. Name of Partnership or S Corporation

Partnership or S corporation: Enter the partnership’s or S corporation’s name and federal and Federal ID Number Minnesota ID Number

Minnesota tax ID numbers in the boxes to the right. Include a copy of each AWC you receive when you

file your Form M3 or M8 tax return.

Form AWC Instructions

All partnerships and S corporations, not making a pass-through entity (PTE) tax election, must withhold Minnesota income tax for any non-

resident individual partner or shareholder who:

• is not included in composite income tax

• has Minnesota distributive income of $1,000 or more

You must withhold 9.85% of their Minnesota source distributive income, less any credits that are passed through to them.

However, we will allow you to withhold a smaller amount of tax if the partner or shareholder owes less Minnesota tax. This may happen if a

partner or shareholder:

• has paid Minnesota estimated tax or had Minnesota withholding tax taken out of wage income; or

• has Minnesota taxable income less than the distributive income received from this entity, due to losses from other Minnesota sources.

Who should file Form AWC

Complete this form if you are a nonresident individual partner of a partnership or shareholder of an S corporation and you expect to receive

Minnesota distributive income of $1,000 or more from this partnership or S corporation and want less than 9.85% of your Minnesota source

distributive income withheld by the entity.

If you choose to have 9.85% of your distributive income withheld or to be included in composite income tax, you do not need to complete

this form.

9995 Continued 1