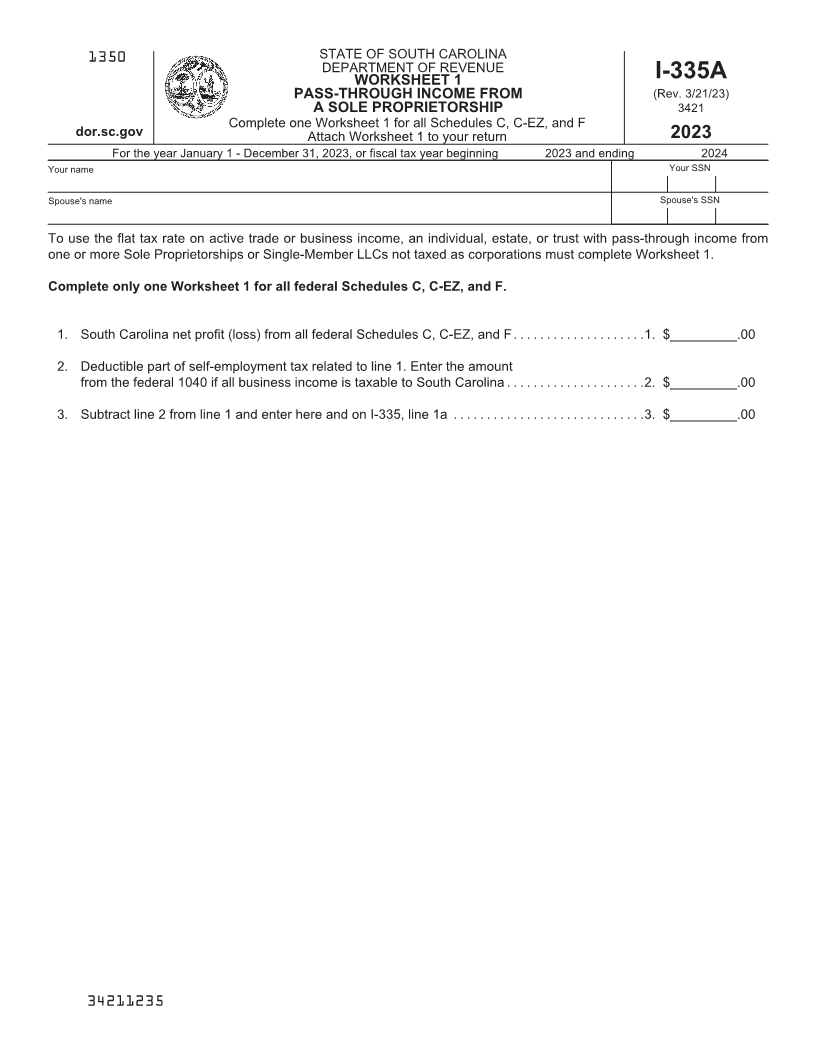

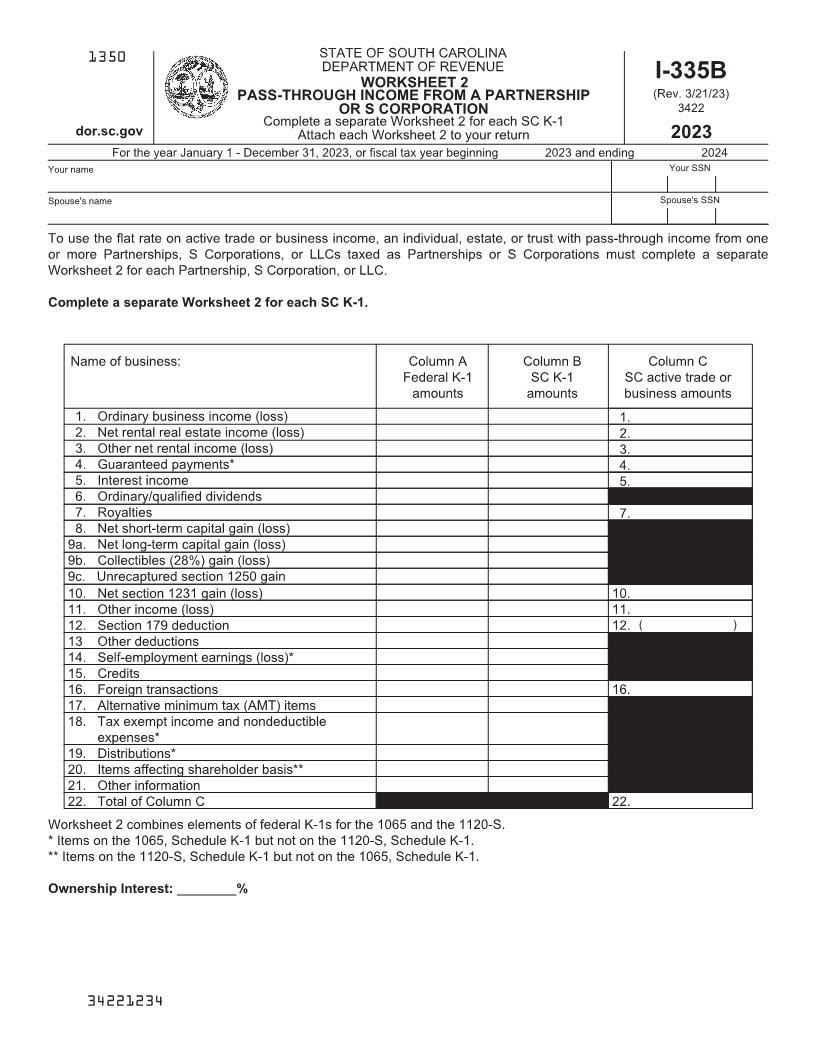

Enlarge image

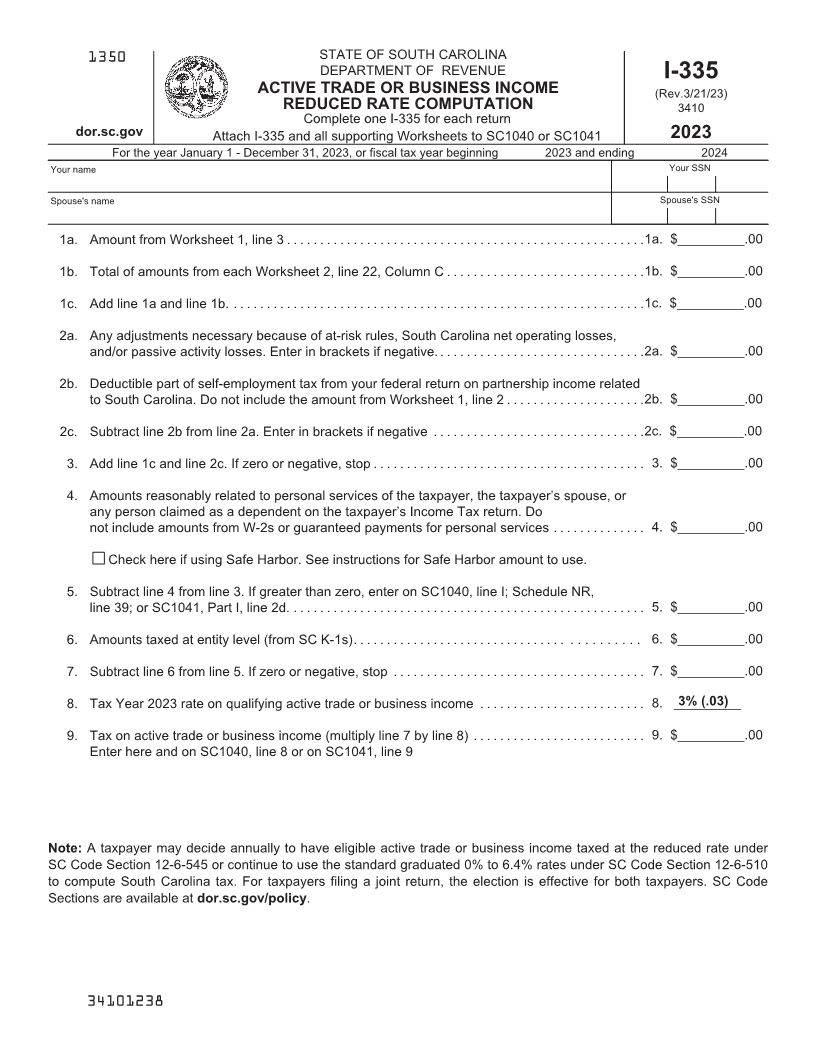

1350 STATE OF SOUTH CAROLINA

DEPARTMENT OF REVENUE I-335

ACTIVE TRADE OR BUSINESS INCOME (Rev.3/21/23)

REDUCED RATE COMPUTATION 3410

Complete one I-335 for each return

dor.sc.gov Attach I-335 and all supporting Worksheets to SC1040 or SC1041 2023

For the year January 1 - December 31, 2023, or fiscal tax year beginning 2023 and ending 2024

Your name Your SSN

Spouse's name Spouse's SSN

1a. Amount from Worksheet 1, line 3 ...................................................... 1a. $_________.00

1b. Total of amounts from each Worksheet 2, line 22, Column C .............................. 1b. $_________.00

1c. Add line 1a and line 1b. .............................................................. 1c. $_________.00

2a. Any adjustments necessary because of at-risk rules, South Carolina net operating losses,

and/or passive activity losses. Enter in brackets if negative. ............................... 2a. $_________.00

2b. Deductible part of self-employment tax from your federal return on partnership income related

to South Carolina. Do not include the amount from Worksheet 1, line 2 ..................... 2b. $_________.00

2c. Subtract line 2b from line 2a. Enter in brackets if negative ................................ 2c. $_________.00

3. Add line 1c and line 2c. If zero or negative, stop ......................................... 3. $_________.00

4. Amounts reasonably related to personal services of the taxpayer, the taxpayer’s spouse, or

any person claimed as a dependent on the taxpayer’s Income Tax return. Do

not include amounts from W-2s or guaranteed payments for personal services .............. 4. $_________.00

Check here if using Safe Harbor. See instructions for Safe Harbor amount to use.

5. Subtract line 4 from line 3. If greater than zero, enter on SC1040, line I; Schedule NR,

line 39; or SC1041, Part I, line 2d. ..................................................... 5. $_________.00

6. Amounts taxed at entity level (from SC K-1s)................................ . . . . . . . . . . 6. $_________.00

7. Subtract line 6 from line 5. If zero or negative, stop ...................................... 7. $_________.00

8. Tax Year 2023 rate on qualifying active trade or business income ......................... 8. _________3% (.03)

9. Tax on active trade or business income (multiply line 7 by line 8) .......................... 9. $_________.00

Enter here and on SC1040, line 8 or on SC1041, line 9

Note: A taxpayer may decide annually to have eligible active trade or business income taxed at the reduced rate under

SC Code Section 12-6-545 or continue to use the standard graduated 0% to 6.4% rates under SC Code Section 12-6-510

to compute South Carolina tax. For taxpayers filing a joint return, the election is effective for both taxpayers. SC Code

Sections are available at dor.sc.gov/policy.

34101238